Russian gasoil resurgence floods Brazil but offers little respite for Med

Russian exports of diesel have surged as unplanned refinery outages have dropped and the current attacks are localized to the Black Sea. This will keep the sanctioned market well-supplied with Brazilian imports for January at multi-year highs and blunt some of the impact of USGC maintenance, but the Mediterranean will likely retain its current strength.

Market & Trading Calls

- Swelling sanctioned market allows Brazilian buyers ample choice but seasonal demand downswing sets up a race to the bottom for suppliers.

- Russian outflows of ULSD to counteract the drop in USGC supply in January and February, widening split between sanctioned and non-sanctioned sources.

- The recovery is uneven and a drop in Black Sea exports adds to structural Mediterranean strength.

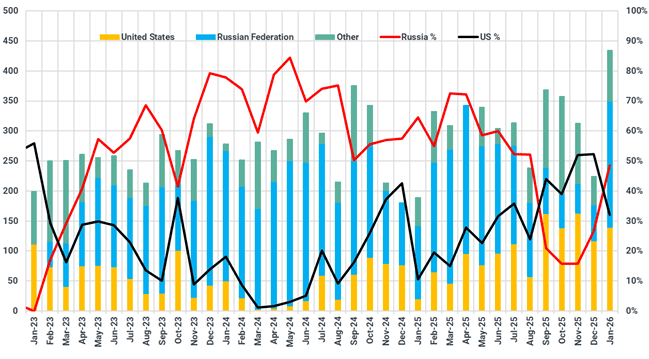

While much of the West of Suez diesel focus has been around the recent winter storms in the US or the impact of the EU’s Article 3ma, Russian gasoil exports have been resurgent over the last months as no planned seasonal maintenance and reduced impact from still ongoing Ukrainian attacks have allowed for a tentative recovery. The implications of this this are bearish for the wider Atlantic Basin as Brazil, the principal off-taker of Russian diesel after Turkey, is now on track to import the most since September 2022, at the expense of product sourced from the USGC.

Brazil gasoil/diesel imports (kbd) and country % share

Source: Kpler

This marks a tentative reversal of a key factor behind the shorter market in the Atlantic Basin experienced for much of Q4. The outages at Russian refineries, both planned and unplanned, supported the US Gulf Coast and cracks on both side of the Atlantic, as Brazil had to look for alternatives to meet its peak demand.

However, in contrast to then, Brazilian demand is currently on the downswing, although February will see m/m improvements. Brazilian demand should not be underestimated, rising over 3% y/y in 2025, but there is only so much to go into stocks. This increased Russian product will ultimately pressure prices once some of the weather driven pull on diesel in the Atlantic Coast wears off, as Brazilian importers are now spoilt for choice in terms of suppliers, lessening the price impact of the USGC refinery maintenance peaking in February.

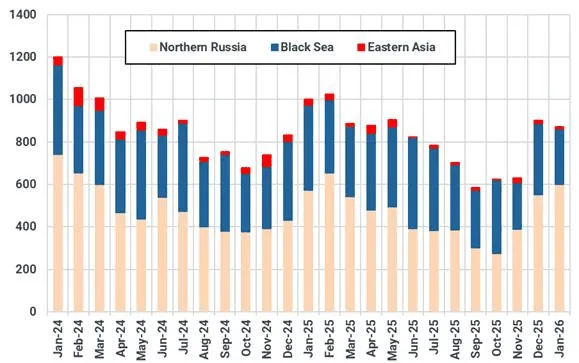

A crucial factor is the Russian export recovery is where the attacks by Ukraine are currently taking place. No recent attacks on key ULSD-exporting refineries like Kirishii (hit three times in 2025, the last of which was in early October) or the port of Primorsk (most recently in September) means the longer haul destinations, such as Brazil, are currently not affected. Exports from Primorsk are the highest since February 2025.

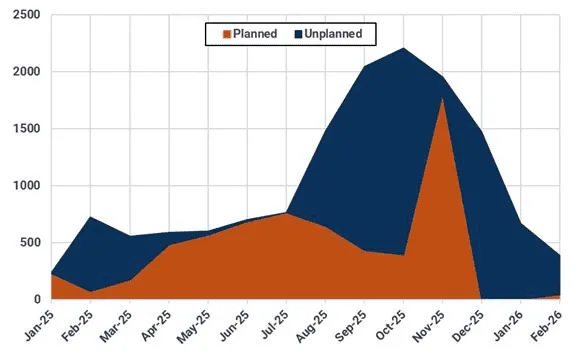

Russia CDU outages (kbd)

Source: IIR * does not include potential damage to Slavyansk refinery

While Russian CDU offline capacity is estimated at above 600 kbd for January (IIR) this is exclusively at refineries close to and that typically export via the Black Sea. The Tuapse refinery is out of action until the end of the February at least, a persistent target given its proximity Ukraine, the 177kbd Syzran refinery along the Volga was hit in December and a week ago the far smaller Slavyansk refinery close to the Black Sea coast was attacked, with damage as yet unknown. The port of Novorossiysk has been attacked frequently, and a step up in attacks on sanctioned vessels, and inadvertently on non-sanctioned vessels has lifted freight rates in the Mediterranean. These factors are combining to render Black Sea exports 35% lower y/y in January.

Russian gasoil/diesel exports by region (kbd)

Source: Kpler

The focus on attacks around the Black Sea is helping to keep the Mediterranean pricing at premium to Northwest Europe by heaping pressure on a market already contending with a decrease in supply due to the EU’s Article 3ma ban effectively cutting Turkish exports of ULSD to the West Mediterranean. This shortage adds to the structural limitations of both ULSD availability - Black Sea ports export a wide variety of sulphur grades – and the typical smaller cargo sizes. All of which leads us to expect little respite for the Mediterranean market despite the recovery in overall Russian gasoil exports.

The only real counterweight is the Middle East Gulf, but it is fragile. Rising ULSD and 10 ppm flows from the Middle East Gulf, increasingly routed via Suez rather than around the Cape, are one of the few mechanisms capable of easing Mediterranean tightness by lowering freight and shortening transit times. However, escalating Iran tensions place that release valve at risk. Any disruption to cargoes loading out of the Strait of Hormuz would remove the only scalable alternative to Black Sea supply. As long as that risk persists, Med pricing will continue to trade with a geopolitical scarcity premium rather than converge back toward Northwest Europe.

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you to track critical crude oil market developments for your own analysis. Our precise forecasting empowers smarter trading and risk management decisions.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler