Saudi’s Aug OSP cuts reinforce oversupply concerns as demand recovery falls behind

Saudi Aramco slashed its August OSPs across all regions, setting its flagship Arab Light grade in Asia at a discount to the Oman/Dubai average for the first time since December 2020.

Key Takeaway:

- Despite aggressive OSP cuts, Saudi crude remains more expensive than spot offers from regional competitors such as the UAE, Qatar and Iraq.

- Supply recovery continues to accelerate despite elevated geopolitical risks, with non-Iranian Middle Eastern crude exports so far in July standing only around 2 mbd below pre-war levels.

- Asia's (ex-China) crude intake has recovered to around 95% of pre-war levels, suggesting limited upside, although restocking needs could generate an additional ~300 kbd of crude demand at least.

- China's independent refiners are expected to increase crude purchases and refinery run rates as margins improve. However, it remains to be seen how much of the incremental demand will be captured by non-Iranian and non-Russian crude.

- Overall Chinese seaborne crude imports are expected to recover to around 9 mbd only in early Q4, supported by a gradual recovery in fuel demand and the expected easing of product export restrictions.

The $11/bbl month-on-month cut for Asia came as a surprise to many market participants, bringing Arab Light to a discount of $1.5/bbl against the pricing benchmark. Even so, the OSP remains above the levels at which Aramco had been selling the grade in the spot market. In a rare spot tender last week, Aramco reportedly sold several prompt cargoes to Asian and European refiners, with some China-bound barrels priced at around Dubai plus $1/bbl on a delivered basis, equivalent to roughly Dubai minus $4/bbl FOB.

Despite the large-scale cut, Saudi crude still appears to be priced above several competing Middle Eastern grades, which have been aggressively marketed through spot tenders and private negotiations in recent weeks. For example, August-loading Upper Zakum was sold at discounts of $7–8/bbl to Dubai on an FOB basis during ADNOC's fifth spot tender in June.

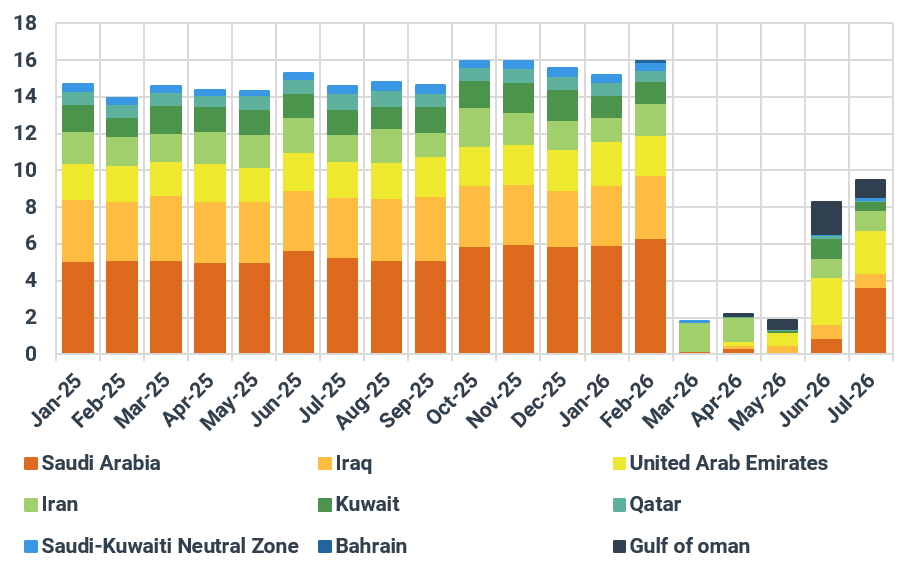

Having said that, Aramco's price cuts reinforce market concerns about oversupply and the potential for a price war, as Middle Eastern supply is recovering faster than demand. Kpler data shows that around 5.67 mbd of non-Iranian crude was shipped out of the Persian Gulf in June, including cargoes that transited the Strait of Hormuz in the dark and then conducted STS operations in the Gulf of Oman, up sharply from 2.1 mbd in May.

So far in July, volumes have continued to climb to 8.55 mbd, driven partly by the ongoing clearance of backlog vessels—which had fallen to around 10 mb at the time of writing—and partly by an increase in new loadings. Saudi Arabia resumed crude loadings from its Ras Tanura terminal in the week beginning 22 June, maintaining a steady pace of around 1.3 mbd since then.

Meanwhile, loadings from Kuwait's Mina Al Ahmadi and Iraq's Basrah terminals have also gradually increased since June, supported by a rise in inbound tanker traffic into the Persian Gulf and the expansion of fleets by oil producers and trading houses to shuttle cargoes to the Gulf of Oman.

Middle Eastern crude/co exports via the SoH by origin, mb

Source: Kpler

In addition, Saudi Arabia and the UAE continue to utilize existing pipeline infrastructure to bypass the Strait of Hormuz, bringing total non-Iranian Middle Eastern crude exports to 14.3 mbd so far in July, just around 2 mbd below pre-war levels.

However, the recovery in demand appears to be lagging behind. Most Asian countries, excluding China, have already recovered to around 95% of their pre-war intake demand levels and 96% of their levels a year ago, suggesting limited upside for further demand growth.

While some countries, such as Japan, are also expected to rebuild depleted crude inventories, the pace is likely to remain modest at around 200–300 kbd even if fully realised, insufficient to reverse the current oversupply dynamic.

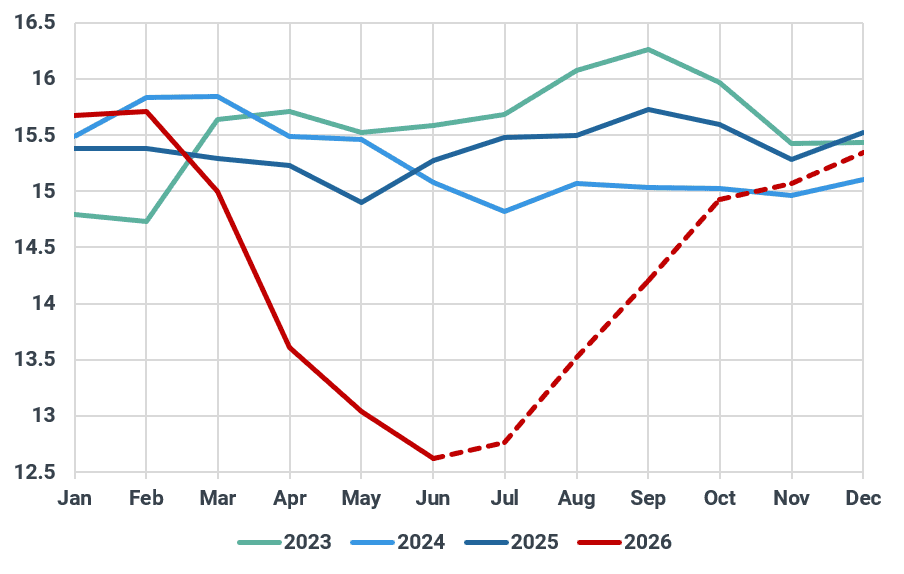

That leaves the elephant in the room—China—which has seen seaborne crude imports fall to 6–7 mbd in May and June, compared with more than 10 mbd before the war. As benchmark crude prices have declined following the US-Iran interim peace agreement and spot differentials have plunged to multi-year lows amid rising supply, Chinese refiners have become increasingly active in the spot market in recent weeks.

However, it remains to be seen whether this represents merely opportunistic buying or a structural shift in procurement, given that refinery crude demand—particularly among China's state-owned refiners—is still expected to remain 1.5–2 mbd below pre-war levels in August and September.

Notably, at least three Chinese independent refineries (excluding the large integrated refiners) have recently purchased non-Iranian Middle Eastern crude for July- and August-arrival, raising hopes that additional Chinese buying could help ease the current oversupply. However, the volumes purchased so far remain limited at around 5.5 mb in total.

In the meantime, Iranian crude sales have largely been muted over the past two weeks due to uncompetitive pricing relative to the sharp decline in Abu Dhabi, Qatari and Iraqi crude prices. Iranian Light, which had typically traded at around $10/bbl below Upper Zakum on a delivered basis into China, has recently become $2–3/bbl more expensive.

As a result, buyers have pushed back and opted for the cheapest barrels available. In that sense, recent purchases of Middle Eastern crude by China's teapots appear to represent a replacement of Iranian cargoes rather than incremental demand.

As refining margins improve and is expected to remain strong alongside lower feedstock costs and declining product inventories, some independent refiners are expected to increase crude purchases to replenish inventories and raise refinery run rates. Yet, it remains to be seen how much of this incremental demand will ultimately shift toward non-Iranian and non-Russian grades, as sellers of sanctioned crude are expected to lower prices in an effort to regain market share.

Moreover, we do not expect refiners to rush back to higher operating rates. Product export quotas are unlikely to be utilised aggressively while the situation around the Strait of Hormuz remains far from fully resolved, limiting the incentive to maximise product exports. As a result, any increase in refinery runs is expected to be measured rather than rapid. We currently expect refinery throughput to average around 12.9 mbd in July, rising to approximately 13.6 mbd in August and gradually increasing further to around 14.2 mbd in September. This implies a steady recovery in crude demand, but one that is unlikely to be strong enough to materially tighten the regional crude balance in the near term.

That said, a gradual return of Chinese buying is expected to provide some support to crude prices, but it is unlikely to reverse the broader downward trend, as China's seaborne crude demand is not expected to recover to ~10 mbd until early Q4 at the earliest as demand gradually picks up and product export restrictions are likely to be eased. Meanwhile, Middle Eastern producers continue to ramp up output and compete for market share, suggesting that the aggressive price cuts announced by Aramco may be only the beginning.

China's refinery intake demand, mbd

Source: Kpler

See why the most successful traders and shipping experts use Kpler