Dry bulks: Top 5 market drivers in 2026

This article was first posted on Kpler Insight on 7 January.

Dry commodity markets are set for another bumpy year in 2026. Much of the attention will again be on China, where a structural slowdown and increased barriers to exports are threatening the steel sector. In the grains and oilseeds markets, unprecedented wheat stocks are set to pressure prices, while US farmers will face tough planting decisions. Discussion of the Simandou ramp-up is set to continue to dominate conversations around iron ore. Meanwhile, we expect aluminium and alumina prices to continue to diverge.

Can Chinese steel exports continue?

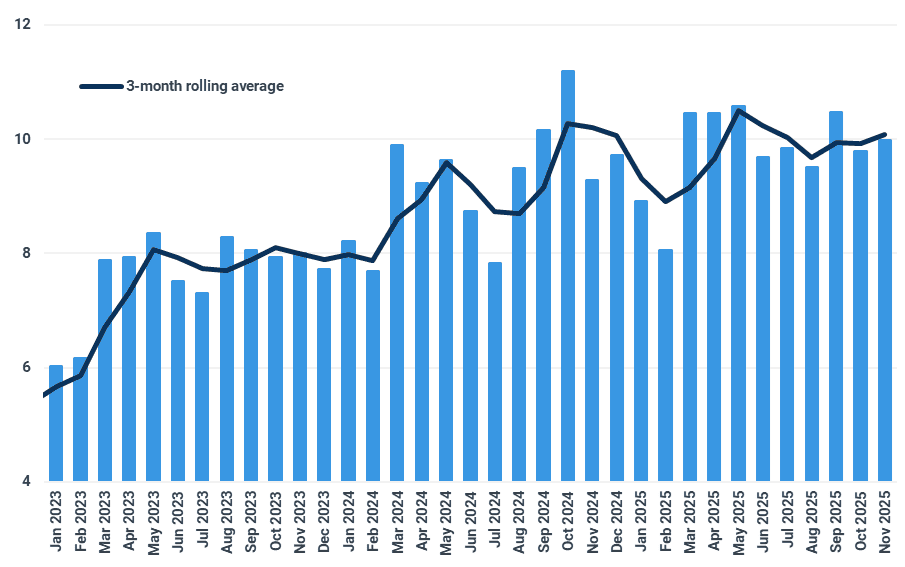

Chinese steel exports defied gravity in 2025, shaking off lower domestic steel production, tariff barriers, and import quotas in receiving markets to push higher. We expect trade to remain robust this year, but dip slightly compared to a very strong 2025.

The country’s steel product exports grew in each of the first eleven months of 2026, with January-November shipments up by 6% y/y at 107.72 Mt. This is impressive, given that 2024 was a multi-year high and crude steel production fell by 4% over the same period.

With trade barriers targeting specific products, Chinese mills have sustained volumes by trading down to lower-value products such as billets. This prompted a call from the China Iron and Steel Association for a clampdown on low-cost steel shipments.

In December, China’s Ministry of Commerce announced a steel export licensing regime. This may slow the pace of shipments however, we believe the focus is more on combating VAT evasion and illegal exports than lowering total trade. With permit issuance the proviso of local governments, who have a strong incentive to support jobs at mills and in the steel supply chain, we expect the impact on trade to be small.

Chinese steel product exports: strength to persist through 2026? (Mt)

Source: China Customs

Unprecedented wheat stocks will pressure prices, especially in Europe

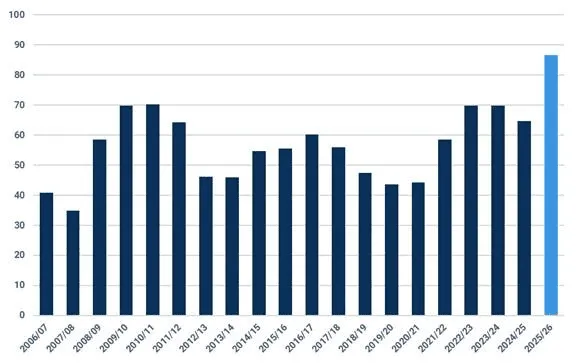

Wheat production is more diversified than other grains, and supply has generally been kept in check over the last decade by weather issues affecting a major producer.

2025 was different. Favourable weather led to all majors producing at trend and above. The resulting deluge of wheat will take 2026 stocks to unprecedented levels.

Wheat ending stocks at top 7 exporters will rise to unprecedented levels (Mt)

Source: Kpler Insight

Despite a delayed harvest, Black Sea exporters have been shipping aggressively through the first half of the wheat year (Jul-Dec). The EU has struggled to compete, with exports at 2024 levels when it had produced the smallest crop in 20 years. When looked at separately, Romania and Bulgaria are competing in the market, while Western Europe is faring worse.

Traditionally, Western European exporters would wait out the Black Sea harvest pressure to export in the second half of the year (Jan-Jun). However, Argentina’s expected record wheat crop and Australia’s near record harvest are reshaping market expectations at a time when Northern Hemisphere supplies are already plentiful.

On the other hand, import demand has not seen a similar increase and remains below its post-COVID highs, mainly due to reduced Chinese imports.

Initial estimates already suggest reduced acreage in 2026 in the EU. Barring weather events, the year is going to be challenging for cereal farmers, especially marginal and higher cost producers. For traders, futures markets should offer carry throughout most of the year.

US farmers will have tough planting decisions in 2026

Global production of corn and soybeans saw a significant ramp-up over the last decade as Brazil increased output. While there was a commensurate increase in demand in the 2010s, supply growth has outpaced demand in the past five years. Barring weather-related supply shocks, global corn and soybean balances will remain in oversupply.

High corn acreage and yields produced a record crop in 2025, leading to stocks of over 60 Mt, +20 Mt y/y, despite massive export demand. A similar crop in 2026 will push Aug-27 stocks to unprecedented levels.

With intense competition from Brazil in the soybean market, the US will struggle to find buyers. Without captive demand through deals, the US is likely to store, rather than export, beans.

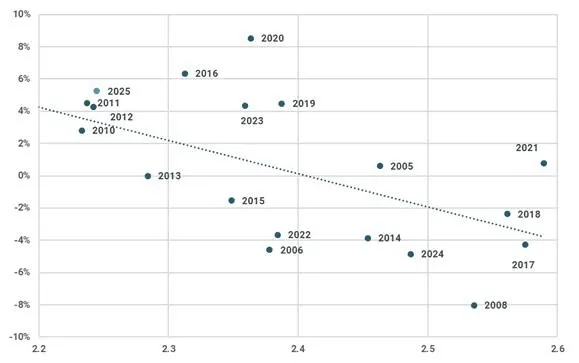

Global S&Ds have made both corn and soybean poor options to plant. The ratio of Nov soybean and Dec corn futures, which is a good indicator for relative acres, saw strength due to Chinese deal talks. A lack of follow-up will see it recede. Models suggest unchanged acres at an average SX/CZ ratio of 2.34 from Feb to mid-March. In the absence of certainty from China, and if fundamentals prevail, we expect corn acres to be close to last year’s highs.

Corn acreage change (%) vs Dec soybean/ Nov corn ratio

Source: Kpler Insight, USDA

Simandou ramp-up: How much iron ore? How soon?

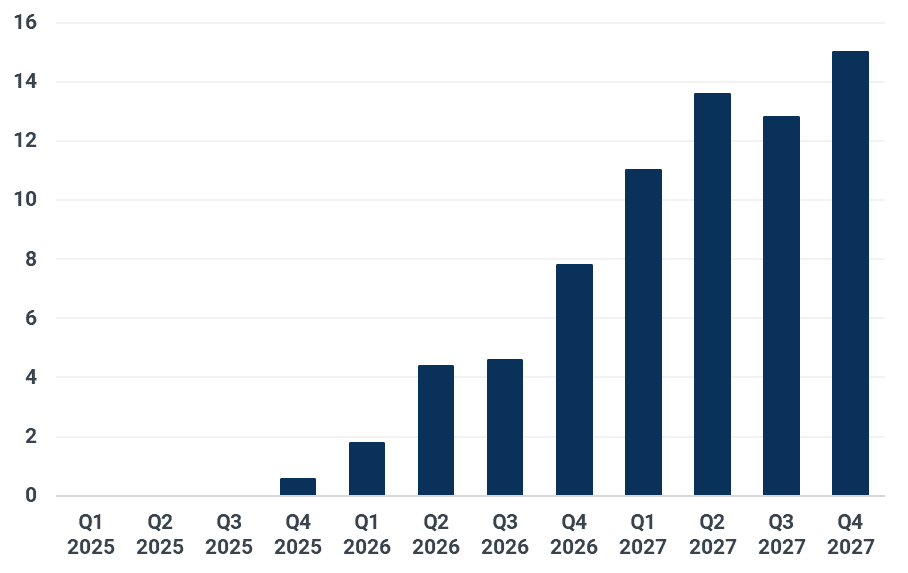

The iron ore market is bracing for a surge in high-grade seaborne supply in 2026 as the Simandou project in Guinea ramps up towards its 120Mtpa nameplate capacity. The pace of this ramp-up is key to the market outlook.

The Simandou project was inaugurated on 11 November 2025. Loading of the Winning Youth with the first export cargo began around the same time. Exports in 2026 are projected at just over 18Mt, but significant volumes of ore are not expected to hit the market until after the rainy season ends in October.

China will be the destination for most of Simandou’s iron ore however, the country’s steel sector is in structural decline, with crude steel output to contract again in 2026. With iron ore demand stagnating, material from Simandou will displace domestic ore and put pressure on prices.

Iron ore prices have finished 2025 firmly. The pace at which Simandou iron ore arrives on the market, and the ability of Chinese steel mills to absorb fresh seaborne supply, will be key to the outlook for 2026. Lower iron ore prices will reduce profits for miners, but improve margins for struggling steel mills.

Simandou iron ore export ramp-up (Mt)

Source: Kpler Insight

Divergence between aluminium and alumina prices will continue

Underpinned by tightening supply fundamentals, aluminium prices are expected to remain elevated throughout 2026. In China, the production of primary aluminium is nearing the government-imposed cap of 45 Mtpa, leaving limited room for further growth. Elsewhere, power availability is emerging as a critical bottleneck. The Mozal smelter in Mozambique faces an uncertain future beyond March 2026 due to stalled electricity contract negotiations, while expansion in Indonesia faces looming power supply limitations.

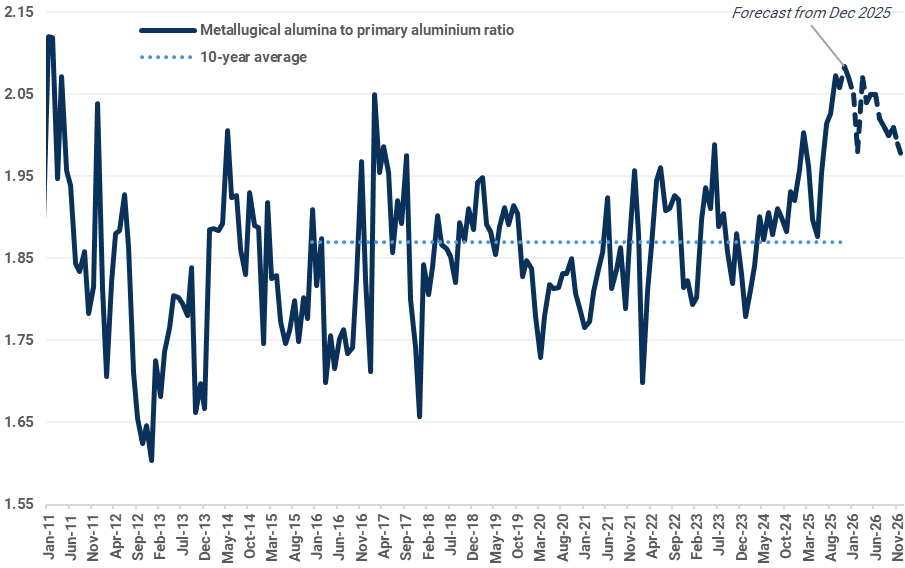

In stark contrast, prices of alumina, the key raw material for primary aluminium, are likely to remain depressed in 2026, weighed down by persistent oversupply. China, representing over 60% of global alumina output, saw its metallurgical alumina-to-primary aluminium output ratio surging to a 14-year high of 2.08 in November 2025, significantly above the long-term average of 1.87. Despite these signs of saturation, additional alumina capacity is scheduled to come online in 2026 across China, India, and Indonesia, far outpacing production curtailments in regions such as Australia.

China’s metallurgical alumina-to-primary aluminium output ratio may stay over 2 in most of 2026

Source: IAI, Kpler Insight

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you to track critical crude oil market developments for your own analysis. Our precise forecasting empowers smarter trading and risk management decisions.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler