Kpler Arbitrage | The Arb View: Brent Dubai EFS Widens on European Tightness and Dubai Contango

Executive Summary

Trading calls

- Neutral on Dubai M1M3. We expect structure to remain in contango this week, but multi year low levels should draw selective buying and keep the spread range bound rather than pushing materially wider.

- Bullish CPC premiums near term as CPC terminal disruptions limit supply.

Middle East & Asia: Dubai Structure flips into contango on Supply Fears

Dubai M1M3 flipped into contango last week, averaging around -$0.30/bbl, the weakest since 2023. The move has been building for weeks on soft prompt fundamentals and an overhang in medium sours, but it was amplified by the difficulty Glencore had placing February loading Upper Zakum cargoes. Even after those barrels were reportedly cleared, mainly to Chinese state buyers, Dubai stayed in contango and only recovered marginally, indicating the weakness is being driven by the broader prompt balance rather than the clearing of the February overhang.

For this week, we still expect Dubai M1M3 to hold in contango, but stay range bound rather than sliding much further. The spread is already at a multi year low and that level tends to attract some buying, even if fundamentals are not improving. We do not see the setup for a strong recovery either. Excess prompt barrels remain available and Kpler’s supply demand data points to around a 3mbd surplus in Q1. At the same time, discounted Russian and Iranian cargoes are still clearing at steep discounts; Urals is currently landing at about $19/bbl cheaper than Dubai swaps (about $10 decline from a month ago). This limits the urgency for China to pay up for alternatives and keeps a lid on Middle East spot demand.

Aramco’s 30c OSP cuts into Asia are consistent with the weak spot market and look aimed at defending market share. Term nominations should stay firm, leaving less room for Atlantic Basin barrels to move. On our arbs dashboard, Angolan medium grades appear workable, but the arb is not compelling enough to drive a broad shift in buying. Kissanje and Hungo land into Ningbo at around +$2.55/bbl and +$2.80/bbl versus Dubai swaps, undercutting delivered alternatives such as Qatar Al Shaheen and Brazil’s Mero. Kissanje is particularly interesting as it’s landing at the lowest level we’ve seen in over a year and while Asian refiners are reported to have secured some of these barrels for Feb loading, we see limited upside for these volumes.

Sanctioned barrels will continue to set the ceiling for spot Middle East premiums. Even as refiners like Reliance step back from Russian crude, the replacement slate is not automatically Middle East. With Jamnagar taking record level LatAm, US, and Canadian inflows last week, the signal is that the refiner is leaning into heavier barrels and blending them with Midland to approximate a Urals type feedstock. That is a clear diversification move away from Russian barrels and could offer marginal support to Middle East spot demand over time, but it does not change the core constraint. As long as Urals remains deeply discounted, the sanctioned pool stays aggressively priced and keeps the Dubai structure capped in contango for now.

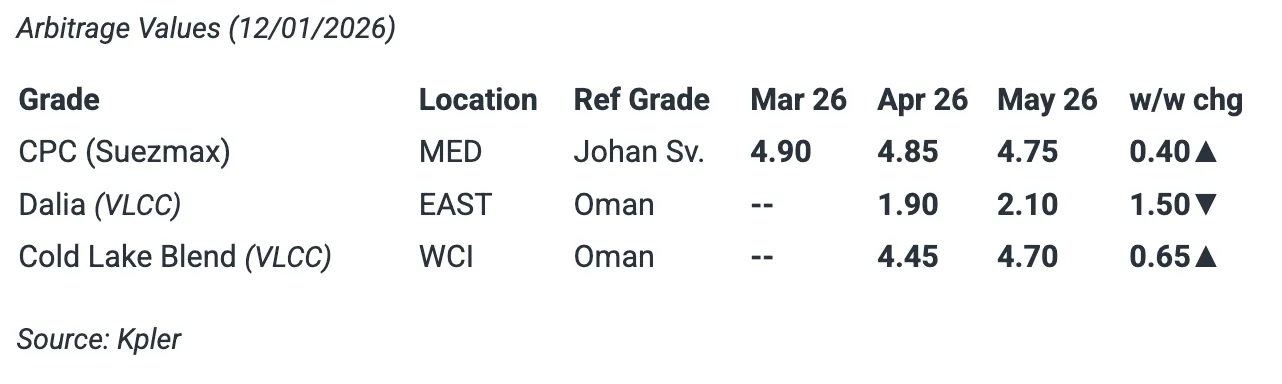

Landed Values of Selected Grades into West Coast India

Source : Kpler

Atlantic Basin: European prompt crude tightens, but Brent-Dubai EFS blocks the eastbound pull

The prompt month Brent-Dubai EFS widened sharply to around $1.30/bbl last week from about $0.70/bbl the week before. The rise is primarily due to European physical tightness on supply disruptions, and weaker Dubai pricing as the prompt Middle East overhang drags structure lower.

On the European side, CPC has been the clearest driver. Loadings out of the Black Sea stayed constrained on SPM issues, with only one cargo being loaded during the week beginning 29 December, compared to the usual 10+ cargoes. Furthermore, in Libya, repeated weather disruption kept several ports closed, including Es Sider, Zawia, Ras Lanuf, Marsa el Brega and Zuetina, with no firm restart timeline, tightening the prompt Med slate further.

This tightness is keeping substitutes in play, with buyers leaning toward grades that need minimal blending while still offering a clear economic edge. Arab Light is landing competitively for February at around $0.95/bbl after the latest OSP cuts, and it stays in the mix as long as CPC remains unreliable. Guyana’s Liza is also standing out as a clean swap on specs and availability. It can run with limited blending and is landing about $0.30/bbl below Arab Light, which keeps it one of the most workable CPC alternatives on paper. Hellenic has already taken its first Liza cargo, discharged on 4 January on the Suezmax Patriotic, and that looks repeatable if CPC and Libyan delays drag on.

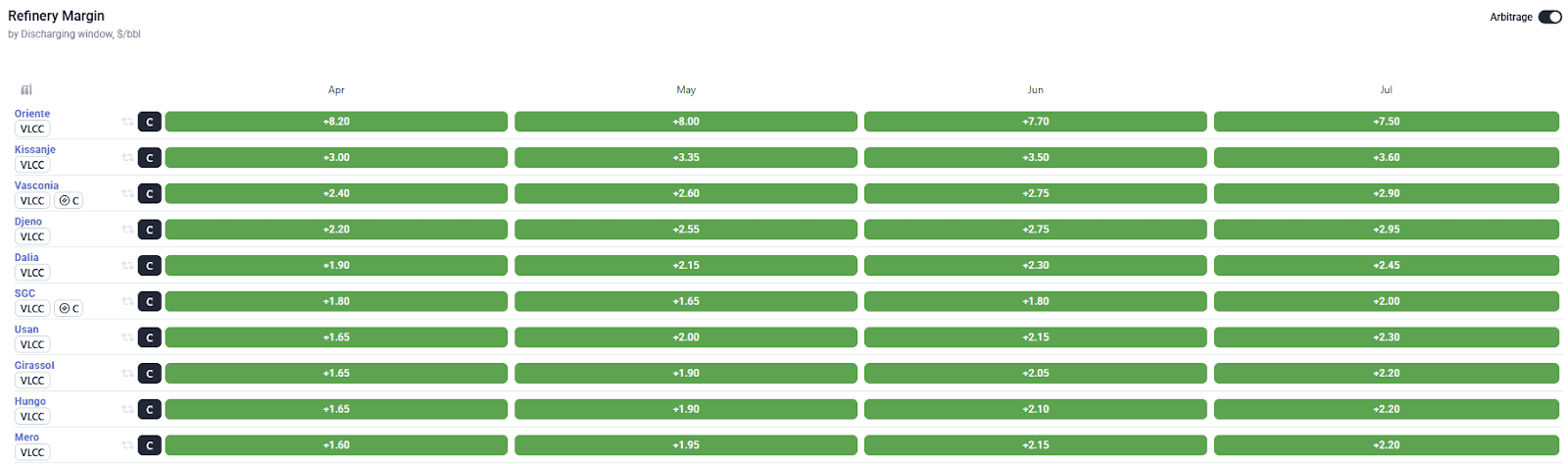

Meanwhile, Angolan arbs to the East are looking workable, with Dalia and Girassol showing close to $2/bbl margin over Oman and Murban respectively. The move is mainly freight led, with VLCC WAF to Asia costs down by more than $2/bbl since December, and Chinese buying has followed. We have over 100 kbd of January loading Dalia heading to Asia across four cargoes, with two reportedly chartered by Sinopec. Into March, though, we would still treat this eastbound strength as fragile. Cheap Dubai and a wider Brent Dubai EFS keep Middle East barrels competitive, which limits how far Angolan differentials can extend unless sellers lean into deeper discounts or freight softens again.

Arb Values of Selected Medium Grades into Eastern Asia

Source : Kpler

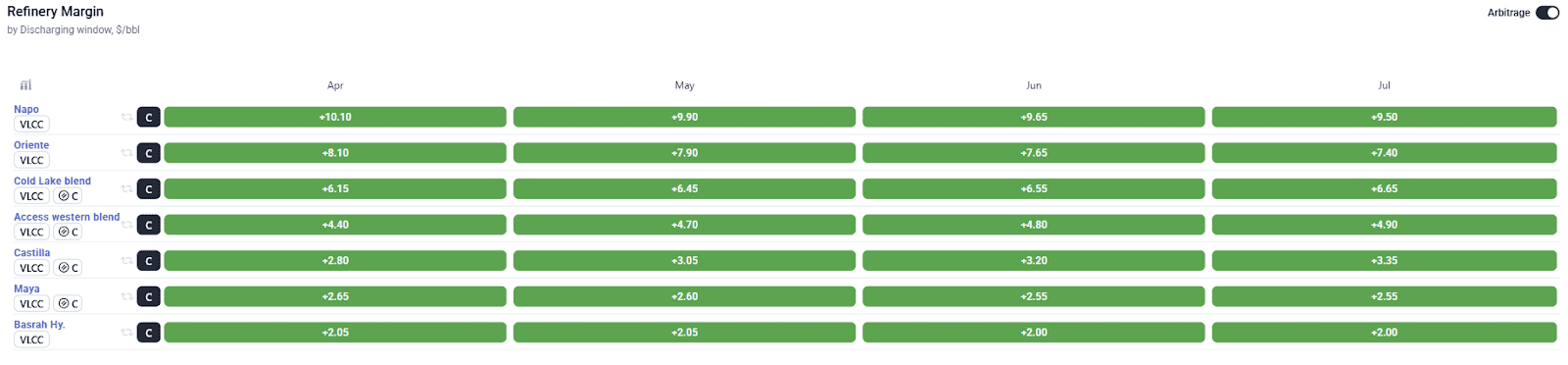

Americas: Venezuela risk reshapes heavy sour pricing and hits Canadian diffs

Recent US Venezuela tensions dominated headlines last week and have quickly fed into heavy sour pricing, with Canadian Cold Lake the clearest pressure point. The latest US posture signals tighter oversight of Venezuelan export routing and a higher likelihood that incremental barrels are steered into the USGC over time. That matters because USGC refiners are structurally the natural home for Merey, Boscan, and Hamaca, and those grades compete directly with USGC heavy sour substitutes such as Cold Lake Blend.

Markets are already reacting to that scenario. Canadian heavy diffs, along with Ecuador’s Napo and Oriente, have softened on the view that a return of Venezuelan cargoes would push more heavy sour into the USGC and squeeze out competing barrels. With roughly 400 to 500 kbd of Canadian barrels exposed to the USGC, even a gradual Venezuelan ramp creates meaningful displacement risk. Cold Lake is unlikely to move to China given trade frictions with the US, but weaker heavy diffs could make Ecuador’s Napo and Oriente more competitive into Asia. That being said, sanctioned alternatives still set the floor, especially for many teapots and remain the biggest hurdle to a large-scale shift.

The real question is how reliable Venezuela becomes, and that is a medium term watch. In the near term it is still messy: ageing infrastructure and blending limits, and day to day operational uncertainty can quickly translate into uneven loadings. But if waivers broaden, volumes can edge higher into mid 2026, with any larger ramp only coming if producers step up upstream investment. That setup keeps the bias softer for Canadian heavy diffs over the next year, with a milder drag on US medium sours, while US light sweets should stay supported since they do not compete directly with the heavy sour barrel.

Arb Values of Selected Medium & Heavy Sour Grades into Eastern Asia

Source : Kpler

Kpler Arbitrage just launched

Kpler’s Arbitrage platform turns complex freight, quality, and benchmark data into simple, actionable arbitrage insights so you can discover value windows, rank opportunities, and build scenarios confidently.

With Arbitrage you can:

- Compare delivered crude values by region and freight cost

- Quantify refining margins and route profitability

- Spot open arbitrage opportunities quickly

- Breakdown value drivers like FOB differentials, spreads, and freight

- Model scenarios with custom market inputs

Find out more

See why the most successful traders and shipping experts use Kpler

Unmatched crude arbitrage intelligence -pricing, freight, and flow data in one platform

.jpg)