India LNG demand forecast raised on stronger cooling demand and monsoon downside risks

Stronger cooling demand and rising monsoon downside risks are expected to increase India's call on thermal generation through Q2–Q3. With June rainfall forecast below 92% of the Long Period Average (LPA) and June–September rainfall projected at around 90% of LPA, Kpler Insight has raised its 2026 India LNG demand forecast by 0.25 mt to 25.35 mt. The revision implies approximately 3–4 additional LNG cargoes during the late-Q2 to Q3 period, increasing competition for prompt and Q3 cargoes and reinforcing a modestly bullish bias for Asian LNG prices.

Market & Trading Calls:

- India LNG Demand: Increase, as Kpler Insight raises its 2026 LNG demand forecast by 0.25 mt to 25.35 mt, as stronger cooling demand and increased monsoon-related hydro downside risks lift gas-for-power requirements during the summer months.

- Asian LNG Prices: Slightly bullish, as additional Indian LNG procurement during late-Q2 and Q3 is expected to increase competition for prompt and summer-delivery cargoes, providing incremental support to regional LNG prices.

India’s latest weather outlook points to stronger cooling demand and increasing downside risks to hydro generation through the monsoon season, supporting higher thermal power generation requirements during peak summer demand. The India Meteorological Department (IMD) forecasts June rainfall below 92% of the Long Period Average (LPA), while above-normal temperatures and heatwave conditions are expected across several high-demand regions.

The broader monsoon outlook remains relatively weak. IMD forecasts June–September rainfall at around 90% of LPA, increasing the risk of below-normal hydro generation during the peak demand season. A weaker monsoon would reduce hydro availability at the same time that higher temperatures increase electricity demand, resulting in a larger call on thermal generation during Q2–Q3.

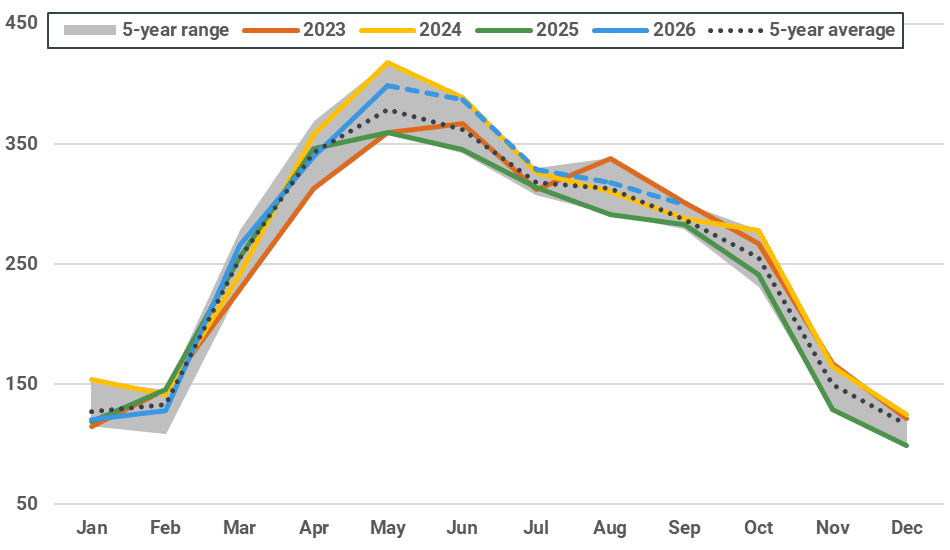

Kpler Insight has therefore revised its June Cooling Degree Day (CDD) assumptions higher to approximately 387 degree-days, reflecting renewed heat risk and a hotter-than-previously-assumed June outlook. July–September gas-for-power demand expectations have also been revised higher to account for the increased probability of weaker hydro generation during the core monsoon period.

The combination of stronger cooling demand and increased hydro downside risks is expected to support higher gas-fired power generation through the summer months. As a result, Kpler Insight has raised its 2026 India LNG demand forecast by 0.25 mt to 25.35 mt, equivalent to approximately 3–4 incremental LNG cargoes concentrated in the late-Q2 to Q3 delivery window.

Although the revision represents only around 1% of total forecast LNG demand, its concentration during the summer procurement season increases its market significance. Additional Indian LNG buying during the peak cooling season is expected to increase competition for prompt and Q3 cargoes, reinforcing a modestly bullish outlook for Asian LNG prices. Risks to the outlook remain centred on stronger-than-expected rainfall during July and August, which would improve hydro generation and reduce the need for incremental thermal power output.

India’s monthly population-weighted Cooling Degree Days (CDD)

Source: Meteostat, Kpler Insight, IMD. Population-weighted average CDD of selected major cities across a country is shown for both historical and forecast.

See why the most successful traders and shipping experts use Kpler