Metals vs fertilizers: Who pays more for sulphur?

One commodity, three industries, one constrained supply. Kpler maps who adjusts output, who has the margin to pay, and how the allocation dynamic plays out across copper, nickel, and fertilizers.

One commodity. Three industries. A question of margin.

Sulphur is one of the least visible inputs in global commodity markets. It moves quietly in granular yellow piles on bulk carriers and in tank vessels carrying sulphuric acid. Additionally, it underpins the production of copper cathode, battery-grade nickel, and the fertilisers that feed a significant share of the world's population. In a normal market, there is just about enough for everyone. In 2026, the supply picture has changed materially.

The Strait of Hormuz closure on 28 February, followed by China's sulphuric acid export ban on 10 April, has created a situation in which copper producers, nickel producers, and fertiliser manufacturers are competing for the same constrained supply. The question is not just who secures the cargo. It is who has the margin to absorb the cost, who adjusts production, and how Kpler's flow data makes the allocation dynamic visible.

The cost structure: sulphur is not equally painful for everyone

Before examining who wins the bidding war, it is worth understanding why the stakes are so different across these three industries. Sulphur is not a marginal input for any of them. But the percentage of total production cost it represents - and therefore the pain threshold - varies enormously.

For HPAL nickel, the shift has been particularly acute: sulphur's share of operating cost has moved from a historical range of 20–30% to 35–50% under current market conditions and for the most exposed plants, some estimates put that figure closer to 70%. That structural repricing of feedstock cost is what makes the current disruption qualitatively different from previous supply tightness events.

- MHP Nickel - HPAL

Sulphur is the dominant cost driver. At current prices, many Indonesian HPAL plants are running on tight margins in combination with the Indonesian domestic policy that makes things more difficult for the Nickel Ore production. No partial leach option, plants are either on or off.

- MAP/DAP Fertilizers

Enormous volume consumer, but thinner final-product margins than metals. Mosaic has already cut 2 mmt of domestic phosphate production rather than absorb the cost.

- Copper Cathode - SX-EW

Lower sulphur cost share, but the final product value is high enough that producers can absorb very steep feedstock prices. DRC producers are bidding significant premiums compared to other downstreams.

The paradox is immediate: HPAL nickel is most exposed in cost terms with acid representing 50–60% of MHP production cost, comparable to phosphate fertilisers. Yet copper, where sulphur accounts for roughly 12–18% of cathode production cost, is the most aggressive bidder.

Metals: integrated vs. non-integrated is everything

Not all metals producers are equal in this market. The critical divide is between integrated operations - which generate their own sulphuric acid as a byproduct of copper smelting - and non-integrated SX-EW and HPAL operations that must source acid and sulphur from the seaborne market.

- Integrated producers : effectively insulated

Codelco (Chile), Aurubis (Germany), Pirdop (Bulgaria) are copper smelters that generate sulphuric acid as a smelting byproduct. Their feedstock supply is internal and disconnected from seaborne acid prices. They are not buyers. In some cases - like Pirdop - they are now sellers, redirecting acid exports to Chile in a new arbitrage corridor.

- Non-integrated producers: fully exposed & bidding hard

BHP Escondida, Antofagasta, Ivanhoe (DRC), Huayou (Indonesia) - these operations must buy acid or sulphur from the seaborne market. The non-integrated copper producers in the DRC occupy a particularly powerful position: they face the highest acid prices in the world, but they also generate the highest-value copper cathode from their deposits. The result is that DRC copper operations can rationally bid at prices that are economically impossible for an Indonesian HPAL plant or a Moroccan fertiliser producer to match.

Fertilisers: the volume buyer who can't win on price

Here is the uncomfortable truth about fertilisers in this market: they consume sulphur at a scale that dwarfs metals. The global fertiliser industry - led by OCP, Mosaic, Ma'aden, and PhosAgro - processes tens of millions of tonnes of sulphur annually to produce phosphoric acid for MAP, DAP, and NPK. By volume, fertilisers need sulphur far more than metals do. By margin and by ability to pay, they lose the bidding war.

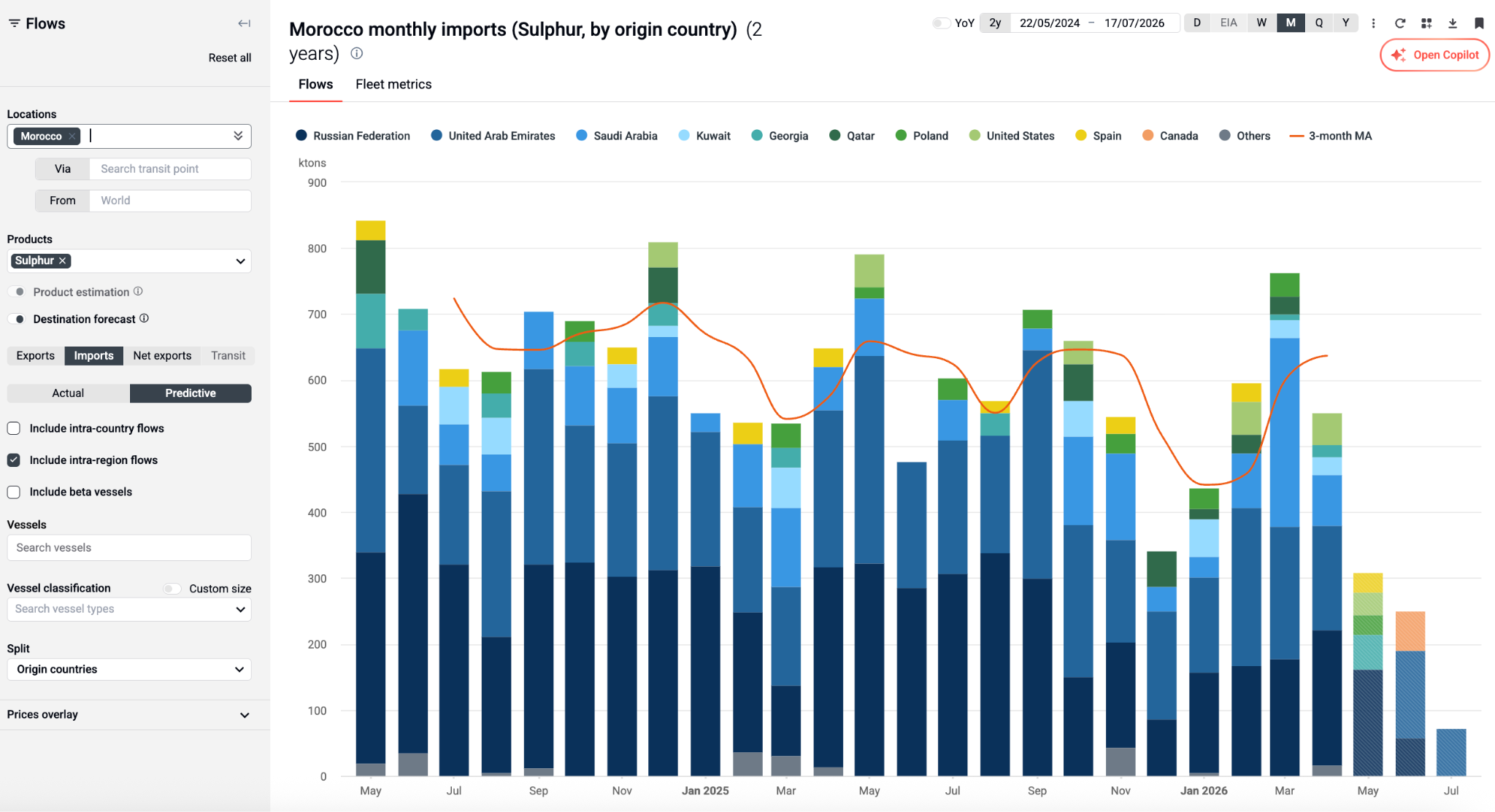

Morocco's OCP is the world's largest phosphate exporter. Jorf Lasfar is one of the world's largest consumers of sulphuric acid. The last MEG sulphur cargo to arrive at Jorf Lasfar discharged on 10 April 2026 - the vessel Kallone. Since that date, OCP has been sourcing from Russia and the US Gulf, at markedly higher cost.

(Do we have any data /intel on OCP that can be included here?)

The rational response, already underway, is production cuts. Mosaic has reduced domestic US phosphate output by approximately 2 million tonnes rather than absorb the feedstock cost at the margin. This creates a secondary perversity: Mosaic's domestic phosphate cuts free up US and Canadian sulphur supply that is now flowing to Africa, where copper producers bid it away from the fertiliser market entirely.

Nickel: caught in the middle and losing

HPAL nickel sits in an uncomfortable position between the two. Its sulphur cost share is the highest of any sector, more than 50% of MHP production cost at current prices. But its final product, MHP, is priced at a discount to primary Class 1 nickel, limiting the margin available to absorb feedstock spikes.

Unlike copper SX-EW - which can run a partial leach when acid is short, maintaining reduced output - HPAL plants have no such flexibility. The process requires a continuous, high-volume acid supply to maintain the slurry at operating temperature and pressure. A shortfall means shutdown. There is no middle ground.

"The big difference between copper and nickel here is that copper will be curtailed slowly — leaching takes 6 months and producers can run a partial leach — while HPAL operations are either on or off." Ben Ayre - Director of metals & minerals data, May 2026.

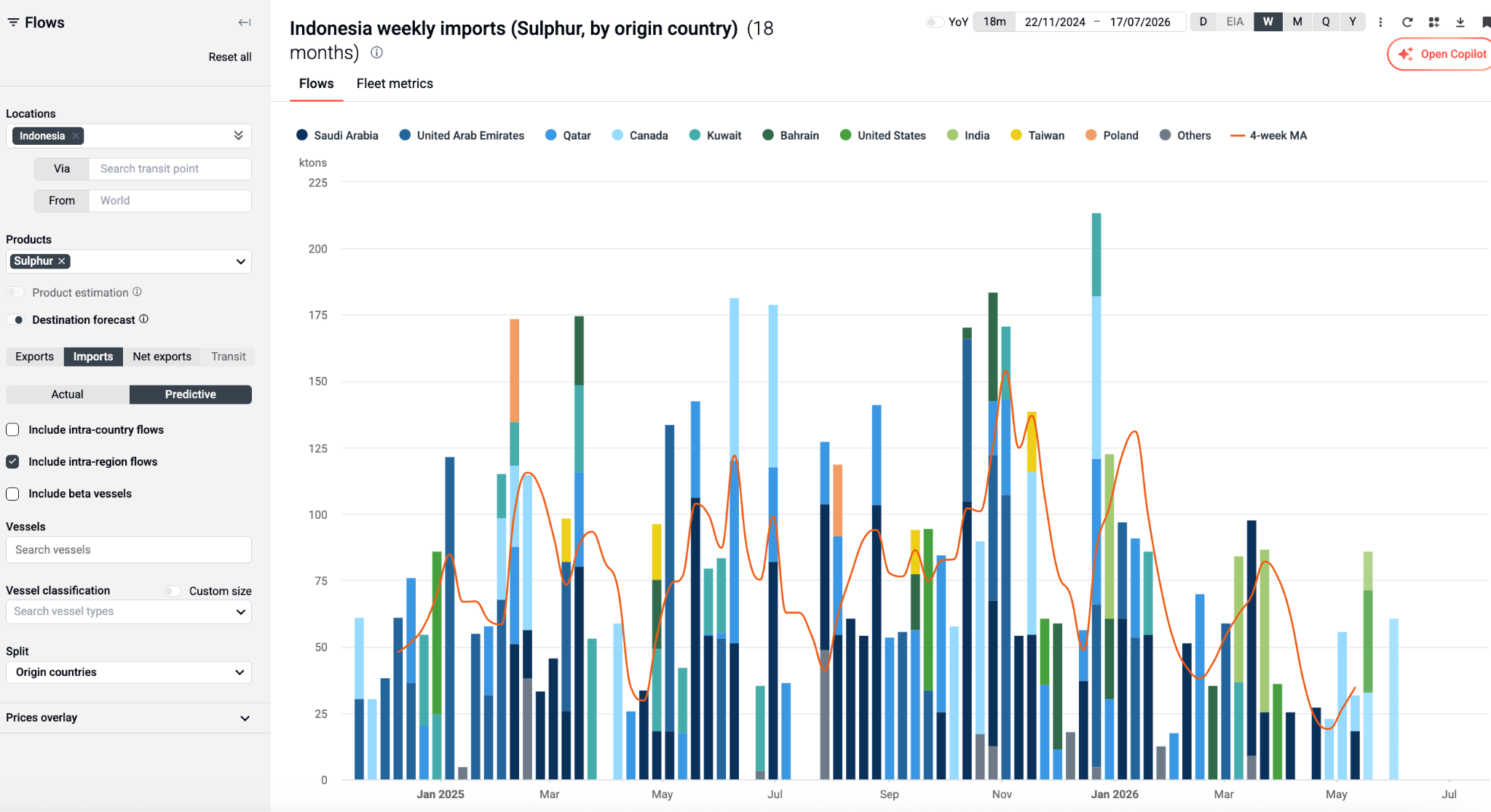

Huayou's decision to cut Indonesian HPAL output by approximately 50% is the logical outcome of this dynamic. The company could not out-bid DRC copper producers for spot sulphur. It could not source enough from India or Canada to maintain full production. The binary economics of HPAL made the cut inevitable, and Kpler's Indonesia import data showed the supply gap three weeks before Huayou's announcement.

Conclusion

In a tight sulphur market, the allocation dynamic resolves through margin. The flows show where it's happening.

Copper's product economics absorb elevated feedstock costs; fertiliser producers adjust output rather than absorb the margin compression; HPAL nickel, with the highest cost share and the least pricing power, curtails first. Whether a Strait reopening materially changes this depends on how much caged supply is already committed under long-term contracts. Kpler's import and transit data tracks that resolution in real time.

The Kpler view: curtailments are visible before the headlines

The practical value of Kpler's flow data in this market is that it surfaces the allocation problem before it appears in production statistics, earnings calls, or analyst consensus. Import flows into Indonesian HPAL installations started falling in mid-March. The public announcement of Huayou's cut came in late April. The import data led by three weeks.

The same logic applies to fertilisers. Morocco's last MEG sulphur cargo is a confirmed data point in Kpler, the Kallone, discharging at Jorf Lasfar on 10 April. OCP's shift to Russian and US supply is visible in the import origin split. Mosaic's production cut is visible in the reduction of US domestic sulphur consumption, freeing tonnes that then appear in Kpler's Africa export data.

These are not predictions. They are observed flows at the vessel level, continuous, ahead of the market consensus that forms when the sell-side publishes its next monthly report.

CTA: Explore the data in Kpler

See why the most successful traders and shipping experts use Kpler

Get real-time sulphur and sulphuric acid intelligence

.jpg)