Flows over economics: Supply risks drive global crude flows | The Arb View

Supply disruptions across the Middle East and Russia are tightening global crude availability, pushing refiners to secure alternative barrels despite weakened arbitrage economics. This is driving stronger demand for Atlantic Basin and US grades, with WAF differentials firming and record volumes of Midland and select US sour barrels moving east.

Executive summary

Arbitrage Values (30/03/2026 07:00 UTC)

Source: Kpler

Trading Calls

- Bullish WAF diffs as limited supply and softer freight will encourage refiners to bid up prices as they scramble for alternatives for disrupted MEG supply.

- Neutral to slightly bearish Brent–WTI spread. Brent should continue to carry the geopolitical premium, but stronger export demand for Midland is likely to keep WTI supported, putting mild narrowing pressure on the spread.

Middle East and Asia: Houthi, Ukraine attacks pose further supply risk

Price action last week remained highly reactive, with the market quick to respond to headlines. Trump’s Truth Social post on Monday triggered a sharp $17/bbl drop before prices retraced, underlining ongoing uncertainty around any near-term resolution. The Brent–Dubai EFS has widened further to around $13/bbl, although the move increasingly looks sentiment-driven rather than a reflection of additional physical tightening.

We currently estimate around 11.4mbd of MEG crude supply disruption, with additional outages now beginning to emerge from the Baltics. Ukraine has stepped up attacks on Russian energy infrastructure, taking roughly 550 kbd from Ust-Luga offline, including around 300 kbd typically flowing to India. With no exports reported since the 23rd, any prolonged outage will force Reliance and IOC to look beyond their usual slate.

LatAm grades such as Castilla, Vasconia and Payara Gold are becoming more relevant. Castilla in particular is starting to work, with complex margins around $14/bbl, up roughly $4 m/m on firm middle distillate cracks. Reliance has already imported around 4mmbbls of Castilla last month following a one-year hiatus, highlighting how quickly Indian refiners can adjust sourcing. Diffs have remained relatively stable at around an $8/bbl discount to Brent Futures, still landing cheaper than alternatives such as Dalia and Hungo. That relative value should keep LatAm sours supported, especially with Chinese refiners competing for similar barrels.

Meanwhile, there are early signs of flows being negotiated on a bilateral basis, with Iran reportedly granting passage to countries such as India and Thailand. This may allow selective access to MEG cargoes, but without consistent tanker movement it is difficult to argue that the Strait is meaningfully open. At the same time, Houthi threats around Bab el-Mandeb add further constraints, limiting Saudi exports via Yanbu and restricting Med barrels moving out of Ain Sukhna. This keeps the EFS supported and leaves most West-to-East arbs uneconomic on paper.

Landed Values of Selected LatAm Grades

Source: Kpler

Atlantic Basin: North Sea Tightens as Asian & European Refiners Bid Up

The North Sea remains tight as Asian and European refiners compete for a shrinking pool of prompt barrels. Unipec has fixed a Forties Suezmax East, likely leveraging an arb that had been open for several weeks but the move also highlights the strength of prompt demand. DFL has pushed to around $11/bbl, up roughly $5/bbl w/w, underlining how tight physical is relative to paper. At these levels of backwardation, holding barrels becomes punitive, forcing buyers into the spot market.

While prompt pricing should remain supported on limited supply and steady refining demand, a sustained pickup in Eastbound North Sea flows still looks unlikely given freight risk and exposure over longer voyages.

The Atlantic Basin is also being leaned on to partially offset the MEG shortfall. Nigerian light sweets are becoming more attractive into Europe, offering suitable quality and workable economics relative to North Sea alternatives. Freight has increased by around $2/bbl w/w, which will weigh on margins, but strength in North Sea differentials should keep the arb open. Johan Sverdrup, CPC and other key grades are trading near highs, with Sverdrup clearing around $13/bbl, keeping the broader Atlantic pool tight.

Looking ahead, the pull between West and East is one to watch. Bonny Light is now generating around $13/bbl in complex margins in the east, up roughly $9/bbl m/m, which should keep refiners bidding for WAF barrels. Meanwhile, supply remains limited as NNPC struggles to even meet term deliveries to Dangote, supplying only around 5 of the expected 15 cargoes per month. With supply constrained and demand holding, WAF differentials should stay supported and likely push higher.

Bonny Lt Arbs West Vs East (NWE-Ningbo)

Source : Kpler

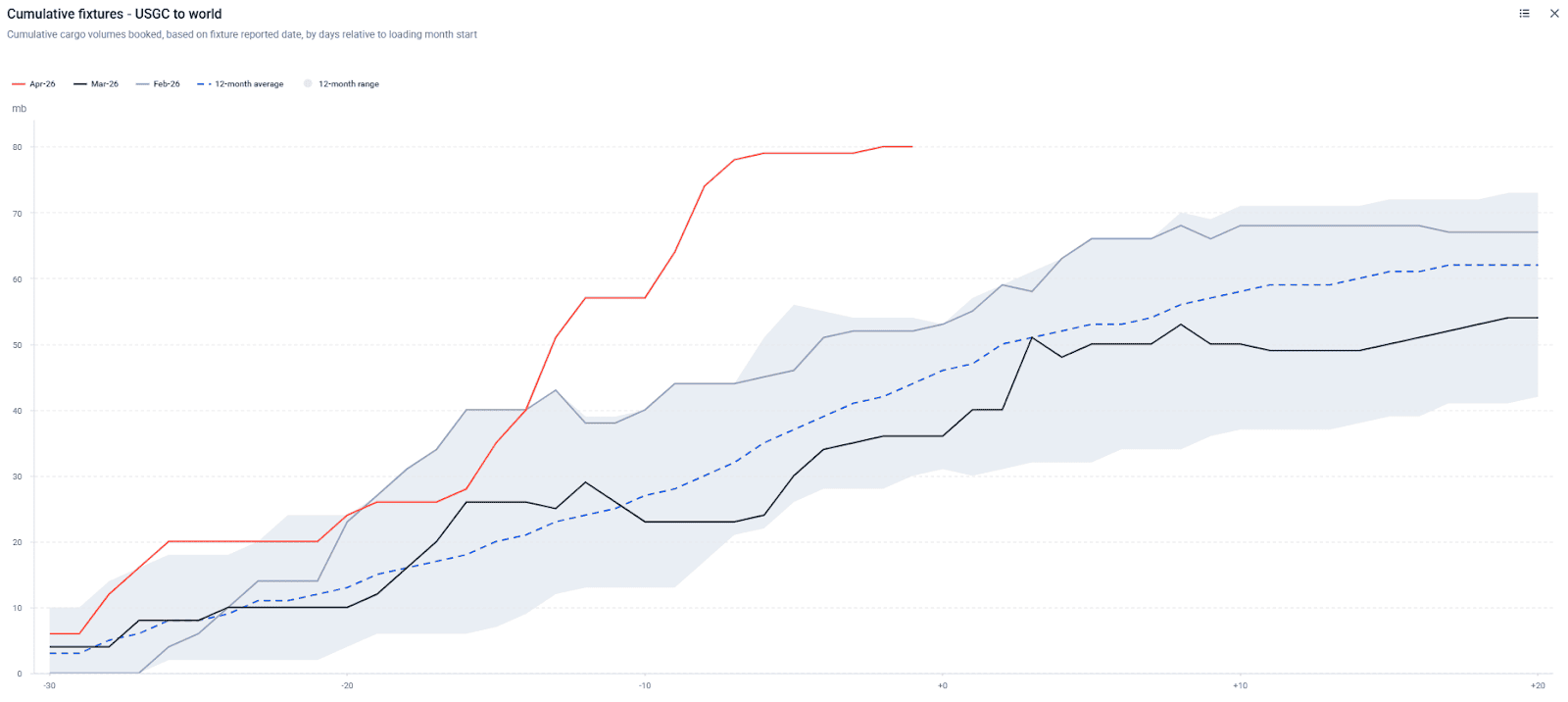

Americas: Record Midland Cargoes Head East as US Becomes Swing Supplier

US crude is tightening into the global system, with export pricing strengthening alongside Brent and reinforcing its role as one of the few scalable supply sources. US exports to Asia are set to hit record highs for April loaders, with close to 50 mmbbls expected — more than double typical levels. China appears as the main buyer on paper, although some cargoes are likely to be redirected toward South Korea and Japan depending on refinery demand.

That strength is feeding into Midland differentials, with WTI Midland FOB USGC now trading close to $3/bbl over May WTI futures, up roughly $1 w/w and the highest in over four years. The Brent–WTI spread remains the key signal to watch. As long as it holds at these levels, Midland should continue to clear into a wide range of refineries.

On the sour side, grades like Mars are moving when available, given their ability to substitute for Middle Eastern barrels. Chevron has recently shipped a co-loaded cargo of Midland and US sour crude to Yeosu aboard the VLCC Glasgow Voyager, the first such trade since April 2024. With the cargo loading out of LOOP, it is likely Mars, pointing to the re-emergence of US sour grades into South Korea. These flows should persist while disruption in the Strait continues, despite elevated TD22 freight. On our arb view, Mars is landing at roughly $30/bbl over Dubai, roughly $13 w/w increase, reinforcing tight US sour availability.

Cumulative Fixtures - USGC to all destinations

Source : Kpler

Kpler Arbitrage

Kpler’s Arbitrage platform turns complex freight, quality, and benchmark data into simple, actionable arbitrage insights so you can discover value windows, rank opportunities, and build scenarios confidently. With Arbitrage you can:

- Compare delivered crude values by region and freight cost

- Quantify refining margins and route profitability

- Spot open arbitrage opportunities quickly

- Breakdown value drivers like FOB differentials, spreads, and freight

- Model scenarios with custom market inputs

See why the most successful traders and shipping experts use Kpler