[UPDATE] Running out of barrels: cumulative oil losses reach 961 Mbbls, a few days short of 1 billion barrels

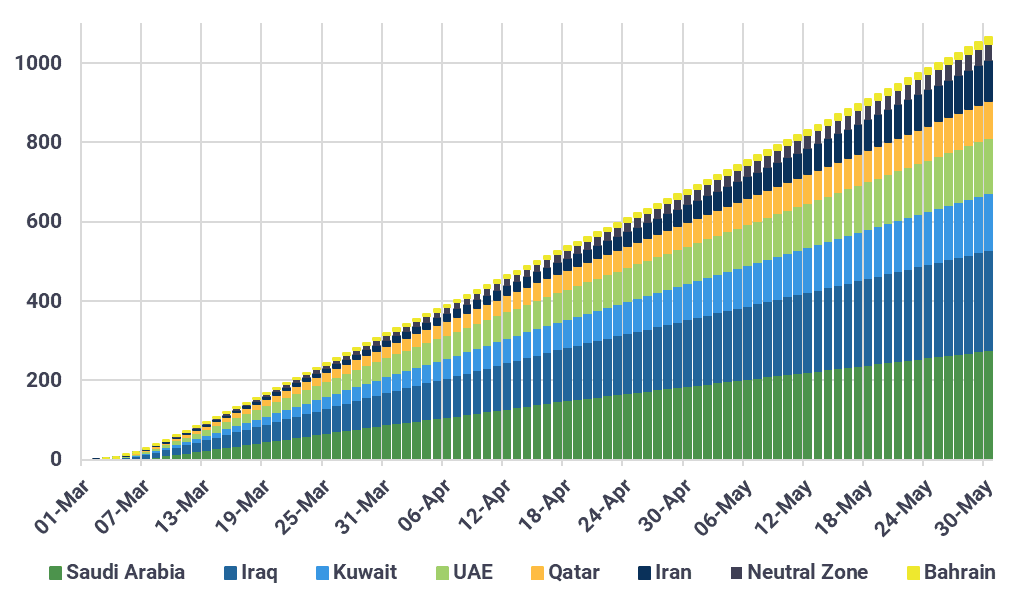

Cumulative crude and condensate supply losses in the Middle East have reached 961 Mbbls as of 22 May, with the psychologically important 1 billion mark to be breached early next week.

Cumulative Middle Eastern crude and condensate supply outages have continued to climb rapidly in recent weeks, jumping some 90 Mbbls in the past week, as the outright production shut-ins have inched higher as well. Another 100kbd is likely to have gone offline in the past week, made up of continued pressure in Iraq and Saudi Arabia, while Iranian supply (despite the blockade), was revised slightly higher due to the resilience in the country’s refinery run rates.

Seasonally-higher demand is coming, which could incrementally boost regional supply to meet demand, though the economic realities in the region may force some organic demand destruction as well, capping any summer-linked marginal increase in production levels.

In the face of the continue pressure of the blockade, Iran is attempting to manage the remaining onshore and ballast vessel options in terms of storage, with a maximum of 45 Mbbls combined that could be used, though it is likely that usable storage would be filled before the end of June.

Cumulative crude and condensate supply outages by country, Mbbls

Source: Kpler

While the pace of inventory builds is dictating the Middle Eastern production landscape, the wider market is acutely focussing on inventory draws in the rest of the world.

While China was holding out as an anomaly in terms of stock draws, recent data shows that the stark drop in monthly imports (6.73 Mbd in May), combined with a less severe drop in refinery run rates has meant that inventories have finally started trending lower, drawing around 19 Mbbls in the past month.

In contrast, the rest of the world (excluding the Middle East and China) has seen onshore stocks draw at an accelerating pace, signalling further tightness ahead. A pace of just over 1.5 Mbd was being seen two weeks ago (measuring from the start of the war). This has now jumped to closer to 1.7 Mbd.

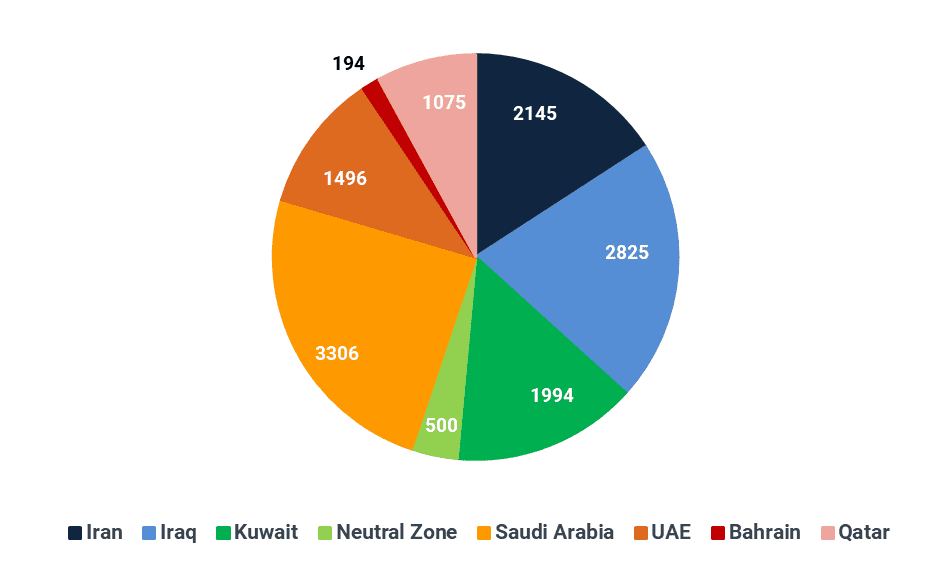

Middle Eastern crude and condensate supply outages by country, kbd

Source: Kpler

See why the most successful traders and shipping experts use Kpler

![[UPDATE] Running out of barrels: cumulative oil losses reach 961 Mbbls, a few days short of 1 billion barrels](https://cdn.prod.website-files.com/65059ad784ac02253c62356c/6a03a3355eae35e6a277fa8c_crude.jpeg)

See why the most successful traders and shipping experts use Kpler