How Europe rebalanced its jet fuel supplies to keep planes in the air

Europe’s jet fuel market has proven more adaptive to the Hormuz disruption than initially feared. Despite the abrupt loss of ~400 kbd of Middle East supply into a structurally short region, rapid supply-side adjustments such as higher US exports, the Dangote refinery ramp-up, and elevated European refinery jet yields have offset a substantial share of the disruption. While the market still remains undersupplied and inventories continue to draw, the resulting deficit has so far been materially less severe than initial fears of a broader aviation fuel crisis across Europe.

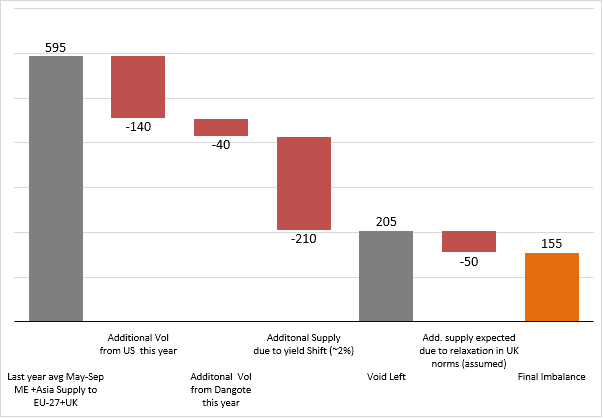

Europe (EU-27 & UK) are structurally short in jet fuel, relying on imports of ~700 kbd to meet aviation demand. Last year avg. of ~400 kbd of these supplies originated from the Middle East during the summer months (May-Sep 25). The escalation of the conflict and the effective closure of the SoH abruptly disrupted this key trade corridor, initially raising concerns over a severe supply deficit.

Yet the disruption has, so far, proven manageable than initially feared. The adjustment has primarily come from the supply side, where refiners and trade flows have rapidly reorganised to offset a substantial share of the lost Middle Eastern barrels. Below are some of the observed adjustments, that have, so far, proven effective in helping Europe navigate the jet shortage.

Dangote’s RFCC restart: The resolution of RFCC operational issues at Nigeria's Dangote refinery recently allowed the complex to operate near-design-capacity. Kpler forecasted this trajectory as early as February 2026, and the subsequent ramp-up has delivered ~40 kbd of incremental jet fuel supply y/y, which has been rerouted toward Europe.

US incremental exports: The most volumetrically material offset has come from the US, redirecting ~140 kbd of jet fuel y/y toward Europe. The sharp widening of crack spreads following the Hormuz closure incentivised US refiners to elevate jet yields, a shift achievable within the flexibility envelope of US refinery units. Europe's concurrent decision to temporarily accept Jet A grade alongside the standard Jet A-1 removed a persistent grade barrier, widening the pool of eligible US barrels clearing into European airports. That last point remains to be proven operationally viable, nonetheless, as operational scrutiny and limited acceptance among airlines are likely to stymie the effect of this change for the time being.

European refinery yield uplift: The most analytically significant response has come from European operators themselves. Europe’s refiners have optimised their complexes to run in jet max mode, pushing yields from ~9 vol% to ~11 vol%, a ~2 vol% uplift y/y, a trend Kpler has highlighted since the early stages of the Hormuz disruption, and which is now corroborated by the JODI March 2026 data release. At March run rates, this translates into ~160 kbd of incremental domestic supply and is expected to rise to ~210 kbd during May–Sep 2026 as refinery throughput climbs to 10.8 mbd following the wind down of spring maintenance.

Together, the three offsets have recouped the bulk of the ~400 kbd Middle East supply void.

A fragile balance heads into peak season

Nonetheless, although Europe has managed to plug much of the Middle East supply void, it still remains short of ~200 kbd of Asian supplies. Last summer, India supplied 100–130 kbd of jet fuel to Europe, but flows have since come under pressure from tightening restrictions on refined products processed from Russian crude. The UK’s recent relaxation allowing imports regardless of crude origin could partially restore this corridor and recover an ~50 kbd of incremental supply (assumption). Even so, Europe is still expected to enter the summer peak season short by ~150 kbd.

Expected Jet fuel balance over May-Sep26 (in kbd)

Source: Kpler

Higher jet fuel prices have also weighed on demand, triggering the rationalisation of less efficient routes and marginal services. According to Kpler’s demand model, EU-27 & UK jet fuel demand losses are currently expected to average ~50 kbd over May–Sep, with the peak impact occurring in July.

Tight jet fuel supplies during a period when Europe would ordinarily be building buffers has left inventory cover below seasonal norms . With the supply stack dependent on US crack economics and export logistics, Dangote continuity, and above-trend European yields all holding simultaneously, the margin for error is narrow. Any one pillar softening could unwind volumes quickly and with stocks thin to bridge even a short-term miss, the price response would be swift .

The crisis has not played out as badly as feared. But the patchwork holds only as long as every piece stays in place.

How much stock buffer does Europe have left?

Assuming the three supply-side adjustments remain in place, net inventory drawdowns are expected to stay within the 100–200 kbd range through October, when shipping conditions through the Strait of Hormuz are forecasted to normalize. Under that scenario, European jet fuel stocks would bottom out at 50-55 Mbbls, still above the estimated 30–35 Mbbls floor of tank bottoms, unavailable stocks, and minimum working inventory. At a sustained 100–200 kbd draw rate, Europe would not exhaust that buffer until February next year.

Should one of those pillars fail and drawdowns accelerate to a sustained 250 kbd, the current stock level would provide cover only through October–November, a materially tighter outcome. It is worth noting that Europe is not a single integrated system: airport infrastructure and logistics vary considerably by country, and the UK and France, both carrying deep short positions and a higher dependence on Gulf supplies, are the most exposed and could face further disruption earlier than the aggregate picture suggests.

Europe jet fuel/kero stocks (Mbbls), forward cover (days)

Source: Kpler

Market insights you can trust

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

.jpg)