Kpler Arbitrage | The Arb View: Brent Dubai EFS widens on US-Iran geopolitical risk

Geopolitical headlines pushed risk premium back into the front of the curve, with Brent leading and the Brent–Dubai EFS widening. At the same time, softer Atlantic Basin differentials are starting to reopen selective eastbound economics, particularly for LatAm heavy crude. In the West, barrels are still having to move on price as refiners head into maintenance.

Executive Summary

Arbitrage Values (23/02/2026 07:00 UTC)

Source: Kpler

Trading calls

- Bullish Brent Dubai EFS. As US-Iran tensions tighten supply on the back of increased risk within the MEG.

- Moderately bullish WAF diffs. Start-up of India’s HRRL refinery is temporarily supportive for light sweet crude but elevated freight will keep a lid on prices.

Middle East and Asia: EFS Firms as US-Iran Tensions Heighten Risk Premium

US-Iran headlines drove last week’s price action. North Sea Dated gained $2.52/bbl to $71.85/bbl last week, with buying accelerating mid-week as the market started paying up for near term risk. Dubai’s prompt structure also saw a slight upward move on the back of this, with the M1/M3 trading just over $1/bbl, 20c higher w/w as traders priced a higher disruption premium into MEG barrels.

A full Hormuz closure still looks unlikely given Iran’s reliance on the route for its own exports. But the market does not need an outright blockade to feel tighter. If shipowners become more cautious around Iranian waters, fewer vessels are willing to enter the Gulf, insurance and lenders get more conservative, and prompt availability tightens. That dynamic supports MEG barrels and keeps Dubai structure firm even if physical supply has not actually been cut. In contrast, Brent has done most of the moving, widening the Brent–Dubai EFS to around $1.9/bbl, contrary to our bearish view last week when CPC flows were expected to weigh.

Even so, with uncertainty still surrounding MEG supply and LatAm and WAF diffs continuing to soften, some Asian refiners may see current levels as good enough to secure a few long hauls. This is more likely to skew toward India than China. Chinese teapots remain well covered with roughly 9 mmbbls of Russian crude floating in the region, so there is less urgency to diversify. India, on the other hand, has more flexibility in its slate and incremental demand potential as new refining capacity gradually comes online.

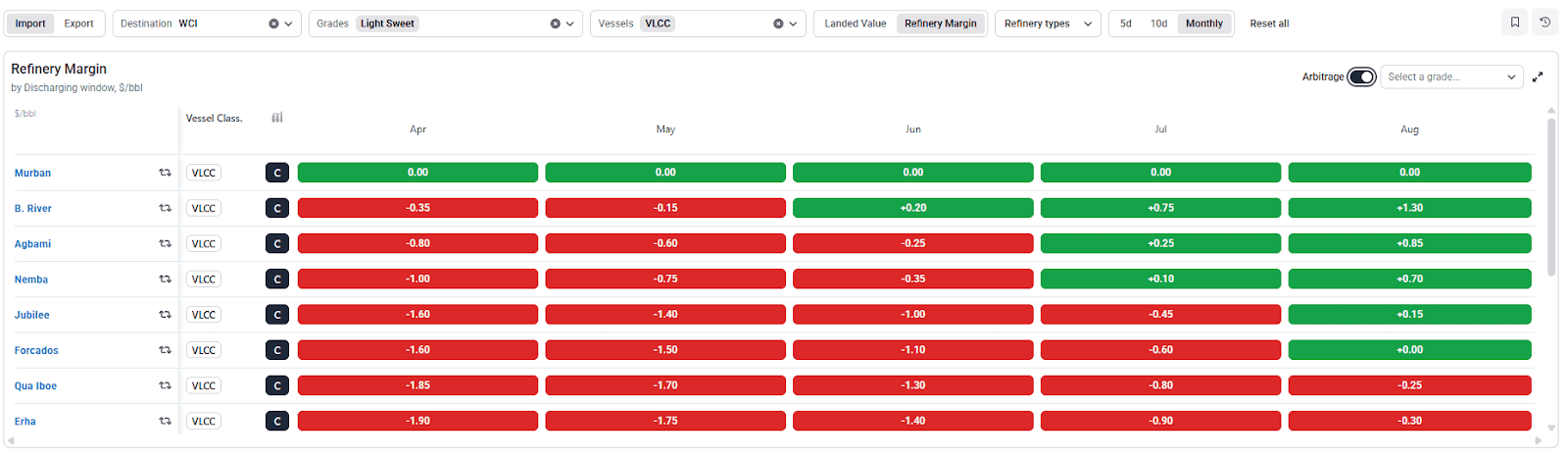

In our previous arb view, we highlighted that WAF and LatAm grades could start flowing into WCI, and that is now starting to show up in fixtures. Nigeria’s Erha has fixed to India, and Ecuador’s Oriente has also moved East. Erha is particularly interesting because it had been flowing to Senegal’s Mboa refinery before being displaced late last year by Bonny lt, so it is effectively looking for alternative outlets. In this case, it looks more like a blending play than a pure arb move, given WAF light sweet arbs to WCI remain shut.

Light Sweet Arbs to WCI

Source : Kpler

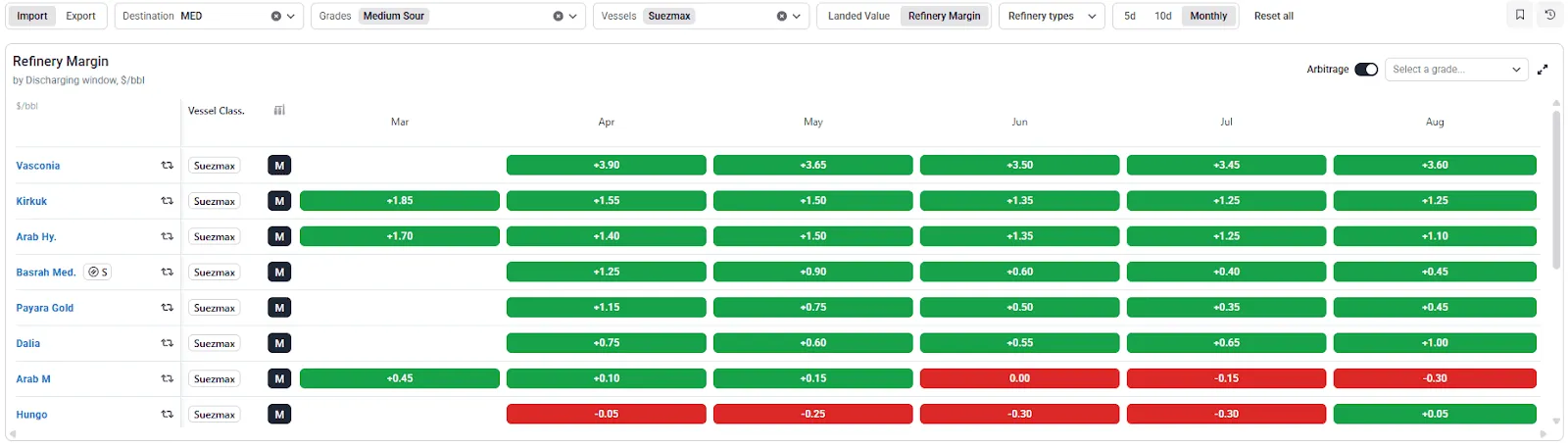

Atlantic Basin : Druzhba Disruption Could Reshape Med Flows as CPC Softens

CPC FOB Novorossiysk diffs have dropped sharply to around a $9/bbl discount to Dated, marking their weakest levels since May 2023. A March loading cargo was reportedly offered in the window at a steep discount, broadly in line with where traders would expect the grade to clear. The move reflects lingering concerns around supply reliability. With Tengiz disruptions and loading revisions still fresh, traders are likely demanding lower pricing to compensate for uncertainty and the added risk around Black Sea loadings. Confidence that flows will run smoothly seems limited, so diffs are adjusting accordingly. On our arbs dashboard the East is looking profitable, but with Ukraine strike risk still in the background, buyers will want to see a few cleaner programmes before leaning into eastbound cargoes.

Another development in the Med is the Druzhba pipeline disruption. Since flows stopped on 27 January following the attack, Hungary and Slovakia have had to rely more heavily on seaborne barrels through Omisalj and up the Adria line. There is talk of a Russian cargo arriving under the carve out, but Kpler tracking has not yet confirmed this. In the meantime, we are likely to see a pickup in non-Russian imports into Omisalj, which could lend support to competing grades, especially as runs trend lower and Hungary’s crude stocks have drawn by roughly 2 mmbbls over the past week.

In terms of suitable replacements, Johan Sverdrup and Guyana’s Payara Gold stand out as the cleanest alternatives to Urals into the Med right now. They land competitively and sit closer to Urals specs, meaning refiners can run them with little to no blending. WAF light sweets can work on paper, but in practice they would likely need to be blended with heavier grades to replicate a Urals style slate, which makes execution less straightforward.

In NWE, Ekofisk diffs are firm enough to make imported barrels, including WAF cargoes, look workable on a landed basis. The issue is timing. Many European refineries are heading into spring maintenance and WAF to NWE freight remains elevated. So even if the arb works on paper, it may not translate into a meaningful pickup in buying until runs recover or freight eases. One factor to watch is the start-up of India’s 180 kbd HRRL refinery at Barmer, which is expected to begin taking crude in the coming weeks. Although the refinery is designed to run heavier, higher sulphur grades, several secondary units are not yet fully ready, meaning early operations are likely to focus on lighter, low sulphur barrels. That could temporarily support demand for Nigerian light sweets before the refinery ramps up toward its intended sour slate.

Medium Sour Arbs to Med

Source : Kpler

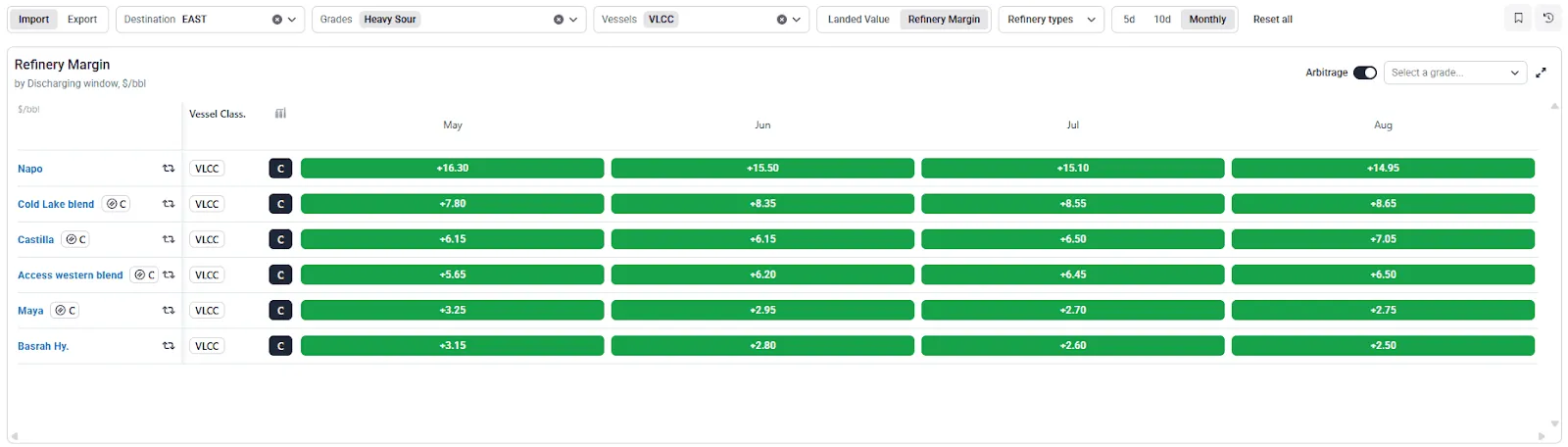

Americas : LatAm Heavy Diffs Slide, India Fixes Oriente VLCC East

Diffs across the LatAm heavy complex are still having to move lower to stay competitive against Venezuelan crude. Kpler cargo flows show more Venezuelan barrels heading directly to US refiners, with Valero expected to lift up to 6 mmbbls in March. That keeps supply concentrated in the Gulf just as maintenance caps runs, effectively forcing competing grades to price lower to clear.

Freight is not offering much relief. USGC to Asia VLCC rates are at multi-year highs, above $7 per barrel equivalent, which keeps long haul options expensive. That said, some eastbound economics are starting to look more workable as diffs slide. The Napo arb to Asia is now closer to $16/bbl versus Oman on a Suezmax, up about $6/bbl from a week ago, largely driven by weaker LatAm pricing. Asia has now become a more credible outlet and should help limit how much further USGC heavy diffs need to fall. We are already seeing India lean into that optionality with Napo and Oriente cargoes, and that flow should remain in play as long as LatAm diffs stay soft.

On the lighter side, Midland arbs into NWE have reopened as the WTI-Brent spread widened to an average of $4.9/bbl last week, roughly $1 higher month on month. Firmer Ekofisk diffs following the CPC disruption have also improved the relative economics for imports. Even so, timing works against a meaningful pickup. With European refineries moving into spring maintenance, buying interest is likely to stay muted, and Midland exports into NWE have already slipped to around 800 kbd, lowest weekly level so far this year.

Heavy Sour Arbs to the East

Source : Kpler

Kpler Arbitrage

Kpler’s Arbitrage platform turns complex freight, quality, and benchmark data into simple, actionable arbitrage insights so you can discover value windows, rank opportunities, and build scenarios confidently. With Arbitrage you can:

- Compare delivered crude values by region and freight cost

- Quantify refining margins and route profitability

- Spot open arbitrage opportunities quickly

- Breakdown value drivers like FOB differentials, spreads, and freight

- Model scenarios with custom market inputs

See why the most successful traders and shipping experts use Kpler

.jpg)