Seasonal shift in grain and oilseed chartering

Demand patterns for grain-carrying dry bulk carriers are shifting as a seasonal change in grain and oilseed cargo availability takes place. Different demand centres will come to the fore, opening up more opportunities for geared tonnage. However, earnings for Panamax vessels will remain robust as a ramp-up in coal shipments compensates for lower demand to carry Brazilian soybeans.

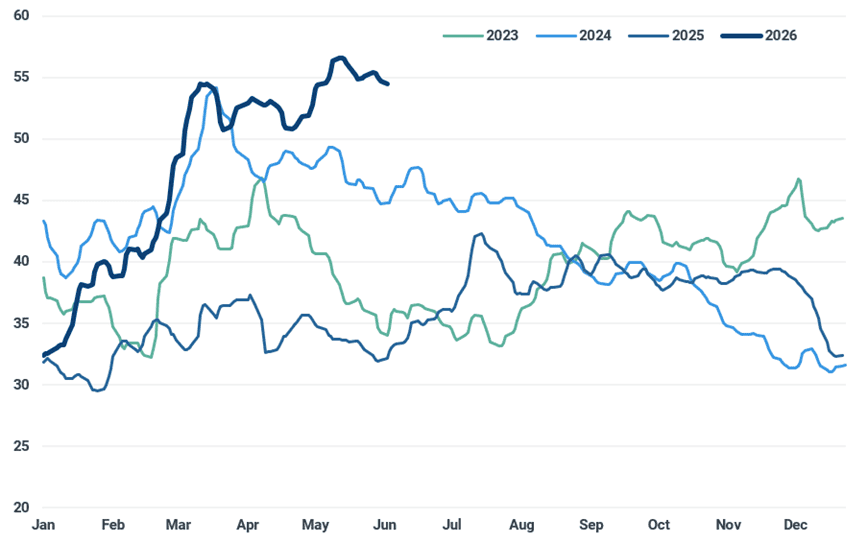

The cost of shipping grains, oilseeds, and other agricultural products soared in the first five months of this year as higher vessel timecharter earnings and a war-driven spike in bunker prices pumped up spot voyage rates. The Panamax P5 (Santos-Qingdao) spot voyage rate averaged $55.10/t in May, 63% higher y/y. The year-to-date average of $47.21/t is 41% higher than the average of January-May 2025.

Demand for grain-carrying dry bulk carriers is now set to change as export patterns undergo a seasonal shift however, we expect spot voyage rates to remain high.

War-driven spike in Santos-Qingdao Panamax spot voyage rate sustained by TC earnings growth ($/t)

Source: Baltic Exchange

Shifting geographies and changing vessel demand patterns

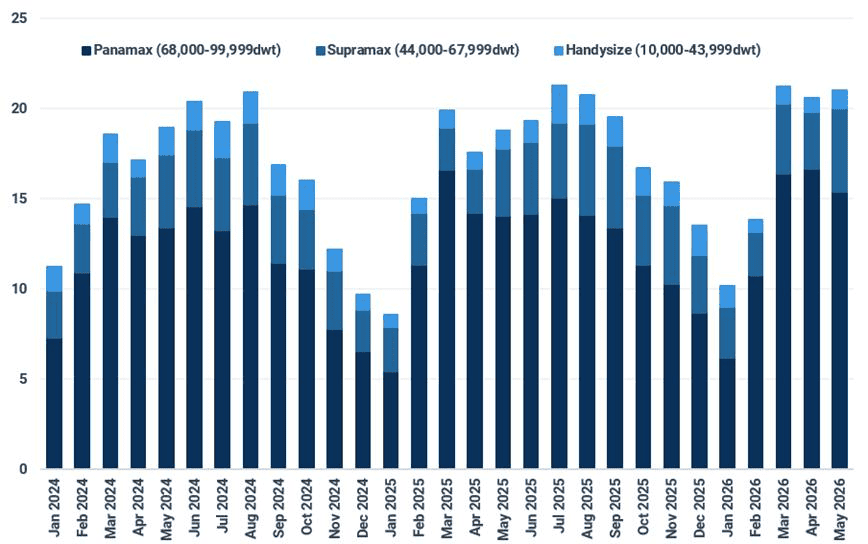

- A seasonal decline in Brazilian soybean chartering activity arrives ahead of the slowdown in physical shipments; vessels are normally fixed weeks ahead of loading. After record exports in April and May, we expect a gradual decline in the pace of Brazilian soybean trade compared to previous years. Meanwhile, the country’s corn exports are now ramping up. Close to 90% (56.78Mt in the year-to-date) of Brazilian soybean exports are carried by Panamax (68-99,999 dwt) dry bulk carriers compared with less than 60% of corn cargoes. Seasonal strength in sugar shipments, as export capacity frees up with the slowdown in soybean shipments, will also support demand for geared tonnage.

Brazilian agricultural exports by vessel type; Panamax share falls as soybeans slow (Mt)

Agricultural exports include soybeans, corn, sugar, plus all other agricultural products shipped in bulk.

Source: Kpler

- Despite outperforming seasonal norms through March-May, US soybean exports are slowing and will hit a seasonal trough in June/July. At the same time, the country’s corn exports are both in seasonal decline and being undercut by cheaper South American material, notably from Argentina.

- We expect another two months (June & July) of very strong Argentine corn exports, which should continue to outperform the year-ago level through the rest of the third quarter. Close to 60% of these cargoes are carried on geared bulkers as the shallower draught allows them to load at river ports. South Atlantic grain chartering is the key factor in the HS3 (Brazil-Continent) spot voyage rate outperforming the year-ago level by 47% in the year-to-date, compared with +37% for the 7 TC average.

- Australian wheat exports, primarily a geared vessel trade, will sharply underperform the year-ago level in June and through the third quarter. Higher freight costs and uncompetitive pricing mean Australian sellers are struggling in markets where they do not have a geographical advantage. Looking ahead, we expect El Niño to negatively impact this year’s crop, with 4q26 shipments to be muted.

Implications for earnings

Lower demand from Brazilian soybean chartering and US Gulf trades will see more Panamaxes stay in the Pacific after discharging cargoes in Asia. A ramp-up in Indonesian coal exports, after a disappointing start to the year, will be important in combatting supply-driven downward pressure on earnings. The exceptionally high Capesize market may provide an additional boost to Panamaxes by encouraging more uptake of the smaller and proportionally cheaper ships. The Capesize:Panamax average earnings ratio has been above 2.30 since 25 May. Supramax and Handysize earnings will see increased demand in the North Atlantic but are likely to continue to lag a strong Panamax market.

See why the most successful traders and shipping experts use Kpler