Fed moves from cutting to caution

The January FOMC underscores a narrower runway for rate cuts amid an improving economic outlook.

Summary

- Policy Hold: The Fed held rates steady at 3.5 – 3.75% in January, reinforcing a hawkish pivot that began last October as Powell emphasized resilient growth and still-elevated inflation. Despite two dissents favoring a cut, the Committee signaled reduced urgency to support the labor market.

- Macro Backdrop: Stronger growth and sticky inflation underpin the Fed’s cautious stance, with US GDP now expected to grow 2.4% this year and core PCE inflation running at a 2.6% six-month pace. Labor market weakness reflects slower labor supply growth rather than deteriorating demand.

- Forward Path: We expect the Fed to remain on hold through the end of Powell’s chairmanship in May, with the post-May cutting path dependent on Board composition and leadership. While we believe a Trump-appointed chair will ultimately manage 50bp of easing this year, markets are increasingly pricing in a shallower and more uncertain cutting cycle.

Market Analysis

As expected, the US Federal Reserve kept the official policy rate steady in a target range of 3.5 – 3.75% at the January 28th FOMC meeting. The move was largely anticipated by the market with CME Fed Funds futures pricing a pause with near full certainty. The official policy statement indicated that the unemployment rate had “shown some signs of stabilization,” while inflation remains “somewhat elevated.” Powell mimicked this sentiment arguing that both the upside risk to inflation, and the downside risk to the labor market have both lessened somewhat. Powell was notably more upbeat on the outlook for the US economy.

In our view, the January meeting completes a hawkish pivot that began last October, when Powell indicated that a December rate cut was not a foregone conclusion. While the Fed ended up cutting in December, sentiment was clearly shifting away from an outright bias to support the labor market, a pattern that continued into the January meeting. While two voting members, Miran and Waller, both dissented in favor of a 25bp rate cut, the other 10 members voted to keep the policy rate steady.

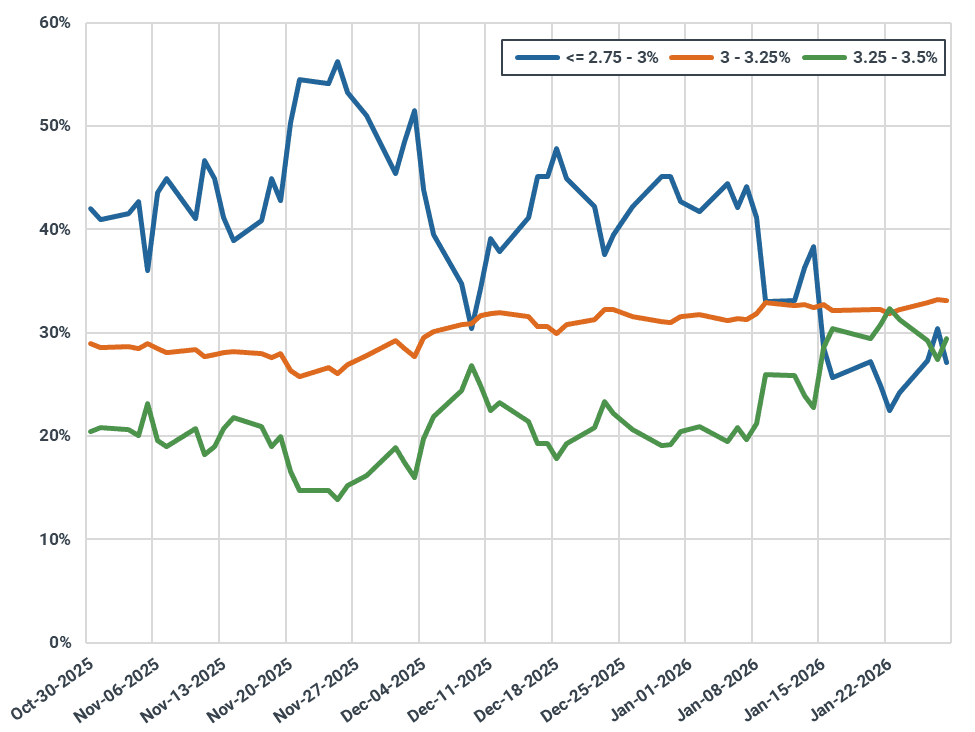

Fed Funds Rate Expectations by Year End (Current Policy Rate 3.5 - 3.75%)

Source: CME

We generally agree with the stance the Fed is taking on the economy. Growth expectations have clearly risen – we see US GDP expanding 2.4% this year, up from 2% last year. Inflation remains an issue. Core PCE-based inflation, which removes volatile food and energy, finished January at a six month annualized pace of 2.6%. The labor market looks weak from a job creation standpoint, but much of this is due to far lower labor supply growth. In January, the unemployment rate fell back to 4.4%, down from a cycle peak of 4.5% seen a month earlier.

Our view on the forward outlook for the Fed Funds rate is two-tiered. Given the current US dynamics that include growth acceleration, and ongoing above-target inflation, we believe the Fed will remain on pause until the Powell chairmanship finishes in May.

The path for the Fed cutting cycle after Powell exits the chairmanship looks unclear. Powell can technically remain on the Board of Governors for two additional years, though he might leave. In the press conference today, Powell gave no indication of his decision. If Powell stays on the Board, the Trump administration’s ability to bring in an additional outside ally depends on Board vacancies; the most immediate lever is Miran’s seat, whose term technically ends on January 31st. This would limit Trump’s influence over the FOMC’s voting arithmetic, although the chairman can still exert meaningful influence over Committee consensus and messaging.

There are also questions about Lisa Cook, another governor facing legal scrutiny from the White House. Her departure would represent another pathway for appointing an outsider. However, recent legal developments suggest Cook is likely to remain in her role while the case is adjudicated.

Betting markets have recently elevated Rick Rieder as most likely to receive the nod from the White House as the next chair. Rieder, who currently serves as CIO of Global Fixed Income at BlackRock, would likely argue for a more aggressive cutting cycle, and would look for other ways to provide liquidity to certain sectors of the economy. Our view is that Rieder, or whomever Trump appoints, will find a way to get a limited number of cuts, say ~50bp, through the Committee by year-end. We will back off our existing expectation for a cut range of 50 – 75bp, as the upper end looks like a stretch right now.

Markets have also grown more sanguine on the outlook for rate cuts. Since early January, 2y yields, a good barometer for monetary policy, have pushed to 3.6%, up from 3.45% as the market backs off expectations for aggressive monetary policy easing. According to CME Fed Funds futures, there is a 74% probability of two or less 25bp cuts through the duration of this year, and a 41% probability of one or less 25bp cuts. USD, which has been in freefall following Trump comments on January 27th, firmed somewhat on the Powell press conference.

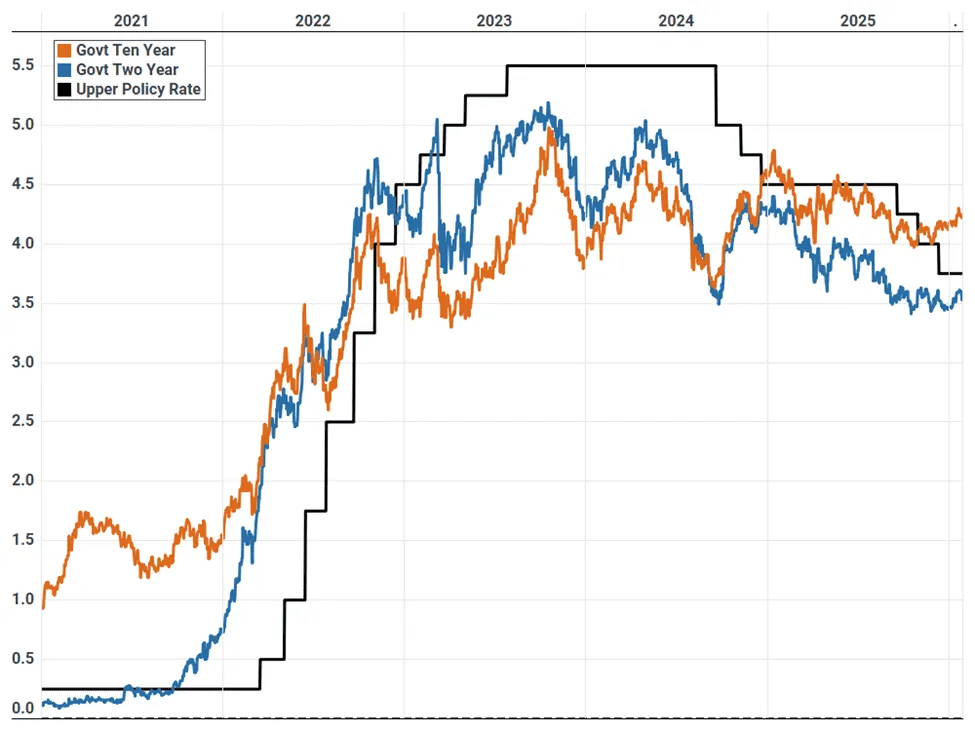

Daily US 2y, 10y Government Bond Yields and Upper Policy Rate (%)

Source: US Fed

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you to track critical crude oil market developments for your own analysis. Our precise forecasting empowers smarter trading and risk management decisions.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler