Beyond Hormuz: The pipeline routes that could reshape Gulf oil flows

The crisis around the Strait of Hormuz has sharply accelerated both short-term rerouting and longer-term pipeline planning, creating renewed political momentum behind several bypass routes.

Key takeaways:

- The Saudi East–West Pipeline is running below capacity, with export infrastructure at Yanbu — not the pipeline itself — limiting throughput.

- The UAE's proposed Hamriyah–Fujairah pipeline is in early planning and could be operational within three years, offering a meaningful additional bypass corridor.

- IPSA rehabilitation faces a prohibitive combination of decades of disrepair and deep political complexity between Riyadh and Baghdad, making a near-term restart unlikely.

- The Basra–Aqaba pipeline would require an estimated $10 billion in new construction, several years to complete, and would traverse a security-sensitive corridor through Anbar province.

- The Kirkuk–Ceyhan pipeline's theoretical capacity of 1.6 Mbd is well beyond practical reach, constrained by severe physical degradation, chronic operational instability, and Iraq's south-heavy production base.

- The Kirkuk–Baniyas revival remains commercially and financially unviable in the near term, blocked by Syrian sanctions, fragmented territorial control along the route, and the near-impossibility of securing Western financing or insurance.

Previous regional pipeline plans were repeatedly suspended or shelved due not only to prohibitive costs and logistical complexity, but also to the geopolitical challenges inherent in cross-border infrastructure. Inter-country pipelines, in particular, have historically proven difficult to advance, requiring sustained political alignment, security guarantees, and long-term cooperation between often competing states.

The current disruption, however, has fundamentally shifted that calculus. A new set of geopolitical incentives — driven by the war and the urgent need to mitigate reliance on the Strait of Hormuz — is reviving momentum behind projects that had long stalled. Looking ahead, several pipeline options could be expanded, reactivated, or newly built to reduce dependence on the Strait. All such projects, however, would require substantial capital investment and would likely take several years to come online.

Two bypass routes are already operating at high utilisation — Saudi Arabia's East–West (Yanbu) Pipeline and the UAE's ADCOP pipeline — allowing both countries to route exports around the Strait. The most immediately actionable steps would therefore centre on expanding capacity within these existing corridors: debottlenecking and enhancing the East–West Pipeline, and building additional parallel capacity alongside ADCOP to Fujairah. Crucially, these options avoid the political and logistical complexity of new cross-border infrastructure.

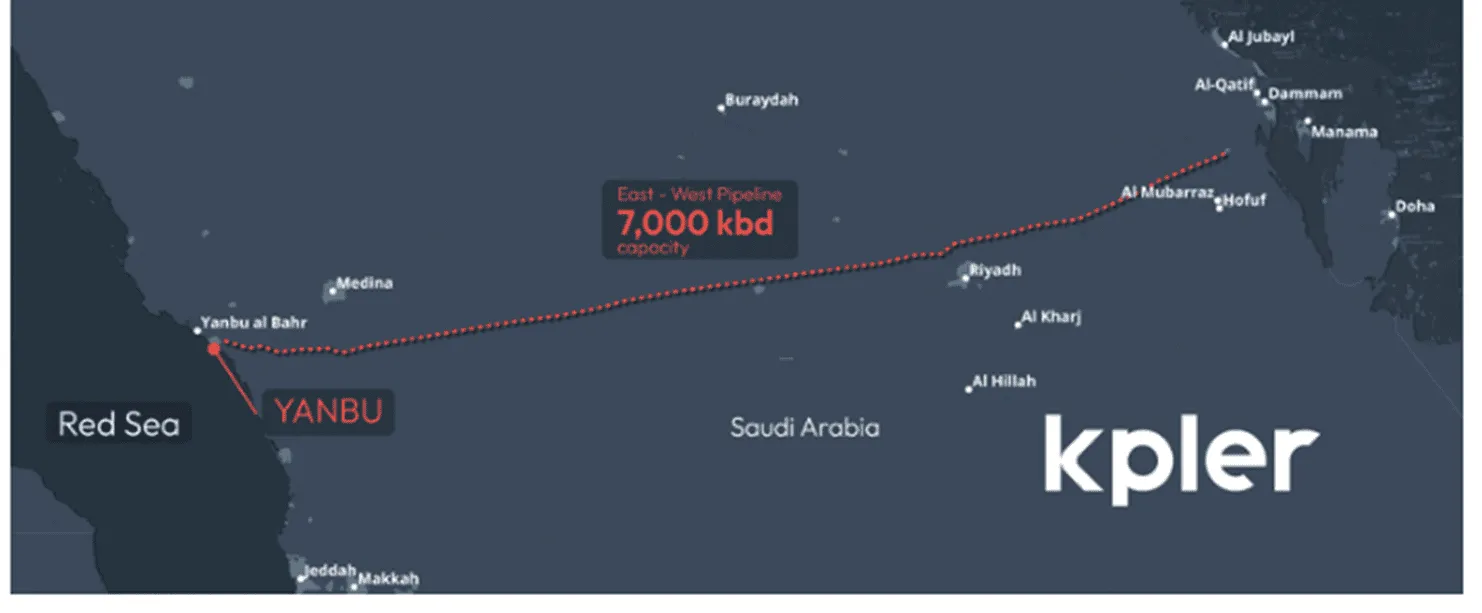

Maximising capacity of the Saudi East–West Pipeline

The East–West Pipeline is technically capable of moving up to 7 Mbd from Abqaiq to Yanbu on the Red Sea. Considreing future expansions, the binding constraint lies not within the pipeline itself but at the export terminals downstream. Sustainable export capacity at Yanbu is estimated at around 4.5–5 Mbd — approximately 1.5 Mbd from Yanbu North Crude Terminal and around 3.0 Mbd from Muajjiz — with limited scope to push beyond that ceiling under current infrastructure. Since the Strait's closure, West Coast exports have risen to 4.77 Mbd in April, suggesting Yanbu is already operating at or near its effective limit.

Any meaningful expansion of throughput would therefore require debottlenecking the loading infrastructure at Yanbu before the pipeline capacity could be expanded/parallel pipeline added. Bridging this pipeline–port mismatch — and designing Yanbu for sustained exports beyond 5 Mbd — would entail billions in capital expenditure. To date, no major crude-loading expansion at Yanbu has been publicly announced. Beyond infrastructure constraints, the route also carries geopolitical risk, given Iran-linked Houthi activity in the Red Sea and at the Bab el-Mandeb chokepoint.

Saudi East-West pipeline

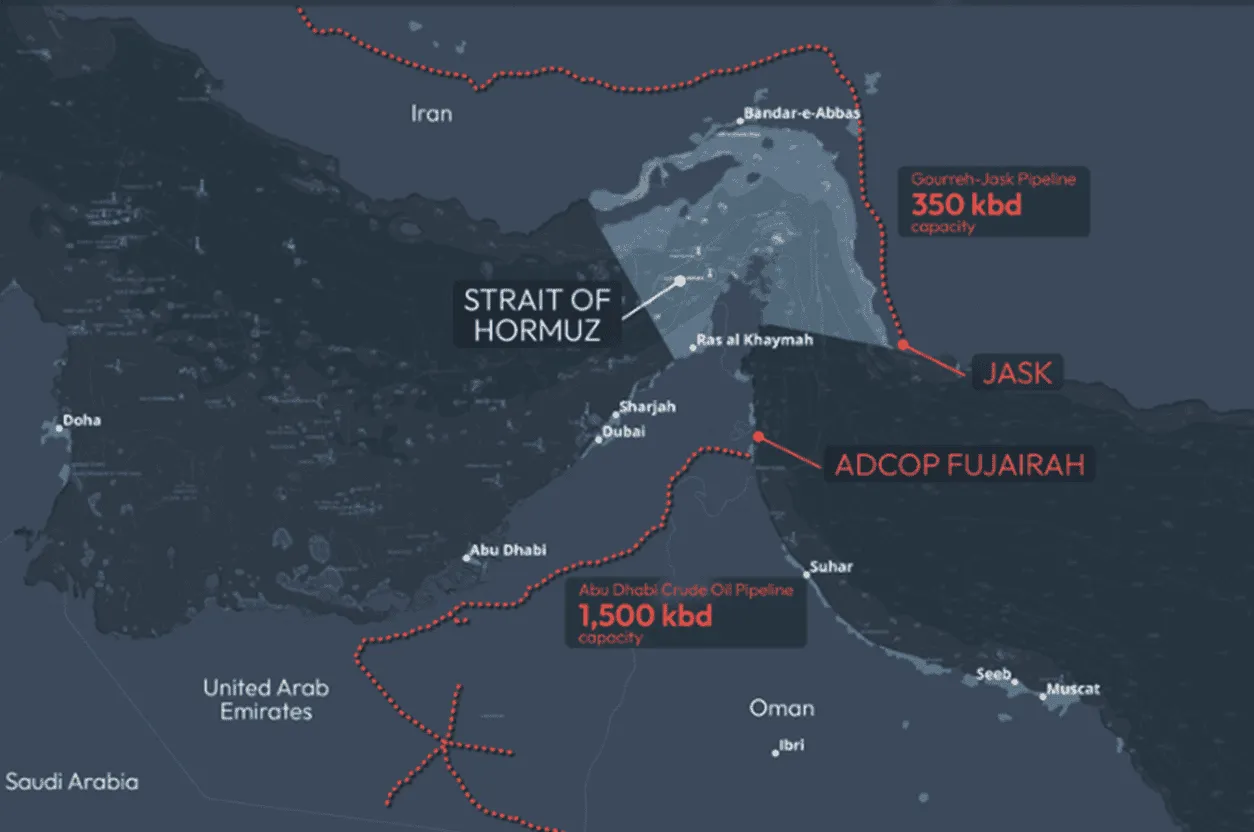

Expanding the UAE's ADCOP Pipeline

The UAE's principal bypass route is the Abu Dhabi Crude Oil Pipeline (ADCOP), which runs from inland production at Habshan directly to the Fujairah export terminal on the Gulf of Oman, bypassing the Strait entirely. With a nameplate capacity of around 1.5 Mbd, ADCOP has become critical to sustaining UAE export flows since the disruption began. The shift in export patterns has been stark: ADCOP accounted for roughly 30% of UAE crude loadings in 2025, a share that surged to 80% in April as Gulf transit routes were curtailed. Loadings from the terminal reached 1.82 Mbd that month, indicating the system is operating at or beyond its effective capacity.

Plans to expand this corridor were already in motion prior to the current crisis. ADNOC had been evaluating a second parallel line — a $3 billion, 300-kilometre pipeline designed to carry an additional 1.5 Mbd from Jebel Dhanna in Abu Dhabi to Fujairah. Unlike the existing ADCOP route, this line would allow offshore and western Abu Dhabi crude streams to reach Fujairah without transiting the Gulf, effectively doubling the UAE's Strait bypass capacity from approximately 1.5–1.8 Mbd to over 3 Mbd.

In addition, early-stage plans have emerged for a further pipeline to Fujairah originating at Hamriyah Port in the emirate of Sharjah. Under this concept, crude would be loaded from vessels at Hamriyah and transported overland to Fujairah, adding another bypass corridor without reliance on Gulf waters. The project is not yet in formal planning, with construction estimated to take around three years and capacity of around 1.5 Mbd.

UAE ADCOP pipeline

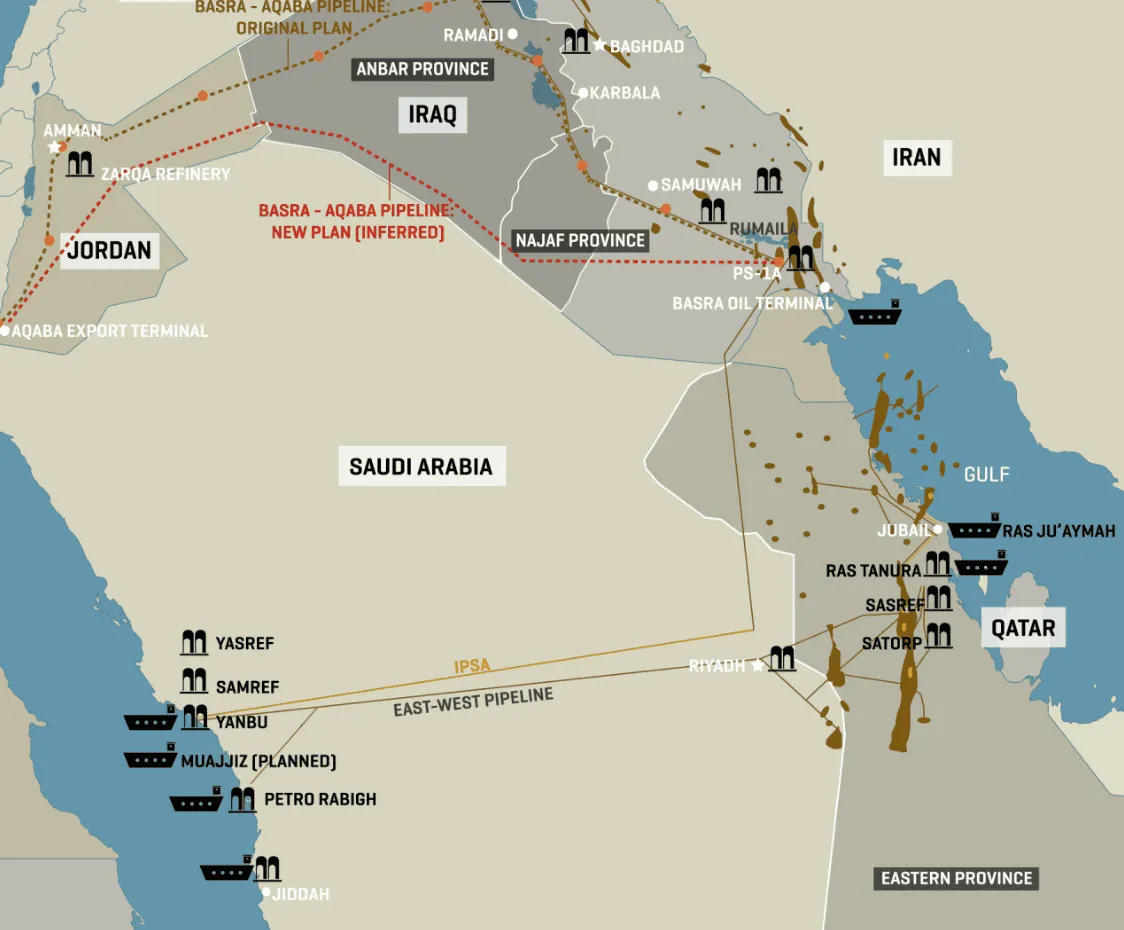

Revival of the IPSA pipeline

A further option, though considerably more complex, is the currently dormant Iraqi Pipeline in Saudi Arabia (IPSA), which runs from Al-Zubair in southern Iraq through Saudi territory to Yanbu on the Red Sea, with a nameplate capacity of approximately 1.65 Mbd. IPSA was originally constructed in the 1980s during the Iran–Iraq War to allow Iraqi crude exports to bypass the Gulf via Saudi territory — it was never designed as a Saudi export pipeline. The line fell out of operation in 1990 following Iraq's invasion of Kuwait, after which Saudi Arabia assumed control as part of reparations settlements under UN compensation frameworks linked to the Gulf War. Since then, portions of the system have been repurposed and integrated into Saudi Arabia's domestic gas network under UN Resolution 687, while the remainder has sat idle for over three decades — with no sustained maintenance in the intervening years.

There have been periodic discussions about reopening IPSA for Iraqi exports or repurposing it for Saudi crude use, but no confirmed or near-term project has emerged. The barriers are substantial on both technical and political fronts. On the technical side, decades of inactivity and partial repurposing mean that any restart would require extensive rehabilitation before the pipeline could safely handle crude volumes again. On the political side, reactivation would demand strategic alignment between Riyadh and Baghdad, formalised through a bilateral agreement — a significant diplomatic undertaking given the current regional environment. Saudi Arabia's incentives to pursue this are limited, not least because of Iraq's deep political, economic, and energy ties to Iran. Iran-aligned militias operating out of Iraqi territory played a direct role in attacks on Saudi and Kuwaiti targets during the recent conflict, adding a further layer of strategic risk for Riyadh.

While IPSA's reactivation could in principle provide a meaningful additional export corridor that entirely bypasses the Strait, the combination of rehabilitation requirements, political complexity, and misaligned incentives makes a near-term restart unlikely. We assess the probability as low for the foreseeable future.

Various planned pipelines across the Middle East

Source: MEES

Construction of Basra–Aqaba pipeline

Another frequently cited option is the Basra–Aqaba pipeline, which would involve constructing over 1,600 kilometres of entirely new pipeline to carry crude from Basrah in southern Iraq across the country to the port of Aqaba on Jordan's Red Sea coast. With a planned capacity of around 1 Mbd, this greenfield megaproject would require an estimated $10 billion in capital investment.

From a political standpoint, Basra–Aqaba is more feasible than IPSA. Iraq–Jordan relations are broadly positive and Amman has been supportive of the project. The principal risks, however, centre on Iraq's internal stability and the financing challenge of mobilising capital at this scale. The pipeline's proposed route through Anbar province in western Iraq raises particular concern: the region has a history of instability, and the risk of pipeline sabotage cannot be discounted.

Re-start of the Kirkuk–Baniyas pipeline

Also under discussion is the revival of the Kirkuk–Baniyas pipeline, linking Kirkuk in northern Iraq to the Syrian Mediterranean port of Baniyas. Originally constructed in the early 1950s, the pipeline had a capacity of roughly 300 kbd before operations ceased entirely in 2003 amid the Iraq War and subsequent regional instability. Under current proposals, a rehabilitated or entirely new system could carry up to 1.5 Mbd — well above the original line's capacity. In 2025, Iraq and Syria agreed to appoint an international consultant to assess the project's feasibility. Cost estimates vary widely, ranging from approximately $5 billion to as much as $10 billion depending on scope, and timelines remain uncertain. The project has reportedly received some degree of U.S. support and, if realised, could help establish Syria as a Mediterranean transit corridor for Iraqi crude.

Despite this, we assess the probability of near-term realisation as low. While technically feasible, the project is commercially less attractive than either the Basra–Aqaba pipeline or the Kirkuk–Ceyhan route (discussed below). The pipeline would traverse eastern Syria, a region characterised by fragmented control and persistent security risk. Compounding this, Syria remains subject to broad U.S. and EU sanctions, which would exclude Western firms from participation and make even non-Western investors cautious. Securing financing and insurance for a project of this nature — routing through sanctioned territory — would present a barrier in its own right.

Increasing throughput at Kirkuk–Ceyhan pipeline

Finally, increasing throughput via the Kirkuk–Ceyhan pipeline could enable larger volumes of Iraqi crude to bypass the Gulf entirely. The pipeline was shut down between early 2023 and late 2025 following a dispute over unauthorised exports — Turkey had permitted Kurdish crude shipments without Baghdad's approval. A landmark agreement between Baghdad, the Kurdistan Regional Government (KRG), and international oil companies ultimately ended the shutdown, with the KRG committing to deliver a minimum of 230 kbd through the line. For context, Kurdish exports via Ceyhan were trending above 400 kbd prior to the 2023 closure.

The pipeline's return to service has, however, been far from smooth. In mid-March, flows temporarily collapsed to just 9 kbd — a dramatic fall from the 230 kbd recorded only days earlier — reflecting the line's persistent vulnerability to disruption. Kpler data shows exports recovered to an average of 140 kbd in April, with flows trending above 200 kbd in May so far. This operational volatility is not atypical: the pipeline has suffered multiple shutdowns and interruptions in recent years due to security incidents, political friction between Baghdad and the KRG, and recurring technical failures.

Iraq is targeting a recovery toward 400–500 kbd — broadly in line with throughput levels achieved between 2016 and 2022 — against a theoretical maximum capacity of around 1.6 Mbd. In practice, the effective ceiling sits well below that figure, owing to severe physical degradation accumulated over years of underinvestment and intermittent operation. Supply-side constraints add a further structural limitation: more than 90% of Iraqi production is concentrated in the south, meaning that feeding significantly higher volumes into a northern pipeline would require either major field development or substantial internal redistribution infrastructure. Reaching anywhere near 1.6 Mbd is technically conceivable but politically and commercially unlikely in the near term.

Against this backdrop, Turkey put forward a more ambitious proposal in March 2026: extending the Kirkuk–Ceyhan pipeline southward to Basra, which would create a full Mediterranean export corridor and materially reduce Iraqi dependence on the Strait of Hormuz. The proposal remains at an early stage, but if pursued, it would represent a transformative pipeline development in the region.

See why the most successful traders and shipping experts use Kpler