Iran's crude oil storage buffer is shrinking, but the key pressure valve remains cuts

Iran's apparent storage cushion is far smaller than headline figures suggest. While nominal spare capacity stands at around 40 mbbls, condensate infrastructure and operational constraints reduce practical crude storage availability to just 13.5 mbbls, leaving NIOC increasingly reliant on production cuts as export restrictions persist.

Key takeaways

- Iranian onshore crude inventories have increased by 13 mbbls since the US blockade was implemented in mid-April, reaching 74 mbbls.

- Nominal spare storage capacity remains around 40 mbbls, but actual usable crude storage is significantly lower after accounting for condensate tanks and operational constraints. We estimate only 13.5 mbbls of practical crude storage capacity remains available.

- Crude loadings averaged just 260 kbd in May, down from 1.85 mbd during February-April.

- NIOC has already reduced crude production by approximately 1.2 mbd and is likely to deepen cuts if maritime export restrictions persist.

- Onland exports options exist for fuel oil but not for crude, therefore are unable to alter Iran's storage balance.

Iran's crude storage system is coming under increasing pressure as export restrictions continue to disrupt normal oil flows. Since the implementation of the US blockade in mid-April, onshore inventories have increased by 13 mbbls, equivalent to an average build rate of 232 kbd. Onshore crude and condensate stocks now stand at approximately 73 mbbls, with the largest increases recorded at Kharg Island (+5 mb) and the Goreh pumping facility (+5.7 mb).

Iran onshore oil inventories, mbbls

Source: Kpler

At first glance, storage availability does not appear critical. Current utilization rates stand at 63.5%, implying around 40 mbbls of spare onshore capacity. Based on average export volumes recorded between February and April, this would equate to roughly 23 days of exports.

However, the headline figure significantly overstates the amount of storage that can realistically be used for crude oil. Around 10 mbbls of the remaining capacity is tied to condensate infrastructure, primarily at Assaluyeh and the Persian Gulf Star condensate refinery.

Even after removing condensate capacity, the remaining 30 mbbls of apparent spare storage is not fully usable. Operational and logistical constraints prevent many facilities from being filled to tank-top levels. Furthermore, offshore terminals such as Lavan and Sirri are supplied directly by nearby offshore fields and cannot be used to absorb excess onshore crude production.

Using a more realistic assumption of 80% maximum utilisation across crude storage assets, effective crude storage capacity falls to approximately 78 mbbls out of 97 mbbls total installed capacity. After accounting for current inventory levels and condensate stocks, only around 13.5 mbbls of practical crude storage space remains available.

The storage situation would become critical rapidly if production remained unchanged. At pre-blockade production levels, the remaining usable storage space would be exhausted within approximately one week. However, evidence strongly suggests that NIOC has already adjusted output lower, leading to a higher leadtime of around 20-25 days. However, it is likely that NIOC will further decrease its crude oil production if the blockade remains, so as to avoid reaching tank tops.

Combining inventory builds, export performance, and increased domestic refinery runs, we estimate Iranian crude production has already been reduced by around 1.2 mbd, albeit some 60 kbd of condensate output has returned at South Pars in late May. Domestic refinery runs have increased by an estimated 75–100 kbd since April to around 1.96 mbd as authorities attempt to address domestic gasoline shortages. Nevertheless, if restrictions remain in place, production cuts are likely to deepen toward 1.5 mbd below pre-blockade levels.

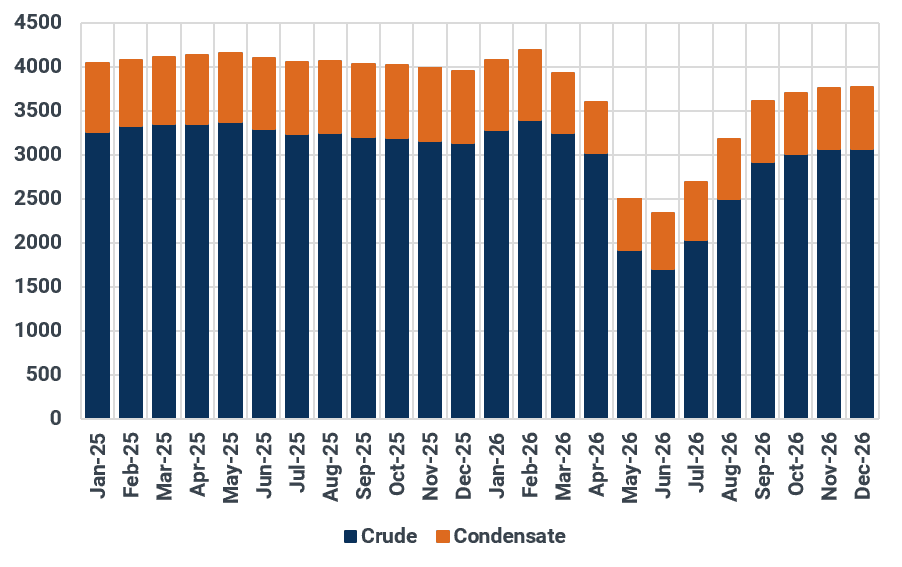

Iran oil production, kbd

Source: Kpler. Our base case assumes a temporary deal between the US and Iran is reached in July.

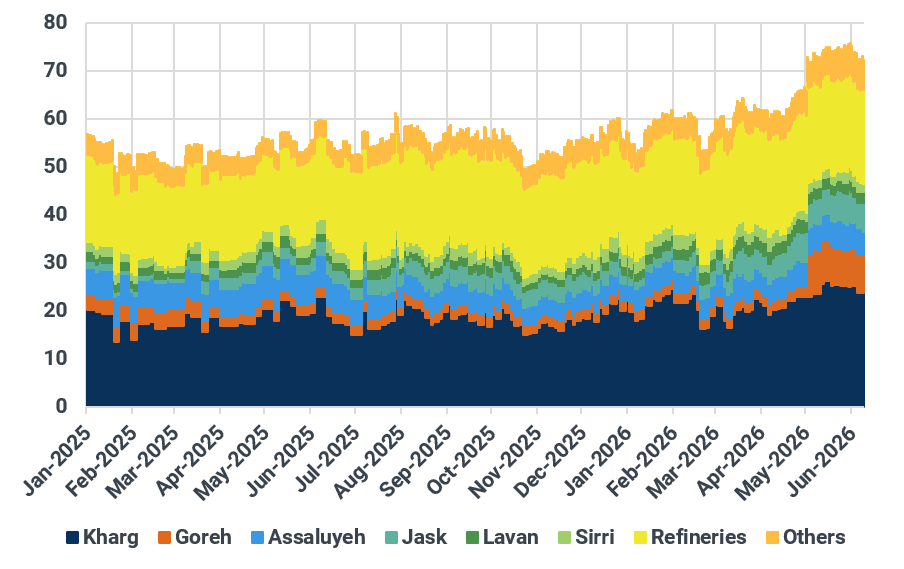

Meanwhile, export activity remains severely constrained although the Goldcrest has been the first VLCC load 2 mb of oil from Kharg since early May. Crude loadings averaged only 260 kbd in May, compared with 1.85 mbd during February-April and more than 2.1 mbd during March and early April.

Iran oil exports by origin port, kbd

Source: Kpler

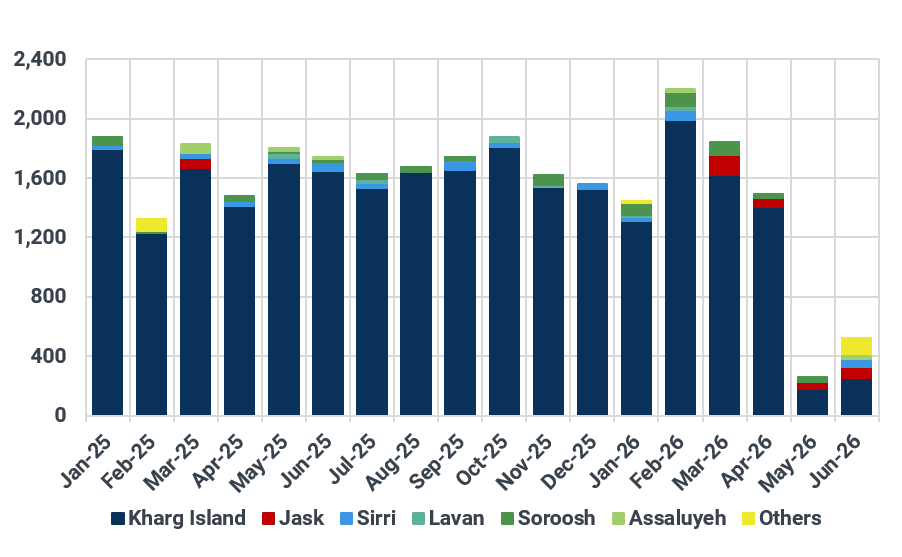

Floating storage inside the blockade zone has increased from 60 mbbls before 13 April to 68 mbbls currently. Although NIOC continues loading some vessels, tankers remain trapped inside the blockade zone between the Persian Gulf and the Gulf of Oman.

Iranian oil on water, mb

Source: Kpler

Overland options remain marginal, rail exports are unlikely

Iran retains several alternative export channels, including truck deliveries into Iraq, Afghanistan, and Pakistan and rail-based shipments through Central Asia. Historically (up until 2012), crude and product swap arrangements used to operate with Caspian neighbors where Iran was an importer of crude, not an exporter.

These routes provide an outlet for some barrels but even if used, would provide marginal relief. Truck exports are largely focused on refined products rather than crude oil and face significant logistical limitations. Due to its gasoline shortage, Iran has been an importer of gasoline and an exporter of fuel oil.

Rail exports offer greater capacity but high transportation costs and logistical constraints mean they're highly unlikely. A typical crude train carries only around 20–25 kb of oil. Replacing 1 mbd of exports would therefore require more than 40 fully loaded trains per day, while replacing pre-blockade export levels would require closer to 80 trains per day. Current regional rail networks are incapable of handling such products and such volumes: they mainly run from China to Iran rather than the opposite, and wagons are not suitable for crude or products transportation. Trains also run at a pace of 1-2 per week only.

The geography further complicates the logistics. Iran's oil fields are mainly located in the southwest of the country, making transportation costs very high and logistics challenging: crude needs to be piped to the Tehran refinery, then trucked to the rail lines and boarded on train. On the Chinese side, Chinese teapots: the sole buyers of Iranian oil, are located in Shandong, far from the rail line which goes to Shanghai.

As a result, overland routes are not a feasible option for NIOC to replace maritime flows. Excess fuel oil and LPG are being smuggled across borders to alleviate localized inventory pressure but crude exports are unlikely to materially recover. Production restraint remains NIOC's primary mechanism for preventing tank tops.

Market insights you can trust

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler