Hormuz reopening optimism shifts sentiment, but flows stay constrained | The Arb View

Reopening optimism has softened crude prices, but flows through Hormuz remain constrained, keeping underlying prompt tightness intact. Atlantic Basin differentials are starting to ease on weaker refinery demand and reopening expectations, though downside should be gradual with flows still limited. In the Americas, Midland arbs are improving and supporting flows to Asia, but logistical constraints are likely to cap further upside in exports.

Executive summary

Arbitrage Values (20/04/2026 06:30 UTC)

Source: Kpler

Trading Calls

- Neutral to moderately bullish Atlantic Basin sours: Asian diversification should support demand, offsetting reopening optimism and weaker prompt refinery demand.

- Bearish WAF diffs: Weaker European and Asian demand should pressure premiums that look unsustainably high.

Middle East and Asia: Asian Procurement Shifts as Flows Remain Uncertain

June Brent futures settled at $90.38/bbl on Friday, the lowest in over a month, as markets reacted to Iran’s announcement on a potential reopening of the Strait of Hormuz. That move has already started to unwind, with Brent back up to around $95 following a re-closure over the weekend and no meaningful vessel activity. With flows still constrained, the market remains sentiment driven, but underlying tightness persists. We expect prices to recover modestly, though upside should be more measured as early signs of flow resumption cap gains. The Brent-Dubai EFS is likely to widen back toward a $10–15/bbl range this week unless there is a clear resolution.

On the physical side, the reaction is more muted. Murban differentials are unlikely to spike given disruption had already been priced in, while Asian refiners have cut runs, delaying any recovery in demand. At the same time, roughly 125mmbls of crude has built up in the Gulf, which could weigh on prompt demand if flows resume, limiting upside in diffs.

Refiners could shift back to landed economics from here. Midland remains a key swing barrel and is becoming more attractive into Asia after the recent softening in diffs. While still fetching about 40c lower gross margins than Murban, it remains viable as a blending component, particularly with softer freight and FOB values supporting optimisation of trade routes, including shorter hauls via the Panama Canal. That said, the ability of US barrels to continue scaling into Asia may face logistical constraints, which could limit how much incremental displacement of Middle Eastern grades occurs in the near term, as discussed further in the Americas section.

Looking ahead, supply diversification is likely to remain a key theme. Even if Middle East flows normalise, Asian buyers are expected to keep some exposure to Atlantic Basin barrels. Japanese and South Korean refiners in particular are likely to continue pulling Midland when economics allow, reinforcing a gradual shift toward non-Dubai linked alternatives and greater flexibility in crude sourcing.

Brent-Dubai EFS M1

Atlantic Basin: Medium sour weakness builds on reopening optimism, but risks remain

The potential reopening of the Strait should offer some relief to European refiners, who have been under pressure from weak margins. Simple and medium complexity refineries have been running at losses of around -$20/bbl and -$9/bbl respectively, while deep conversion units are only just around breakeven. Forties differentials have corrected sharply, falling to $13.90/bbl vs spot Dated on Friday from around $21/bbl earlier in the week. While this reflects expectations of easing tightness, refiners will likely need to see lower and more stable prices before considering any meaningful increase in runs.

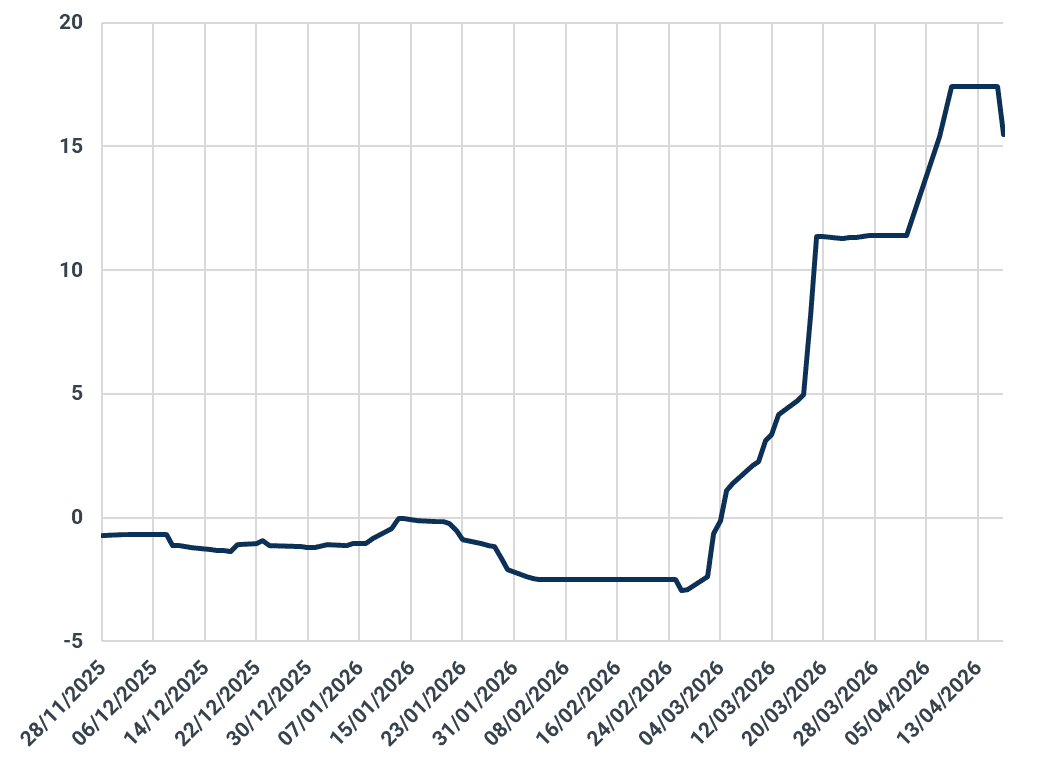

Medium sour diffs have reacted first, given their role as the closest substitutes for Basrah and Arab Medium. Johan Sverdrup has come off by around $2/bbl, although it remains elevated above $15/bbl and still looks expensive on a historical basis. That said, the move so far appears largely driven by optimism around a reopening rather than fully normalised flows. With physical movements still constrained and visibility limited, any downside in diffs is likely to be gradual and could prove short-lived if disruptions persist.

Further softening across the European medium sour complex should start to limit the Westbound pull for LatAm cargoes. The LatAm arb into NWE, which widened by around $6/bbl w/w to ~$17/bbl, is likely to begin narrowing as Johan Sverdrup diffs ease and refiners trim runs into May. That does not necessarily translate into weaker prompt demand, as Asian refiners are likely to absorb excess supply, with more LatAm barrels instead moving East.

WAF also looks exposed. Differentials for grades such as Bonny Light, Jubilee and Escravos have held above $7/bbl, but that looks difficult to sustain if Middle East supply improves and Asian demand softens. Indonesia should provide some support through term liftings, but flows are likely to become more regional, with shorter haul outlets such as Nigeria’s 650 kbd Dangote refinery and Ghana’s 120 kbd Sentuo absorbing a larger share, supported by freight economics.

Johan Sverdrup Diffs vs Dated

Americas: US crude demand surges, but logistical constraints may cap flows

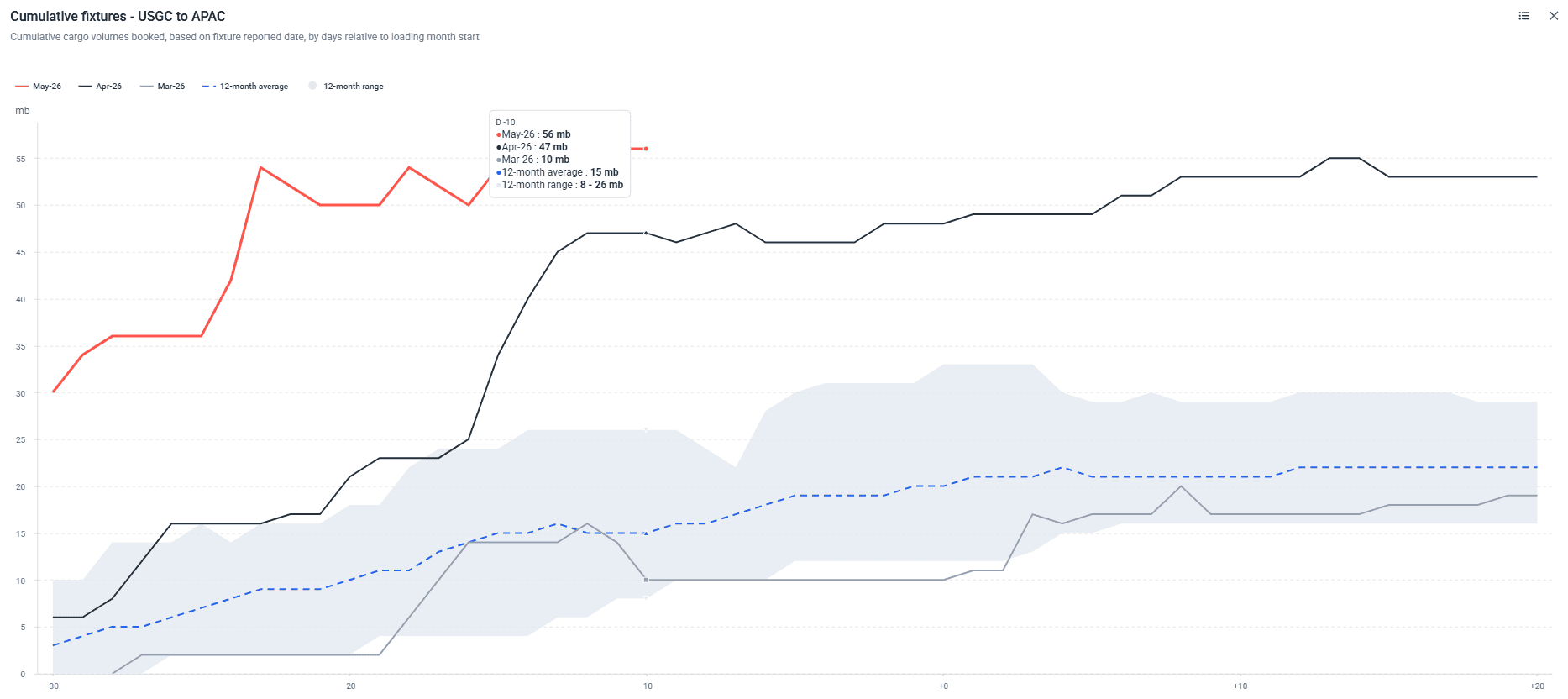

US crude is increasingly acting as the marginal barrel, with export demand strengthening amid disruptions to Middle Eastern supply. The WTI-Brent June spread is around -$7/bbl, attracting strong buying from both Europe and Asia. Flows to East Asia reached a record ~1.1mbd last month, with Japanese refiners leading Midland purchases. Early fixtures for May show a similar trend, with around 56mb already fixed, roughly 4 times the 12-month average.

Demand has been supported by improving arb economics, with all-in costs easing by around $2/bbl m/m. That has kept Midland workable into Asia, particularly as a blending component alongside heavier barrels such as SPR releases or ANS.

However, the pace of flows is likely to run into logistical constraints. A heavy concentration of inbound tankers, including a large number of VLCCs, is expected to strain USGC port capacity, increasing the risk of congestion and delays. That effectively raises delivered costs and delays potentially extending several days. This should act as a natural cap on how quickly exports can scale, even with firm demand.

At the same time, the broader geopolitical backdrop remains mixed. Ongoing restrictions on Iranian exports continue to tighten global balances, supporting demand for alternative barrels. However, any sustained de-escalation or easing of Middle Eastern disruptions could reduce the urgency for replacement flows. In this context, US crude should remain structurally supported, though there is some downside risk to diffs and long haul arbitrage flows if supply from the region begins to return.

USGC to APAC Cumulative Fixtures

Source: Kpler

Kpler Arbitrage

Kpler’s Arbitrage platform turns complex freight, quality, and benchmark data into simple, actionable arbitrage insights so you can discover value windows, rank opportunities, and build scenarios confidently. With Arbitrage you can:

- Compare delivered crude values by region and freight cost

- Quantify refining margins and route profitability

- Spot open arbitrage opportunities quickly

- Breakdown value drivers like FOB differentials, spreads, and freight

- Model scenarios with custom market inputs

See why the most successful traders and shipping experts use Kpler

.jpg)