Hormuz reignites lifting US yields

A month of stabilizing energy markets reverse as the US-Iran ceasefire collapses, reigniting concerns about energy inflation

Summary

- Ceasefire Collapses: At the July 8 NATO Summit, Trump declared the June 17 MoU effectively dead following a night of intense US bombing along the Strait of Hormuz, Iranian strikes on Bahrain and Kuwait, and reinstated US sanctions on Iranian crude. This reverses a month of stabilizing markets, during which Brent had fallen roughly $25/bbl to $71/bbl as of June 6 on strong Strait transits and weak Chinese demand.

- Oil Prices Surge: Brent jumped more than 8% over two days through July 8, its largest upside move since mid-April, briefly topping $80/bbl intraday, up from an intraday low of $70/bbl on July 2. Front-month heating oil gained nearly 12% over two days, aided by a Russian diesel export ban. This runs against the disinflationary energy narrative that dominated the prior month.

- Rate Hike Expectations: Renewed concerns of energy inflation pressure has lifted yields, with the 10y testing 4.6% (a high since May). The 2y pushed back to 4.24%, in line with recent highs. CME Fed Funds futures now price at least one rate hike at an 85% probability, and a 47% chance of at least two hikes by year end. We continue to expect one hike this year as our base case.

Market Analysis

On July 8, in comments made to reporters at the NATO Summit, President Trump indicated that the US – Iran MoU signed on June 17, was effectively no longer in force. While the US would continue to pursue negotiations, the ceasefire has ended. The President’s comments came after a night of intense US bombing along the Strait of Hormuz, an action that was met by Iranian attacks on Bahrain and Kuwait. The US also moved to reinstate sanctions on Iranian crude exports. As this report was ready to be published (4pm CT), the US had begun a second night of strikes with Iran vowing more retaliation.

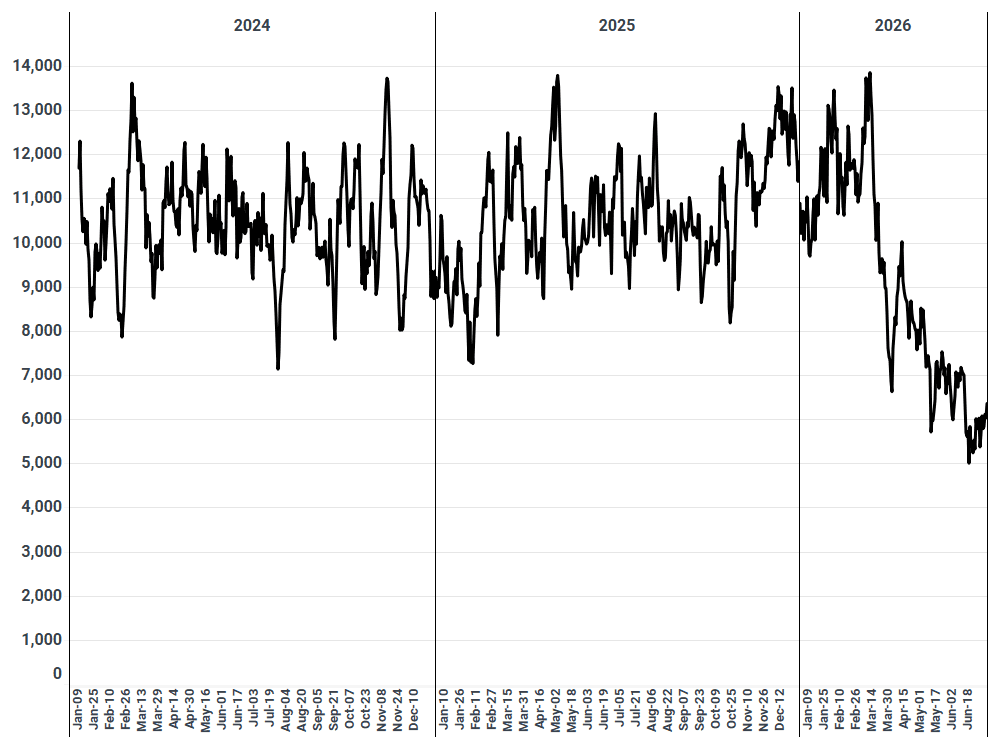

In the four week period leading up to the NATO summit, oil markets appeared to be stabilizing. Front month Brent prices, which were trading in the mid-90s/bbl in early-June, had fallen to levels near $71/bbl as of July 6, marking a decline of roughly $25/bbl in less than a month. This price move reflected physical market realities. Crude/co exports transiting the Strait of Hormuz rose to 5.7 Mbd in June, up from an average of just 1.8 Mbd over March, April, and May. Through the first week of July, crude/co transits continued to look strong, holding at 8.9 Mbd. Weak Chinese demand also helped to keep the market in balance with seaborne imports remaining below 7 Mbd, well under a historical average level of 10.4 Mbd.

Daily Chinese Seaborne Crude/Co Imports (kbd, 10-day MA)

Source: Kpler

However, generally bearish oil market sentiment over the past month has shifted over the past two days through July 8. Trump’s comments at NATO briefly pushed Brent back above $80/bbl intraday, before prices eased back towards $79/bbl. Even with the intraday retracement, front month Brent was up more than 8% over two days, the largest upside move since mid-April. Further out prices were also lifted - the Brent December 2026 contract briefly traded above $78/bbl, the highest level since June 22.

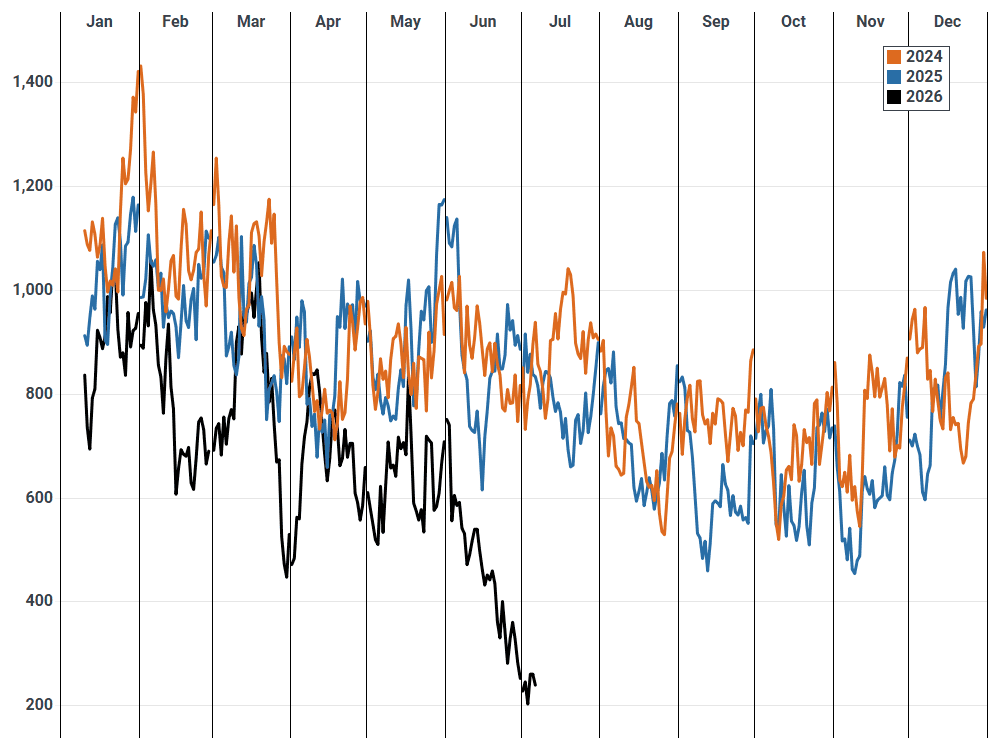

Clean product prices have also surged, particularly for diesel. The front month US heating oil contract traded up to an intra-day high of $3.77/gal before backing off a bit to $3.67/gal, marking a 2-day gain of more than 12%. Higher oil prices, combined with a Russian diesel export ban provided plenty of bullish sentiment. US front month RBOB (gasoline) prices were also up 3.7% over the past two days. Russian seaborne diesel exports have steadily declined since early-June.

Daily Russian Seaborne Gasoil/Diesel Exports (kbd, 10-day ma)

Source: Kpler

Rising oil and clean product prices run against the disinflationary energy narrative that has dominated for the better part of the month. This is creating upside pressure on yields, with more movement seen in longer duration. The 10y yield, which has been relatively well anchored over the past month amid Fed hawkishness, and declining energy prices, pushed to an intraday high of nearly 4.6% on July 8 marking the highest level since May. The 2y yield also tested an intraday high of 4.24%, at the top end of the 12-month range.

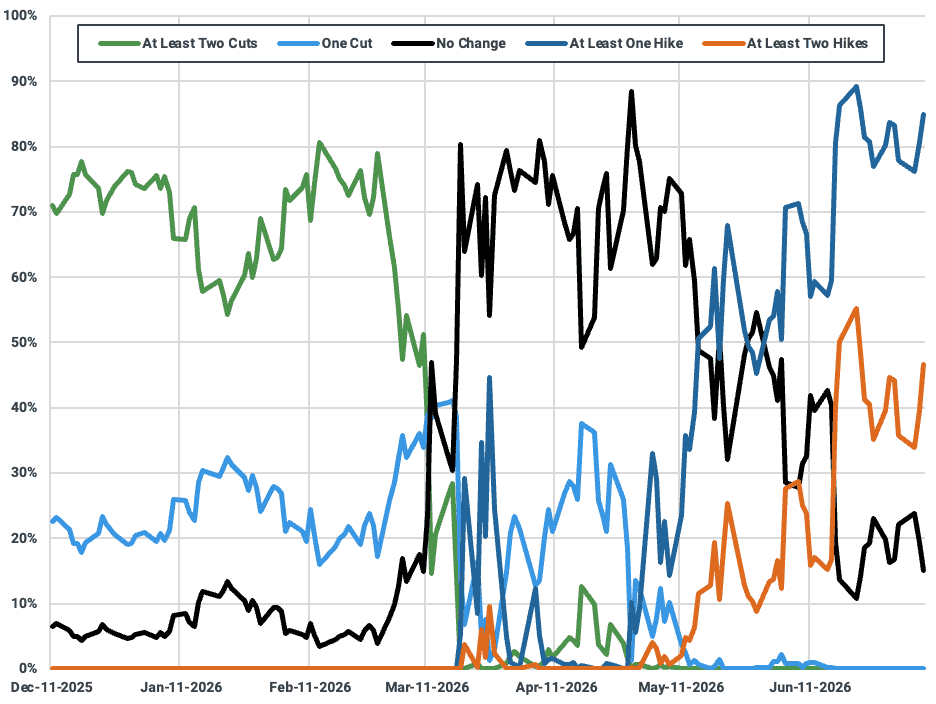

Expectations for a Fed rate hike also remain firmly entrenched. CME Fed Funds rate futures are tagging an 85% chance of at least one rate hike, and a 47% probability of at least two rate hikes by year end. The market no longer believes that rate cuts are a possibility. Our view is that the Fed will hike once this year, with the possibility of another hike in H1 of next year. The Fed is not about to begin a prolonged hiking cycle.

Fed Funds Path Probabilities by End-2026

Source: CME

See why the most successful traders and shipping experts use Kpler