Bucking the trend: Why China is still building stocks amid global supply disruptions

While Middle East conflicts have forced a global inventory drawdown to offset supply disruptions—particularly in the Asia-Pacific, where onshore stockpiles have shed roughly 1.6 mbd since mid-March—China has emerged as a notable outlier, trending in the opposite direction.

Key Takeaways:

- China’s onshore crude inventory has increased by a minor 8 mb in April, even though its seaborne imports have fallen by 2 mbd.

- The apparent discrepancy likely comes from unobserved inventory movements, a higher-than-expected refinery demand reduction, and underestimated domestic production.

- The resilient inventory offers China buffers to cope with a prolonged Middle Eastern war and more influence in physical oil pricing.

- This reinforced energy position provides Beijing with significant strategic flexibility, reducing its exposure to global supply-chain shocks during the upcoming Xi-Trump meeting.

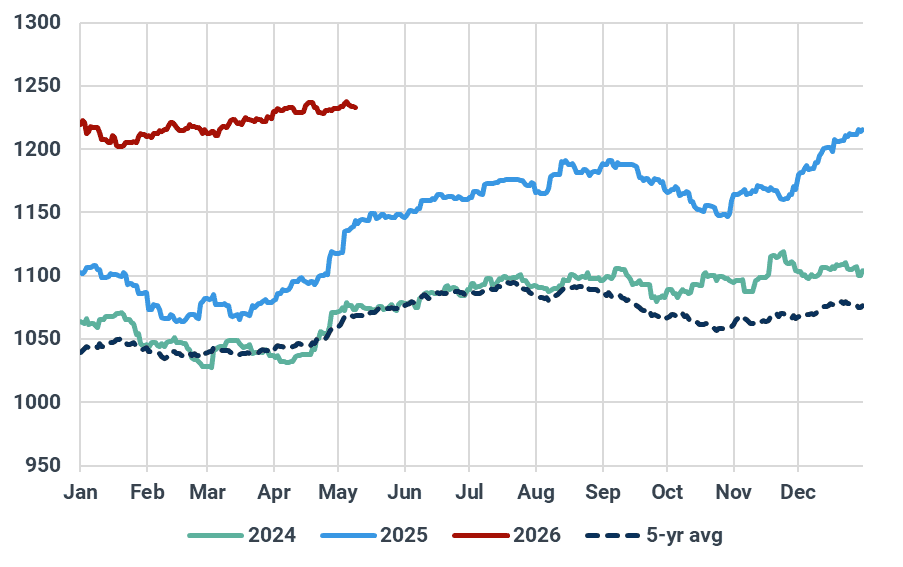

Kpler data shows that China’s onshore crude inventories stood at 1,232 mb at the end of April and have remained at this level since, compared to 1,217 mb in mid-March when seaborne imports first began to ease. During this period, China’s seaborne crude imports—including volumes via Myanmar’s Maday Island—declined from 11.7 mbd in February to 10.5 mbd in March, and further to 8.4 mbd in April.

While supply tightness led us to revise China’s refinery runs down to 14.7 mbd in March and 14.2 mbd in April (from 15.7 mbd in February), this reduction in throughput appears insufficient to offset the steeper decline in imports. While this partially explains why inventories haven't plummeted, it fails to account for the actual build observed during this period.

China's onshore crude inventories, mb

Source: Kpler

So, what might explain this apparent discrepancy?

Assumption 1: Pre-war inventory levels may have been underestimated

China’s onshore inventories—particularly State Petroleum Reserves (SPRs) and government-controlled commercial stocks—remain a closely guarded secret in Beijing. Official transparency has been sparse: the last public update on the locations and availability of China’s oil reserves was released in 2017. Later, in 2019, officials disclosed that total reserves were equivalent to roughly 80 days of demand (likely referring to net imports), though exact volumes were withheld.

At Kpler, we estimate China’s underground storages by integrating proprietary cargo tracking, refinery analytics, and observable onshore data. However, as these assessments rely on a confluence of modelled inputs, our figures may lag in capturing real-time fluctuations or accounting for newly commissioned sites—particularly as Beijing no longer discloses the locations or operational timelines of new storage facilities.

That said, our China crude balance showed an average oversupply of 780 kbd between September 2025 and February 2026, implying roughly 140 mb of “unaccounted” oil. This surplus suggests we may have underestimated either domestic refinery throughput or the pace of onshore stock building during that period.

This likely led to a higher inventory baseline prior to the Middle East conflict than our data reflected. Consequently, the currently observed trend would, in fact, point to a degree of stock drawdown in March and April as that unrecorded surplus is consumed.

Assumption 2: Potential reallocation from underground to overground inventories

As mentioned, our underground stock estimates may not mirror real-time movements as accurately as overground floating roof tanks. Therefore, if oil were withdrawn from underground facilities and moved overground for easier refinery access, we might capture the overground build without accounting for the underground draw. Consequently, our post-war inventory assessments could be higher than actual levels.

Currently, Kpler data assess China’s underground SPR at 100 mb, compared to 94.5 mb in early-March, with the increase coming from the newly launched Yunnan SPR.

Assumption 3: China’s crude refinery demand is lower than expected

While 815 kbd of primary refining capacity was shut down in March and 1.4 mbd in April according to IIR, Chinese refiners were also seen lowering run rates due to feedstock supply tightness and deteriorating margins. Some market participants told Kpler that state-owned refiners might be suffering from losses exceeding $30/bbl in crude processing; meanwhile, independent refiners see a slightly better picture due to more competitive feedstock prices, though most are also falling into the red.

In contrast to the “unaccounted” oil on the balance sheet in previous months, we now see a negative balancing factor of about 700 kbd in China for April. This suggests that the country would require more crude supply to support its refinery demand than what is currently assumed. This gap could be filled by an overlooked inventory drawdown and/or actual refinery demand coming in lower than we anticipated.

Several market participants told Kpler that the previously reported 1 mbd commercial stock release, originally expected to start in April, likely did not materialise, and the timeline could be pushed to June. If this information is authentic, it could help explain the observed Chinese inventory trend and the subdued crude throughput, as refiners are forced (or choose voluntarily) to further cut run rates to manage their stocks before receiving supplies from the national reserves.

Assumption 4: China’s domestic crude oil production is higher than anticipated

It is often overlooked that China is the world’s fifth-largest crude producer, and Beijing has been demanding that energy firms boost output to improve energy security. With CNOOC bringing several offshore projects online while CNPC and Sinopec optimize operations at existing oilfields in recent months, China’s crude oil and condensate production is assessed at 4.6 mbd for January-March 2026, which is 400 kbd higher than the same period in 2025.

While we anticipate China’s April output staying steady at about 4.6 mbd, the actual level could come in higher, offering an explanation for the inventory resilience. However, it should be noted that any increase in China’s domestic supply is likely to be marginal and unable to overturn the big picture.

Ultimately, it is difficult to determine which specific factors led to the resilience in observed onshore crude inventories—it is likely a confluence of all the aforementioned assumptions and other variables—as Chinese data and information remain highly opaque.

However, the data clearly suggests that China maintains a sizable buffer, providing a critical cushion should Middle Eastern supply disruptions persist. This fortified energy security not only secures domestic demand but also strengthens Beijing’s strategic leverage in upcoming Xi-Trump meeting.

In addition, elevated inventory levels offer Chinese refiners the option to push back against high physical crude premiums and wait for prices to retreat. This also allows Chinese firms to exert even more significant influence in the current market, where supply is tightening and demand is being eroded by high prices.

See why the most successful traders and shipping experts use Kpler