Japan LNG demand raised on lower gas-fired efficiency; Hormuz disruption reinforces bullish bias

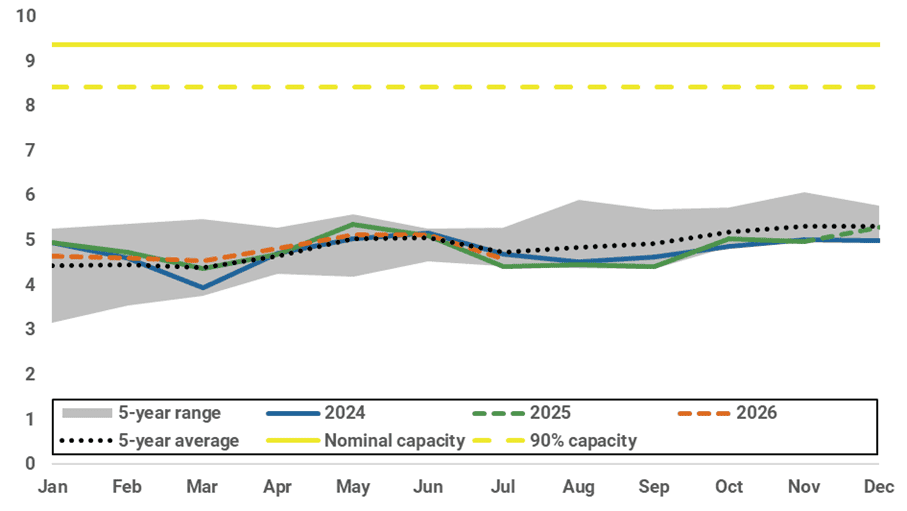

Japan’s 2026 LNG demand forecast has been revised up by 0.6 mt to 64.9 mt, as stronger gas-for-power demand more than offsets weaker non-power consumption. With rising renewable penetration expected to lower gas-fired efficiency and lift LNG burn, the revision implies 8-10 incremental cargoes through Q2-Q3, tightening Pacific basin balances during the Asian summer. Although total inventories are expected to rebuild from 4.8 mt at end-April and hold around 5.1 mt through May-June, the stronger gas-for-power outlook and geopolitical risk from a prolonged Hormuz disruption reinforce a bullish bias for Asian LNG prices in Q2 and Q3.

- Japan LNG Demand: Increase, with 2026 demand raised by 0.6 mt to 64.9 mt as stronger gas-for-power demand outweighs weaker non-power gas demand.

- Asia LNG prices: Slightly bullish in Q2 and Q3, as Hormuz disruption risk drives a geopolitical premium, outweighing comfortable Japanese inventories; further upside if disruption persists and Atlantic replacement demand intensifies amid hotter-than-usual Asian summer.

Stronger gas-for-power demand outlook on lower gas-fired efficiency

Latest data from Japan’s Ministry of Economy, Trade and Industry (METI) show Japan’s total power generation rose 4.3 TWh y/y to 94.2 TWh in January 2026, supported by electrification trends and higher renewables output. Solar, wind and geothermal generation increased 3.5 TWh y/y to 13.1 TWh, while biomass rose 0.5 TWh y/y to 6.1 TWh. To balance higher intermittent renewables output, LNG-fired generation climbed 1.7 TWh y/y to 29.6 TWh. Alongside warmer Q1 2026 temperatures, these gains offset a 2.2 TWh y/y decline in coal generation. As a result, January gas-for-power demand rose 0.3 bcm y/y to 5.1 bcm, while power-sector implied LNG inventories fell 0.4 mt m/m to 2.6 mt, in line with our previous forecasts.

Looking ahead, higher renewables output is expected to drive more frequent gas-fired ramping, weighing on LNG fuel-burning efficiency. Combined with weaker baseload solar contribution amid rainier Q2 weather, lower-than-expected gas-fired efficiency is set to lift LNG fuel demand for power generation. As a result, Kpler Insight has revised up 2026 gas-for-power demand outlook to 49.2 bcm, up 0.7 bcm y/y.

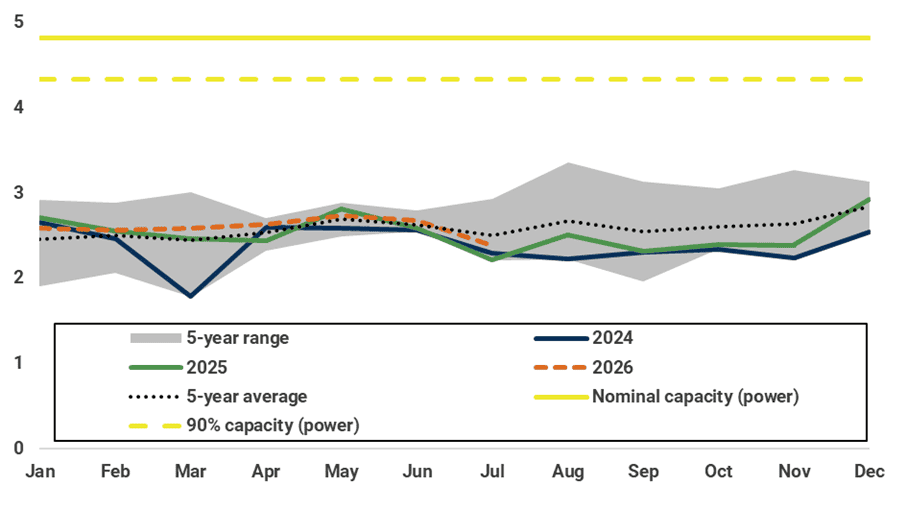

Despite the stronger gas-for-power outlook, higher nuclear availability following the restart of Kashiwazaki-Kariwa Unit 6 is expected to cap further upside. Power-sector LNG inventories are forecast to rebuild slightly from 2.6 mt at end-April and hold ~2.7 mt through May-June, broadly in line with seasonal norms.

Weaker non-power gas demand outlook amid macroeconomic headwinds

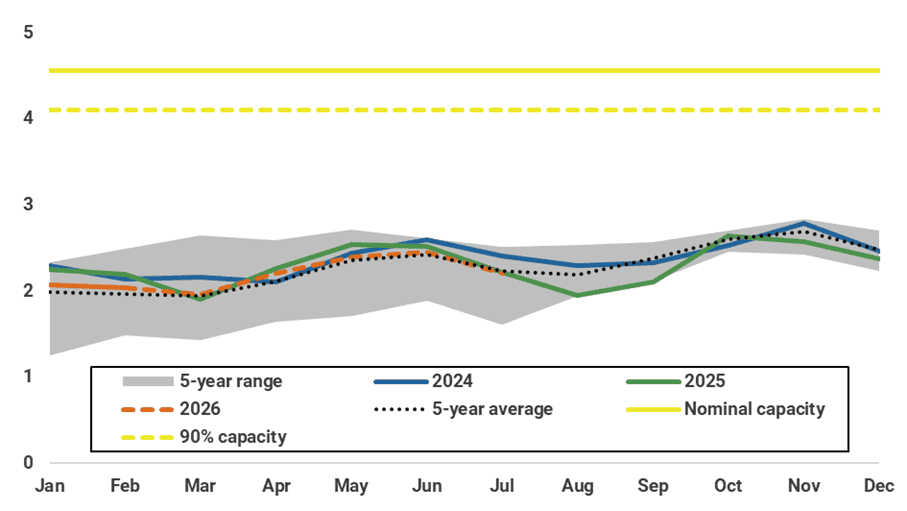

Japan’s February 2026 METI data show non-power gas demand edged 0.1 bcm lower y/y to 3.9 bcm, reflecting softer industrial gas consumption amid narrower manufacturing and industrial exports. Non-power LNG inventories held stable m/m at 2 mt, in line with expectations.

Looking ahead, Kpler Insight has revised Japan’s GDP growth outlook down by 0.2 percentage points to 0.6%, as sustained high energy costs amid the US-Iran conflict point to a weaker macroeconomic outlook. As a result, non-power gas demand has been revised slightly lower to 38.1 bcm, down 1.1 bcm y/y, with industrial activity expected to continue moderating.

Overall, as stronger gas-for-power demand largely offsets weaker non-power gas demand, Kpler Insight revises its 2026 Japan LNG demand outlook up by 0.6 mt to 64.9 mt, implying 8-10 incremental cargoes through Q2-Q3.Hotter summer conditions and weaker solar output are expected to lift thermal power demand for cooling and increase reliance on LNG-fired generation, tightening Pacific basin balances and reinforcing upward pressure on Asian LNG spot prices.

With limited direct exposure to Hormuz-linked disruptions (~0.1 mt/week), Japan’s total LNG inventories are expected to rebuild from 4.8 mt at end-April and hold around 5.1 mt through May-June, tracking seasonal averages and providing a short-term buffer. However, a prolonged disruption would further tighten the global LNG balance, increase competition for Atlantic basin replacement cargoes, and embed a higher geopolitical premium in Asian spot prices.

Historical power generation by fuel type in Japan (TWh)

Source: METI, Occto, Kpler Insight. Note: LNG-fired & coal-fired generations over February-April 2026 are reported by Occto. For other generations, Kpler Insight forecast starts from February 2026 onwards.

Historical and forecasted monthly average gas-fired efficiency in Japan (%)

Source: METI, Kpler Insight

Japan monthly nuclear availability forecast by reactor (GW)

Source: HJKS, Kpler Insight. Note: Dashed area shows the assumed restart timeline and capacity availability of Kashiwazaki Kariwa 6

Japan’s gas-for-power demand (bcm)

Source: METI, Kpler Insight

Japan implied LNG inventory forecast for power companies (mt)

Source: METI, Kpler Insight

Japan’s non-power gas demand (Bcm)

Source: METI, Kpler Insight

Japan implied LNG inventory forecast for non-power companies (mt)

Source: METI, Kpler Insight

Japan implied total LNG inventory forecast (mt)

Source: METI, Kpler Insight

See why the most successful traders and shipping experts use Kpler