US shale growth stalls amid a tug-of-war

The US shale sector is locked in a tug-of-war as mounting headwinds from depleted DUC wells, rising natural decline rates, regional bottlenecks and muted upstream activity clash with rising efficiency gains and the powerful incentive of a higher price environment threatening to pull production back up.

Key Takeaways

- US shale growth has stalled over Q2 2026, but upstream activity is gaining momentum, pushing US crude and condensate supply to record highs of almost 14 Mbd in Q4.

- US shale growth has fallen into steeper negative territory as lower upstream activity and discipline by shale operators has kept a lid on any upside.

- While some shale producers have invested into new projects, reflected by a rising US oil rig count, many have been utilizing drilled-but-uncompleted wells, which can be brought online at a lower cost and more quickly.

- The US oil rig count has recently recorded its sixth consectuive weekly increase in early June, indicating that momentum is increasing.

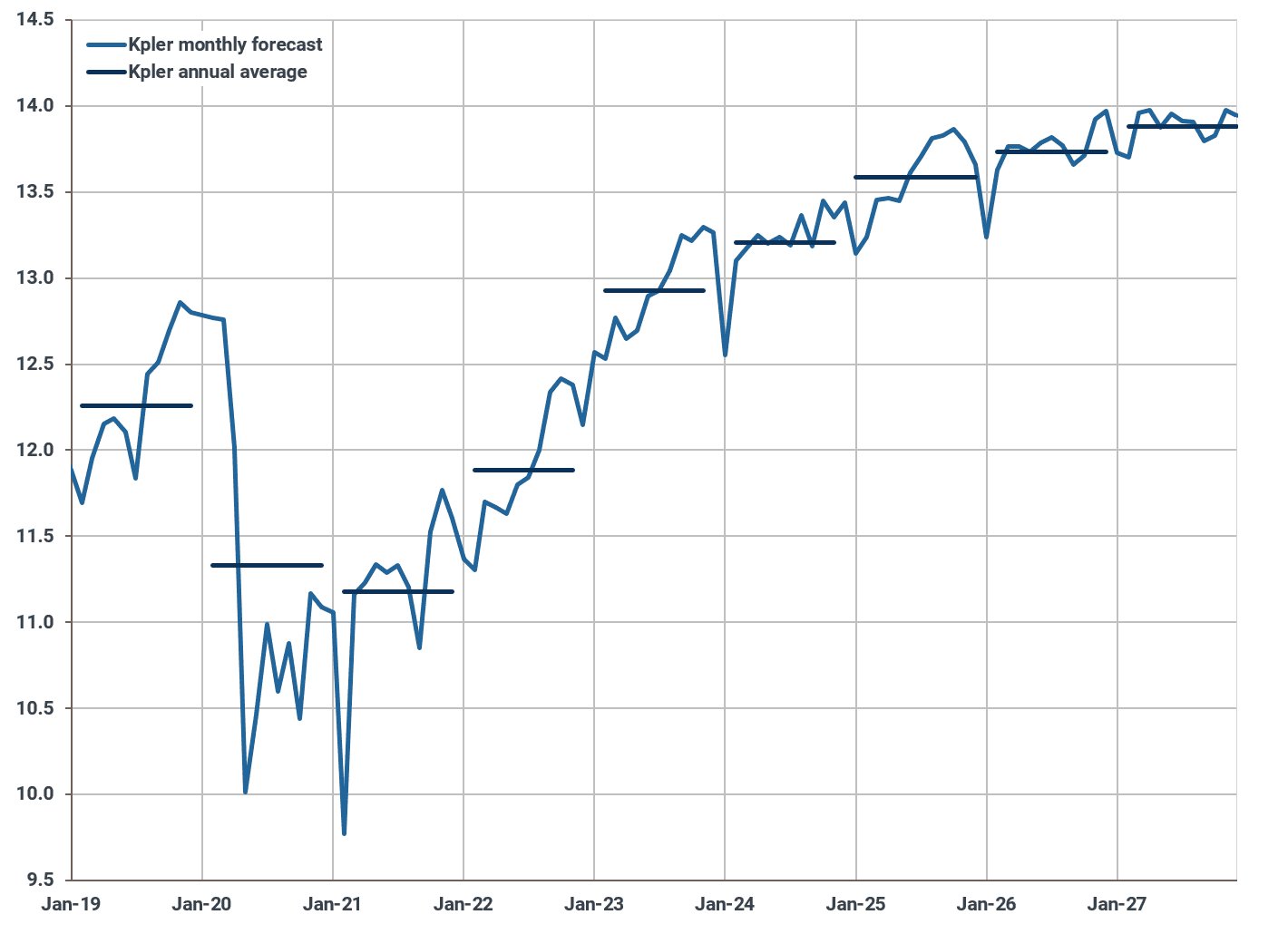

US crude and condensate supply growth has slowed to a near standstill, with weaker growth stemming from both non-shale and shale-producing regions. While output from non-shale areas appears to have plateaued for the time being—led by the US Gulf, where production has been hovering around 2 Mbd over H1 2026—US shale has shown signs of weakness throughout the first half of this year. As a result, US crude and condensate supply has remained largely flat at around 13.7 Mbd over recent months (see chart below).

Looking ahead, upside potential is expected to remain limited despite a higher price environment. Our latest crude price forecast sees prices reaching a low of around $80/bbl over the next twelve months. Although this remains comfortably above producer breakeven levels for the average new shale well, many operators remain hesitant to increase investment in new developments, while others are already well hedged over the coming one to two years.

US crude and condensate production, Mbd

Source: Kpler

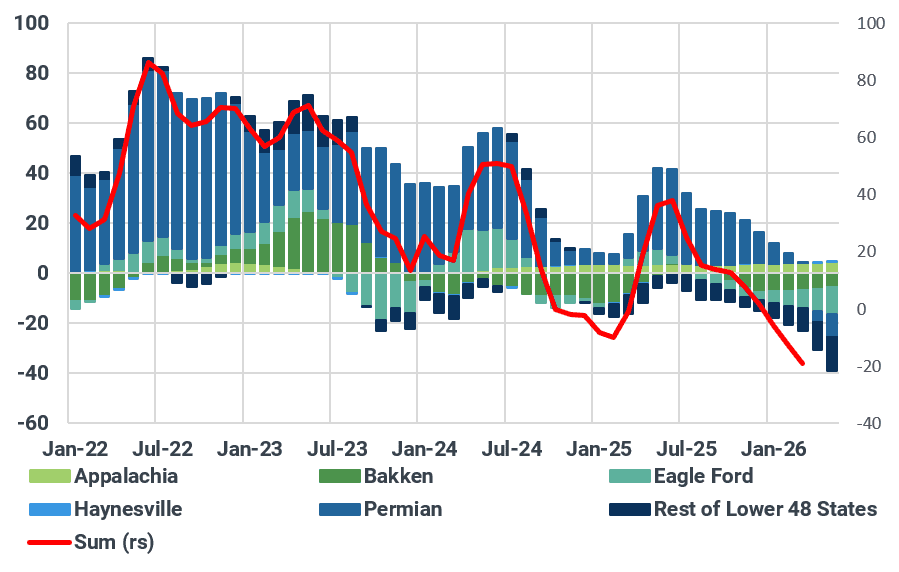

Notably, US shale growth has moved further into negative territory in recent months on a one-year trend basis, helping to explain why total US crude supply has stagnated around the 13.7 Mbd mark. This largely reflects the decline in the US oil rig count over recent years, despite a modest recovery more recently.

The US oil rig count is currently hovering around 430, roughly 20 rigs above the average level recorded since the start of the year. Importantly, the oil rig count recently posted its sixth consecutive weekly increase in early June, suggesting that momentum may be starting to shift in favour of upstream operators, which will help lift domestic output around the end of the year and into 2027.

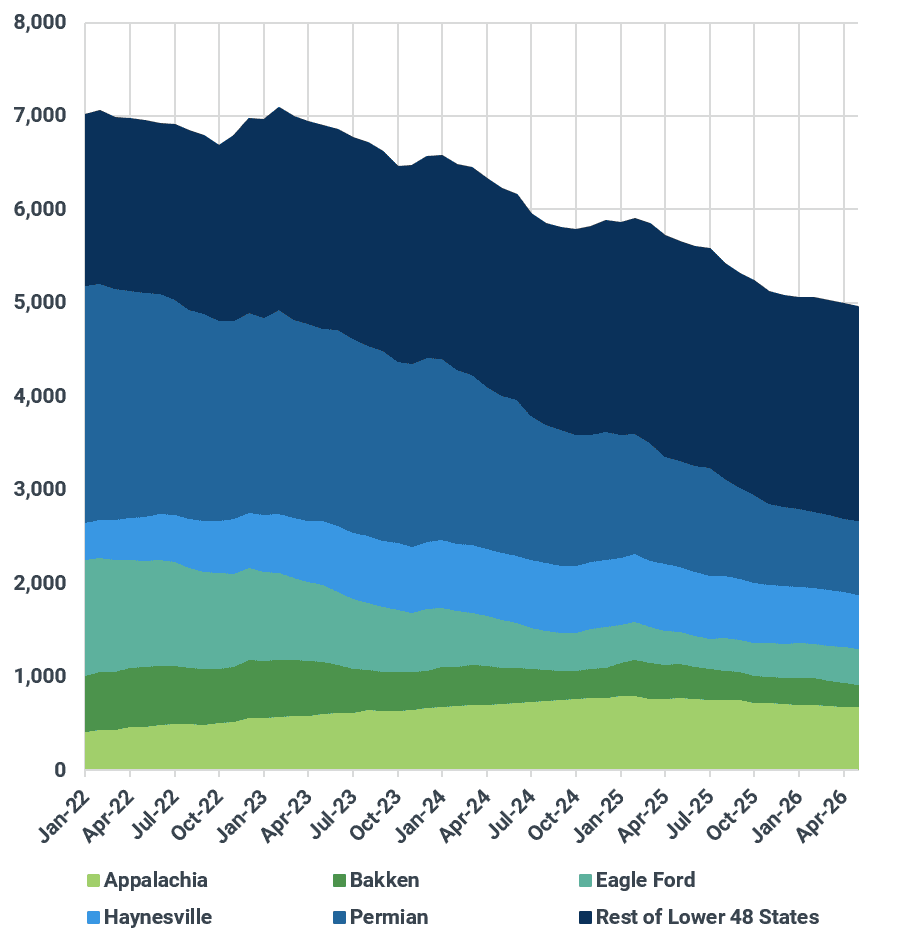

Monthly net US shale growth by basin (1-year trend), kbd

Source: EIA

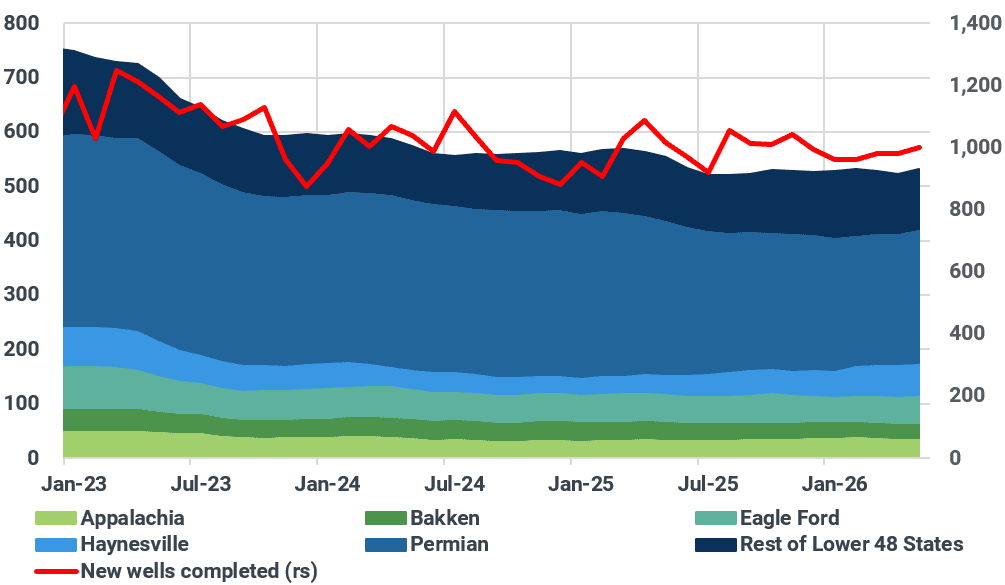

Moreover, while the US oil rig count has remained pressured, the number of new wells drilled per rig has been rising as rigs have become more efficient, meaning that the lower rig count may present a somewhat misleading picture of underlying activity.

Active rig count by basin and completed wells, count

Source: EIA

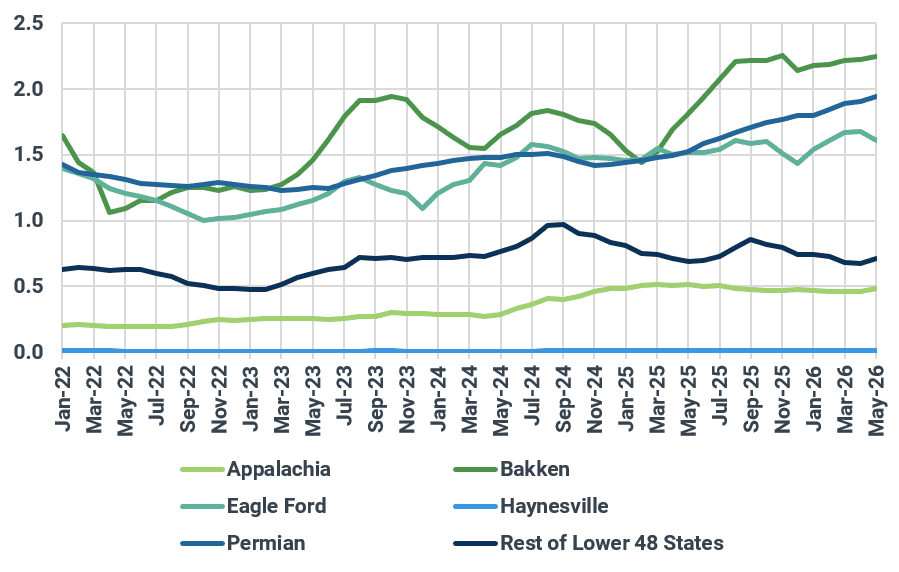

More recent headwinds have emerged in the form of infrastructure bottlenecks, particularly relating to natural gas production in the Permian Basin, as well as higher natural decline rates at ageing fields. However, these challenges have been largely offset by continued efficiency gains. Average crude oil production from newly completed wells per rig has remained on a strong upward trajectory in the Permian Basin, helping to support overall domestic shale output (see chart below).

Crude supply from newly drilled wells per rig, kbd

Source: EIA

Notably, although operators have remained cautious about investing in new developments, many have increasingly relied on drilled but uncompleted (DUC) wells, which can be brought online more quickly and at a lower cost than drilling entirely new wells. This development has been corroborated by the recent rise in the frac spread count, which has outpaced the increase in the US oil rig count this year.

The frac spread count currently stands at around 190, up by roughly 30 compared with average levels seen earlier in the year. While the inventory of drilled but uncompleted wells has continued to decline, with Permian Basin DUCs currently standing at 783—down 363 from July 2025 levels, or around 32%—the pace of drawdown appears sustainable for at least another year in the Permian Basin, before additional drilling becomes necessary. For other shale basins, such as the Bakken or Eagle Ford, DUC inventories are very tight, which may keep potential growth limited.

Taking these factors into account, and assuming our forecast of a higher price environment encourages increased drilling activity during the second half of the year, US crude and condensate production should reach new record highs by late 2026 of around 13.9 Mbd. Notably, declines in non-shale production are expected to be fully offset by higher shale output, primarily driven by growth in the Permian Basin.

Drilled-but-uncompleted wells, count

Source: Kpler

See why the most successful traders and shipping experts use Kpler