Russian barrels to fill Chinese crude stocks?

The prospect of Iran's sanctions being lifted, combined with prevailing low global oil prices, suggests that appetite could grow for stronger sanctions enforcement on Russian crude. The realignment of the Asian crude matrix for 2027 could be profound.

Key takeaways

- China's restocking opportunity: Heavily discounted Russian barrels could serve as the bedrock for China's strategic inventory refill as Beijing capitalises on the distressed supply overhang.

- India's diversification: The anticipated lifting of US sanctions on Iran and greater availability of Middle Eastern crudes could trigger a shift by Indian refiners away from Russian Urals.

- Direction: bearish on Russian Urals differentials; optimistic on Chinese onshore crude inventory builds.

We have previously written about the prospect of the market ending 2026 with unsanctioned Venezuelan and Iranian crude, and with Asian buyers feeling less pressure to abide by Russian sanctions. Price will be the main driver of Asian buying decisions in a post-war world.

But India could return to its prewar stance of 'diversification' away from Russian oil in the name of sanctions compliance, a stance that would become easier with free trade of Iranian barrels and resumed access to other Middle Eastern crude.

Meetings have already taken place between Iran's National Iranian Oil Company (NIOC) and Asian energy ministries, exploring the possibility of renewed oil trade once sanctions are fully lifted — past the 60-day waiver under the current memorandum of understanding (MoU). Some purchases could take place sooner, but it is also contingent on banking sanctions being lifted on Iran.

In an oversupplied market that weighs on prices, lifting sanctions on Iranian crude could come hand-in-hand with tighter enforcement of sanctions on Russian oil trade.

As a result, Indian refiners may be pushed to buy more Iranian barrels in Q3-Q4, in place of Urals — the baseload Indian grade for four years now. India imported 1 mbd of Russian crude in February, but that volume reached an all-time high of 2.5 Mbd in June.

Before the geopolitical disruptions of the early 2020s, Iran was a foundational supplier to India; a return to this traditional baseload will systematically back out Russian volumes. To retain market share in a shrinking addressable market, Russian exporters will be forced to aggressively slash Urals differentials.

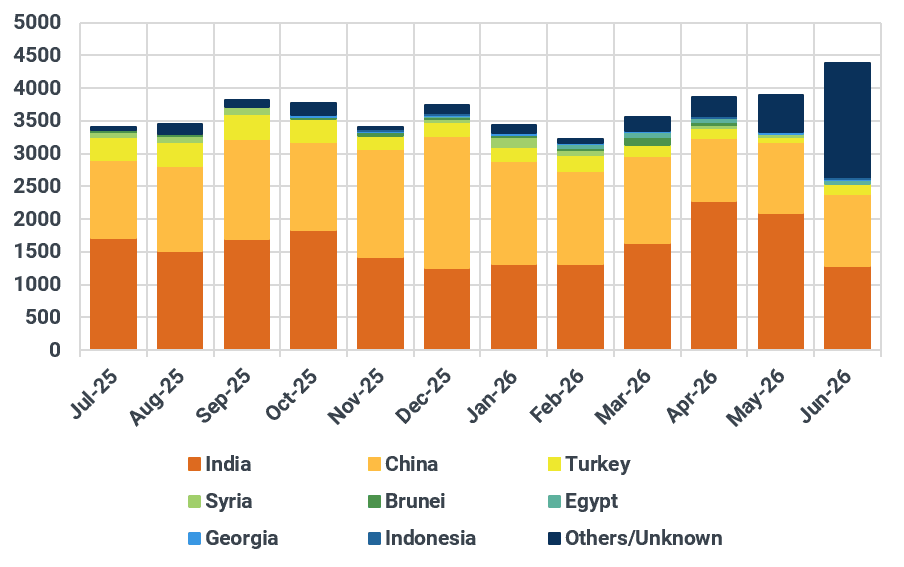

Exports of seaborne Russian crude oil by destination, kbd

Source: Kpler

Compounding this bearish pricing pressure on Russian grades is a structural increase in crude export availability. A renewed volley of Ukrainian drone attacks has inflicted severe and sustained damage on key Russian downstream infrastructure. With domestic refinery intake heavily curtailed by offline distillation units, excess crude is being forced out of the country and onto the seaborne export market.

At least 400kbd of additional spare export capacity is still available unless Ukraine intensifies attacks on export and transport infrastructure. However, because Russia's energy industry has gained experience in restoring operations after attacks, any increase in exports may be sporadic and short-lived.

This surge in available Urals and ESPO volumes could collide with a rise in unsanctioned Iranian exports (upside to around 2 Mbd in the short term) creating an acute, highly localised supply overhang for Russian sellers.

This dynamic clears the path for China to act as the primary clearinghouse for distressed Russian crude. This was the case in late 2025, when the US imposed more sanctions on Russian entities. While Chinese independent refiners operate under strict government-mandated import quotas, the sheer depth of the impending Urals discount will heavily incentivise maximum quota utilisation.

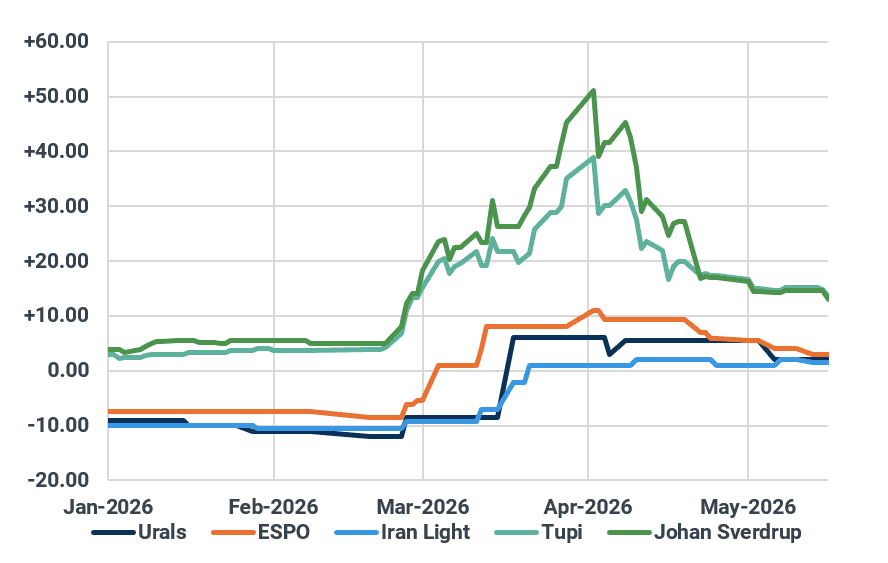

Selected grades DES diffs against ICE Brent, Shandong basis, $/bbl

Source: Argus Media

ESPO flows to China have already moved higher as the grade dropped in valuation by around $4/bbl on a delivered-China basis for July arrival. June imports of Russian crude by China were up 130kbd on the month.

More importantly, these heavily discounted Russian barrels are well placed to become the bedrock of China's strategic inventory refill. Following aggressive stockpile drawdowns earlier in the year designed to cool global flat prices, Beijing now has both the storage capacity and the economic incentive to absorb any excess Russian barrels.

Ultimately, Russian flows could realign toward the Chinese market and away from India, with Urals prices falling sharply. The prospect of sanctioned Russian oil filling Chinese inventories also limits the upside that inventory-refill demand could otherwise lend to prices (because of the sanctions).

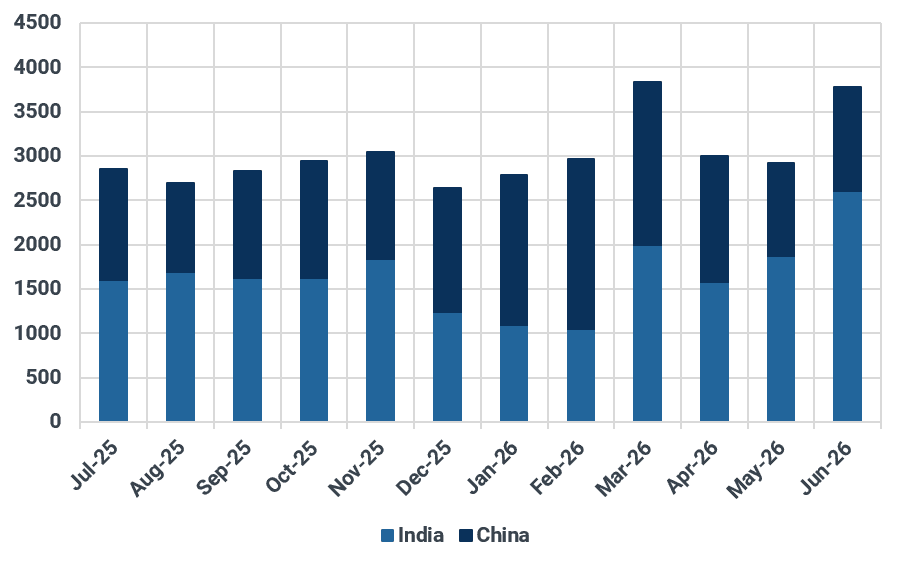

India and China seaborne imports of Russian crude, kbd

Source: Kpler

See why the most successful traders and shipping experts use Kpler