UK opens the door to Russian-origin products

The UK has issued a General Trade Licence permitting imports of middle distillates processed from Russian crude in third countries, removing a key barrier for Indian refiners targeting the UK market. Jet is the more affected product — Shell Haven's LR2-capable jetty and direct UKOP pipeline access give East of Suez cargoes a clean, scalable route into the UK distribution system, capping NWE crack rally potential. Diesel feels the policy change less acutely, with the real bearish driver remaining Atlantic MR freight rates, which have cratered and are feeding directly into delivered price weakness.

A new UK General Trade Licence clears the compliance barrier on importing diesel and jet refined from Russian crude in third countries — effective immediately- Jet bears the brunt: Shell Haven's LR2-capable jetty feeds directly into UKOP, giving Indian exporters a logistically seamless route into the UK pipeline system, creating a cap on NWE jet crack rallies

- Diesel impact is limited: limited major LR2-capable discharge infrastructure exists for road fuels, and the real price signal remains Atlantic MR rates — which have declined, bearing down on delivered diesel independently of today's policy shift

The UK's Department for Business and Trade issued General Trade Licence GBSAN0004 yesterday, coming into force 20 May. The license carves out diesel and jet fuel processed from Russian crude in third countries from the UK's Russia sanctions regime — effectively greenlighting product from Indian and Chinese refiners running Urals or ESPO and exporting into the UK market. The change reflects a structural reality that has been building for some time: the UK has grown increasingly short on both gasoil/diesel and jet/kero as its refining capacity has contracted, leaving it with limited room to be selective about origin.

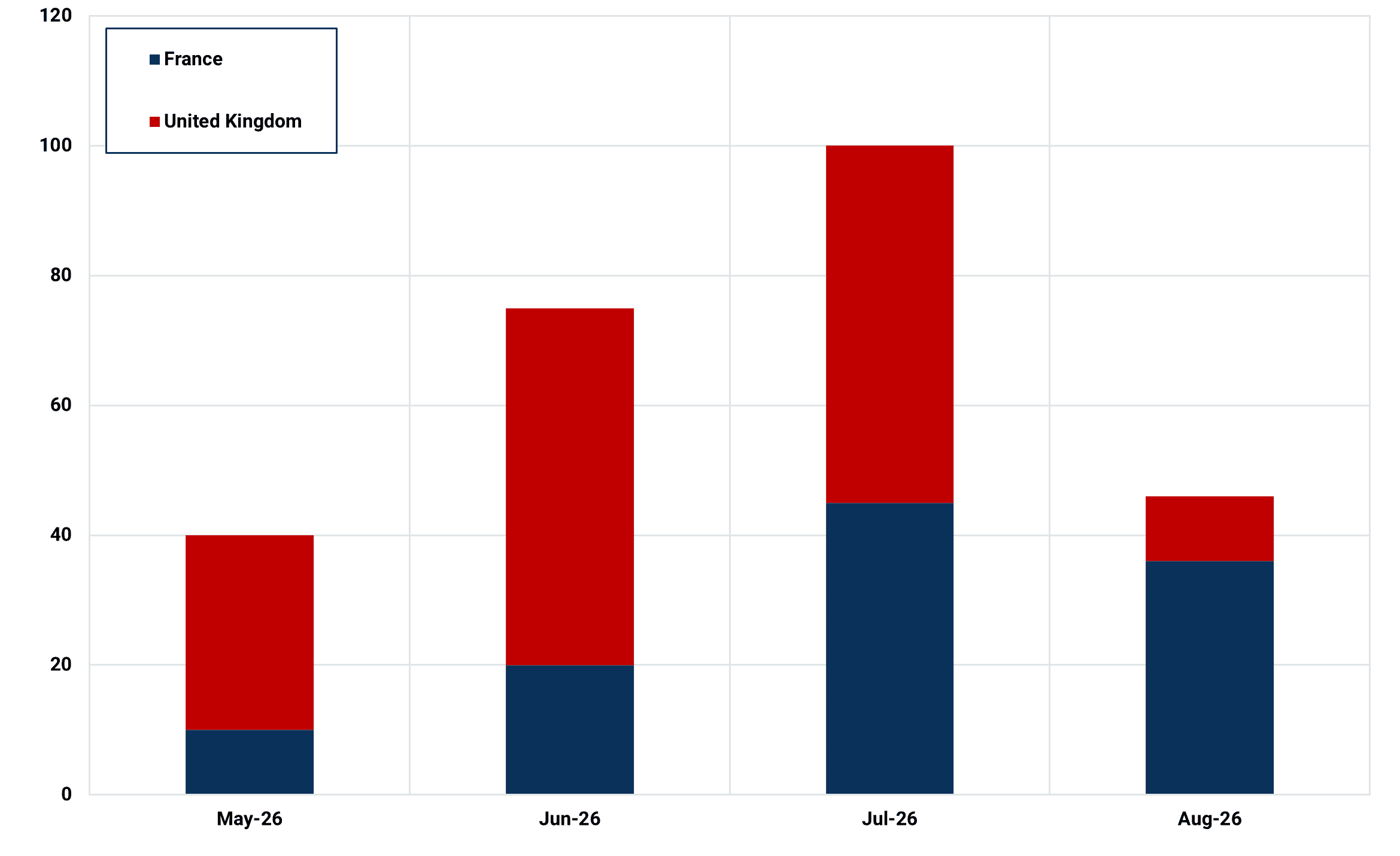

The jet market is where the impact is most direct. Indian refiners — Reliance chief among them — are significant producers of export-grade jet running on Russian crude, and these flows had been the natural supply offset until the EU’s and UK’s sanctions. With those flows constrained, Kpler estimates around 30 kbd of jet/kero demand destruction has already materialized this month, with a further step up to 55 kbd projected for June as the sharp drop in imports feeds through. This trade license addresses that gap directly.

UK, France jet/kero demand destruction (kbd)

Source: Kpler

The timing is pointed: OFAC's recent 30-day moratorium allowing Indian refiners to lift distressed Russian crude, means that such crudes are already being digested by its refiners, and the UK GTL now provides a clean destination for the resulting jet barrels. Separately, New Delhi has cut the Special Additional Excise Duty on ATF exports from 33 rupees ($54/bbl) to 16 rupees per litre ($26/bbl), improving incentives for Indian jet exporters.

The physical infrastructure makes this route particularly compelling. Shell Haven — the UK's largest aviation fuel import terminal, capable of accommodating vessels up to 135,000 DWT — feeds directly into UKOP, which supplies over half of Heathrow and Gatwick's fuel requirements. Oikos, which requires ongoing dredging works, and Milford Haven offer additional pipeline-connected alternatives, though both operate at comparatively smaller scale. An LR2 loading in India can discharge at Shell Haven and inject straight into the pipeline system without cargo breakdown or transshipment. With the compliance barrier now gone, export duties halved, and the infrastructure already in place, Indian exporters have everything they need to move aggressively when the arb opens.

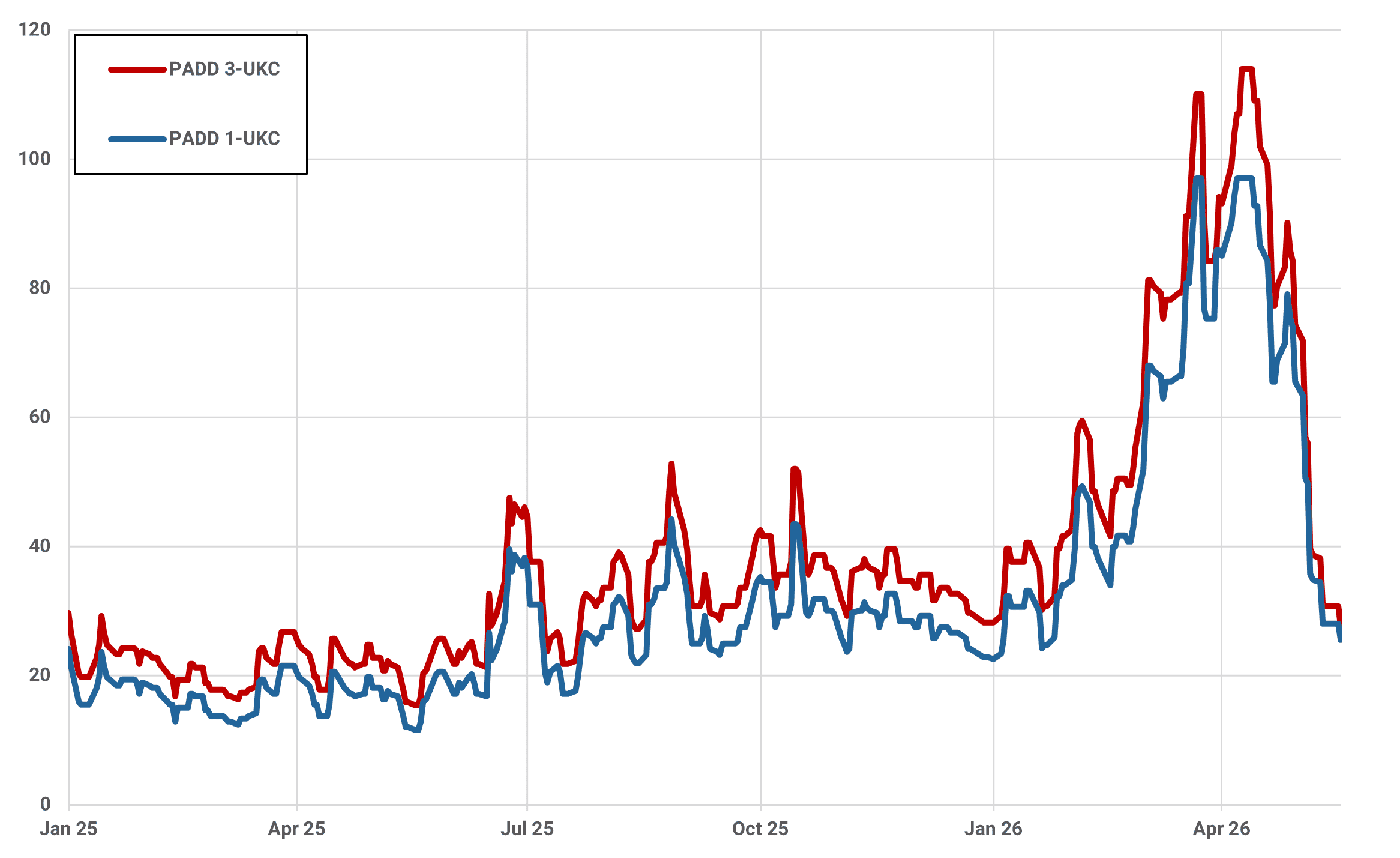

Transatlantic MR freight rates ($/t)

Source: Argus

Diesel is a more nuanced situation. The LR2 route from East of Suez into Europe was already functionally constrained before this license, given infrastructure limitations. Diesel distribution across the UK relies on a fragmented network of smaller terminals with many having vessel size constraints well below LR2s. Shipping economics from India require scale — without a comparable deep-water discharge point, the GTL notionally opens a route that the physical market cannot efficiently exploit. The real diesel supply remains MR-sized cargoes from the US Gulf Coast, and it is there — not in any new eastern arb — that the opportunities lie. Atlantic MRs have cratered, and with European diesel imports now predominantly an MR story, that freight weakness is transmitting directly into delivered prices.

See why the most successful traders and shipping experts use Kpler