Russian wheat exports constrained following Ukrainian attacks

Continued Ukrainian attacks on Russian vessels in the Sea of Azov have led to an indefinite suspension of trade through the sea. As a result, one-third of Russian wheat exports may become bottlenecked depending on how long the suspension lasts. Rival exporters, such as the EU, may find short-term demand. Retaliatory attacks pose a significant threat to already limited Ukrainian export capacity.

Russian export capacity restricted

On Friday, Russia temporarily suspended shipping through the Sea of Azov and the Kerch Strait following Ukrainian attacks on several vessels, including tankers, bulkers, and tugboats. Currently, it is not known when the suspension will be lifted, and local reports suggest both ports in Rostov and Taganrog are no longer taking grain deliveries. Russia has since retaliated, including heightened strikes across the Odessa Oblast, a key region for Ukrainian exports.

The Sea of Azov is significant for Russian exports

All Russian grain trade originating from the Sea of Azov would transit through the Kerch Strait. Given the shallow water ports, the purpose of these vessels is mostly for transhipment, which typically occurs on the Black Sea side of the Kerch Strait at Taman or the Kavkaz anchorage. Some of these coaster vessels also deliver to nearby destinations in the Mediterranean and Black Seas, mainly to ports in Türkiye.

Despite the relatively smaller cargoes, the volume of shipments that originate in the Sea of Azov account for approximately one-third of seaborne Russian wheat exports. At its peak, monthly exports out of the Sea of Azov can account for over 1.5 Mt of wheat, which can be close to the same volume seen by the largest exporting port Novorossiysk. However, monthly exports usually trend lower by a greater extent as the marketing year progresses, seeing it lose export share.

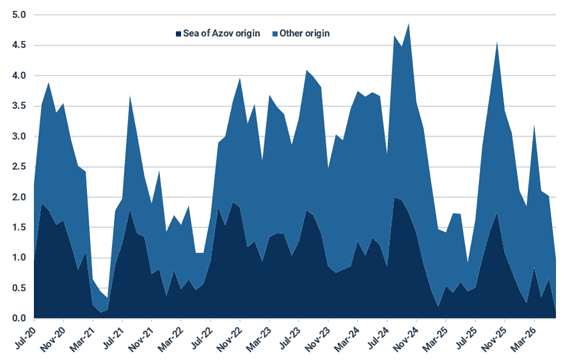

Seaborne Russian wheat exports by origin (Mt)

Source: Kpler

Therefore, the timing of this event coincides with the seasonal peak of exports and will have a stronger impact than if this had occurred in the second half of the marketing year. For wheat, which is the predominant commodity affected, from harvest in July until Oct-Nov, exports depend on full capacity utilisation across all Russian ports in the region. This includes Kavkaz anchorage, which is the second busiest grain export ‘port’, after Novorossiysk. Loss of capacity utilisation at Kavkaz cannot be made up elsewhere, and each day of the suspension will subtract from Russia’s exports in Q3.

A slowdown in Russian or Ukrainian Black Sea grain exports would put further downward pressure on earnings in an overtonnaged Black Sea and Mediterranean Handysize market. Vessel availability there has consistently exceeded the year-ago level, and it was hoped that Russian wheat chartering would help to clear out some of these ships.

Constrained Russian exports will dislocate trader and exporter pricing

Given Russia historically outcompetes alternate exporters at this time of year, the tighter exportable capacity is likely to cause slightly softer competitiveness. FOB offers for Russian wheat (12.5% protein) have risen, partially driven by short covering. As had been witnessed last year, this could serve as an advantage for the EU, which could capture greater market share across the Middle East, North Africa and Sub-Saharan Africa.

Although Russian supply is not lost, it is only restricted through this channel. So, given the uncertain outlook for when exports through the Sea of Azov can return, efforts will be made to redirect grain towards Black Sea ports. However, in practice, this is not easily accomplished given existing capacity. The rerouting would leverage on trucking and railroads.

Russian Railways, the state-owned rail network, is introducing a 38% discount on grain and legume exports heading south along the International North-South transport corridor via the Samur border crossing and Azerbaijani-Iranian route until June 2027. This could partially help to support the outlet of Russian wheat, though as the global reach is limited the impact is likely minimal, with a modest net loss to international seaborne trade. So, it is more probable that there will be elevated interest in utilising the rail network to Novorossiysk. For trucking, rates have since strongly increased and will discourage farmer selling. Trucking and rail capacity was already under pressure given chronic diesel shortages across Russia, so may not be in a position to completely accommodate the redirection of trade away from Sea of Azov ports.

Furthermore, Black Sea port terminal capacity would not be sufficient in storing the abundance of grain from districts further north. For Novorossiysk, the deep-sea port which accounts for over 50% of total Russian wheat exports has a total storage of 0.6 Mt. So, for most months of the year, the port is generally exporting at least two times its storage capacity under usual conditions. The storage capacity for the alternate Black Sea port Tuapse is not much greater at 0.1 Mt.

Therefore, the lost export capacity can’t be offset elsewhere. Russia’s exportable wheat surplus will face a bottleneck during the suspension of exports via the Sea of Azov, which will be of greater intensity given the time of year. For Russian farmers looking to market their wheat crop, particularly those outside of the Southern district, higher logistical costs and meagre domestic demand may be met with weaker offers from traders. So, those who can, would look to store in hope for a better price later in the season.

Russian wheat exports (Mt)

Source: Kpler Insight

Ukrainian exports may come under further pressure

Since the beginning of the year, Russian drone strikes on Ukraine have been continuing to increase w/w, reaching their highest levels since the start of the war. Following the recent Ukrainian response, President Putin is threatening stronger retaliatory strikes.

Ukrainian export pace has already been under significant constraint, with ports seemingly prioritising corn over wheat given market demand and relative competitiveness. As a result, Ukrainian wheat stocks have surged higher. The reestablishment of EU TRQs on Ukrainian imports was of significant impact on wheat. The TRQ sees 1.3 Mt duty-free, then subsequent volumes are subject to a €95/t duty, which acts as a de facto ban.

Ukrainian wheat stocks by 1 June (Mt)

Source: State Statistics Service of Ukraine

So, with Ukraine no longer able to export as much wheat to the EU, the arrival of further attacks on export infrastructure will continue to impede export capacity. Depending on the extent of damage caused, this could see further export demand for EU wheat should Ukraine be unable to safely load and transport cargoes out of the Black Sea.

Indefinite export suspension casts an uncertain outlook

Given the currently uncertain outlook for how long trade originating from Sea of Azov will be suspended for, the impact on the wheat market is not yet understood. Should the suspension be lifted in the coming days, this would alleviate the stockpile build-up as harvest progresses. However, a longer suspension could shift the initial peak of monthly Russian wheat exports to Q4, a trend that was seen last year. So, while major exporters could see some uptick in demand in the short-term, this would effectively be in substitution for demand later in the marketing year. The cost of doing business in the region will remain higher as owners demand elevated risk-related premiums on hire rates and insurance costs increase to reflect recent attacks.

See why the most successful traders and shipping experts use Kpler