Stable outlook across global gas benchmarks amid mixed signals and Hormuz uncertainty

Global LNG and natural gas prices are expected to remain broadly stable over the next week, as market participants await potential developments in a second round of Iran–US talks. In Europe, mixed temperature signals—with cooler conditions in the north offsetting warmer trends in the south—are expected to keep demand balanced. In Asia, rising weather-driven demand is likely to be countered by higher nuclear output, limiting upside to prices.

Market & Trading Calls

European TTF front-month price outlook: Stable, Developments in the Mideast Gulf will continue to shape price movements, posing sideways risks around whether Iran and the US return to the negotiation table. Fundamentally speaking, an increase in pipeline supply and stable LNG imports is expected to balance a strong decline in wind generation in NW, Southern, and SEE. Meanwhile, temperature forecasts are showing mixed signals, anticipating a drop in temperatures in the Baltics and Northern Europe and warmer trends in the south, while the contract rollover into June will also put downward pressure on the benchmark.

Asian LNG front-month price outlook: Stable, as forward weather-driven demand in Japan and Thailand offsets soft near-term fundamentals, with Korea’s nuclear ramp-up, stable China, and weaker Singapore demand keeping spot activity muted. On the supply side, a first LNG cargo from US’ Golden Pass, recovering Australian exports, and steady LNG Canada flows lift Pacific availability, but Hormuz disruptions, alongside security-driven buying, keep the balance tight and prices rangebound.

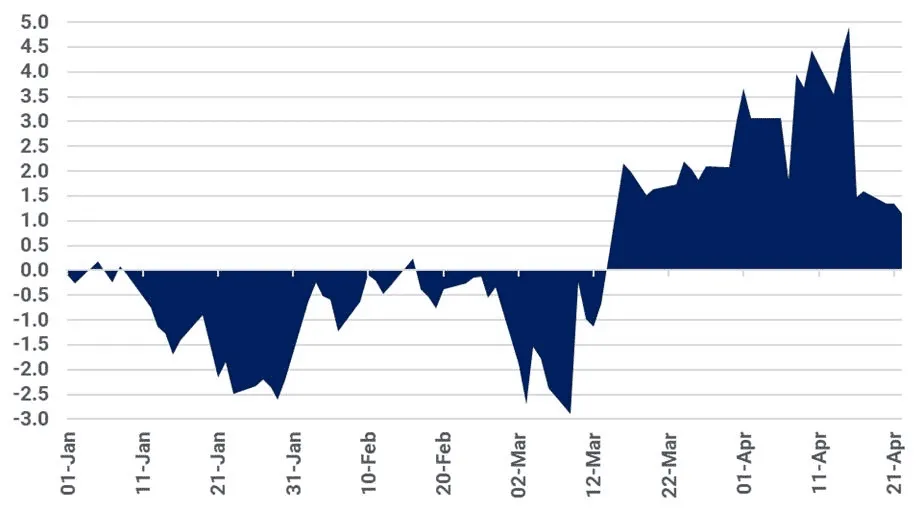

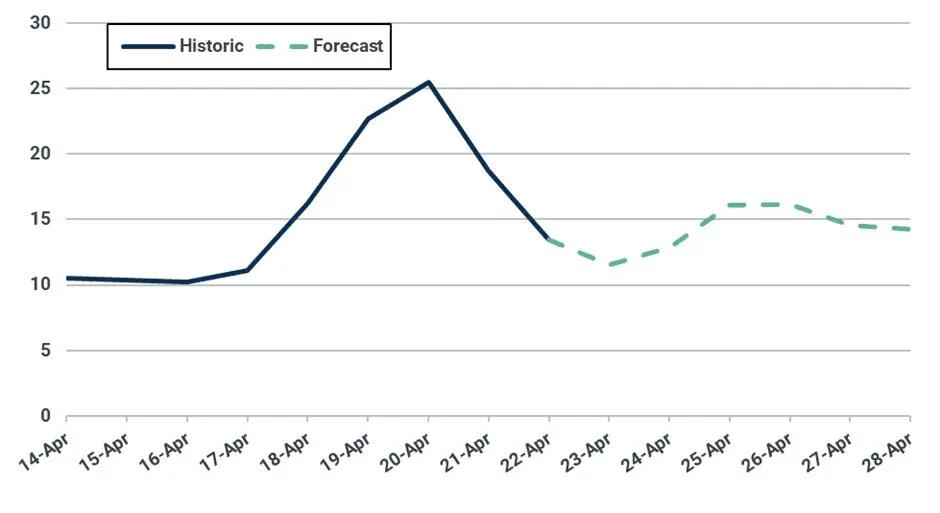

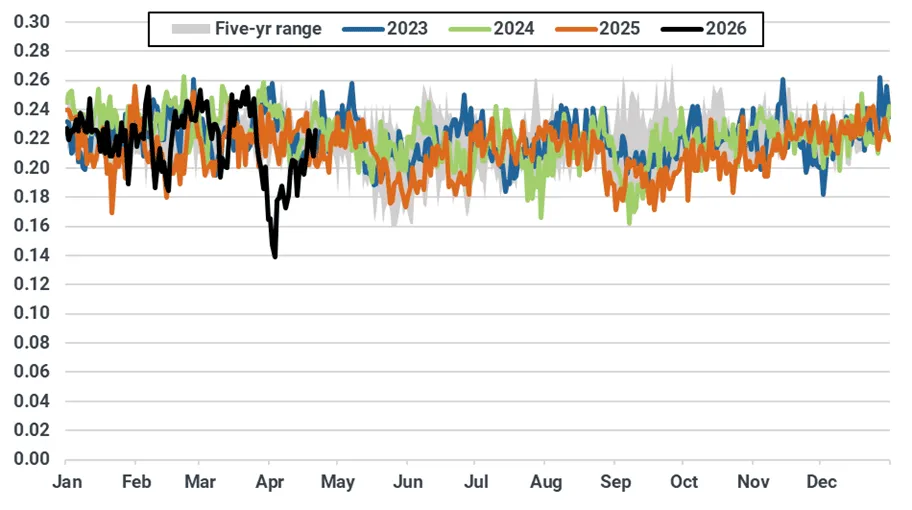

Asian LNG – TTF spread outlook: Stable, as both Asian LNG and TTF prices are anticipated to trade rangebound. Asian LNG prices kept a premium of $1.15/MMBtu over TTF on 22 April (-$3.76/MMBtu w/w).

US Henry Hub front-month price outlook: Stable, as continually weak fundamentals and seasonally strong storage injections counter slightly lower production and low price-driven buying.

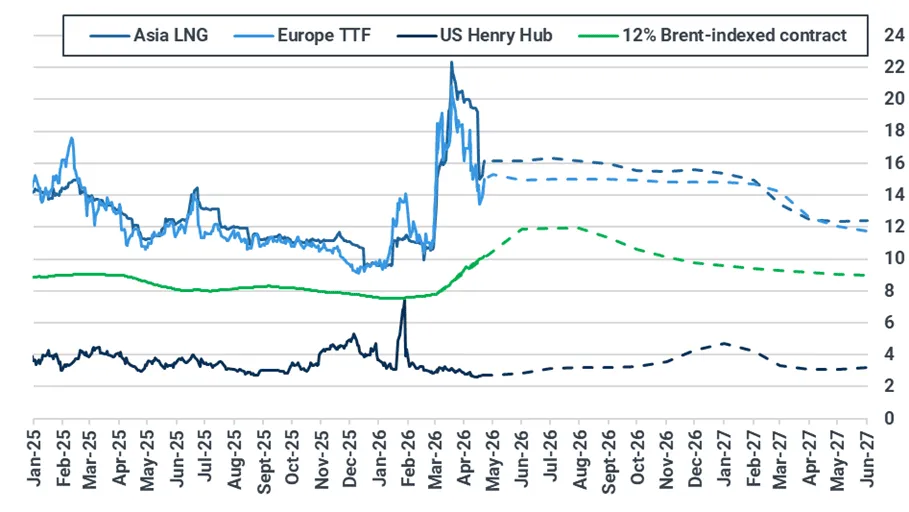

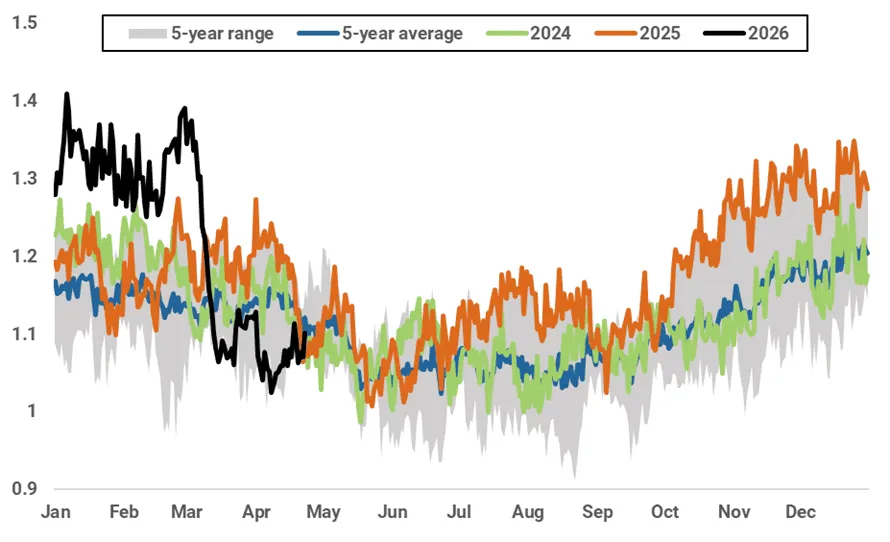

Key natural gas and LNG front-month prices ($/MMBtu)

Source: ICE, NYMEX. Brent-indexed price represents 12% slope of 90-day moving average of Brent contract.

Asian LNG-TTF front-month spread ($/MMBtu)

Source: ICE, Kpler Insight

Europe: TTF to remain rangebound driven by mixed temperature signals across the continent and a slight increase in pipeline supply

The European TTF front-month contract rose to $14.98/MMBtu on 22 April, a 5% increase from $14.29/MMBtu on 15 April. Prices declined on Friday after the announcement that the Strait of Hormuz would reopen for the remainder of the ceasefire period. However, this possibility vanished during the weekend following attacks on several vessels that attempted to cross the Strait. This supported prices from Monday onwards, alongside downward revisions to temperatures in parts of Europe. Pipeline and LNG imports were lower w/w, although consumption also decreased despite a short-lived cold snap.

Looking ahead, Kpler Insight maintains a stable outlook on the TTF front-month contract for next week. Developments in the Mideast Gulf will continue to shape price movements, posing sideways risks around whether Iran and the US return to the negotiation table. Fundamentally speaking, an increase in pipeline supply and stable LNG imports is expected to balance a strong decline in wind generation in NW, Southern, and SEE. Meanwhile, temperature forecasts are showing mixed signals, anticipating a drop in temperatures in the Baltics and Northern Europe and warmer trends in the south, while the contract rollover into June will also put downward pressure on the benchmark.

On the supply side, EU net pipeline imports declined by 3.7% w/w to an estimated 2.86 bcm. The drop was driven by lower flows from Norway as one day of heavy maintenance at the Troll field restricted flows to the continent, in particular to Germany. Additionally, flows from the Turkstream pipeline also fell, partly as a result of maintenance taking place at the Kulata IP between Greece and Bulgaria. While imports from the UK declined, mostly driven by Norwegian maintenance and planned works at Saint Fergus. The losses more than offset the gains observed in Algerian exports to Europe, while Libyan flows to Italy remained at zero, likely due to planned maintenance being conducted at one of the compressors of the Mellitah complex until 28 April.

Looking ahead, Kpler Insight expects pipeline imports to increase slightly as unavailable capacity from Norway is anticipated to be lower w/w, as well as the possible return of Libyan supply if maintenance ends as scheduled. Exports to Ukraine are expected to remain stable, as high prices, seasonally weak consumption, and healthy UGS levels limit the appetite of Ukrainian buyers. Auctions for May deliveries allocated zero volumes via the Polish, Slovak and Route 1/2/3 routes.

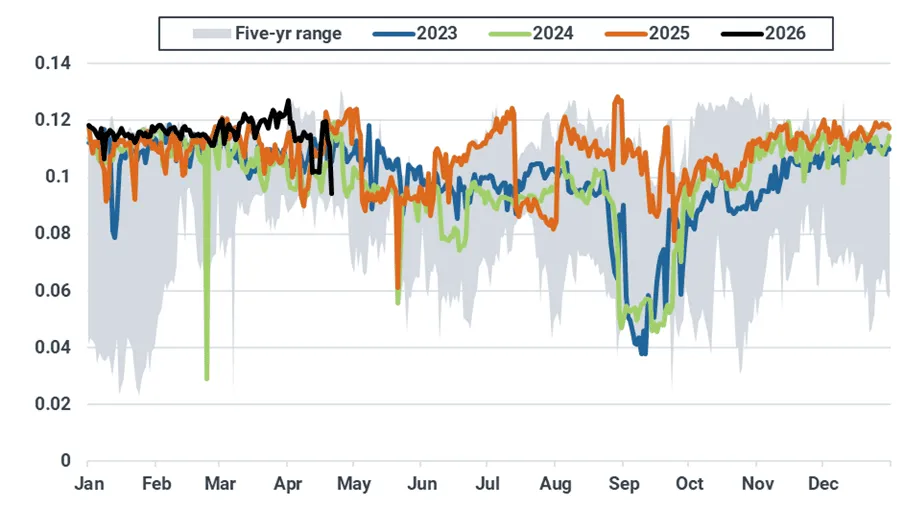

Daily Norwegian pipeline exports to Germany (bcm)

Source: Kpler European Gas, Kpler Insight.

EU-27 LNG imports decreased 15.1% w/w to 2.08 mt, mostly driven by lower imports into Iberia, partly due to ongoing planned maintenance at Spanish terminals, lower exports from Algeria, and increased competition with NWE terminals.

Despite the increase in imports, send-out levels remained relatively stable at EU-level supported by a decline in LNG inventories w/w. Looking ahead, Kpler Insight expects European LNG imports to remain stable w/w, as maintenance at LNG terminals in the region is anticipated to be lighter, however this will be balanced by the lagging effect of a decline in Atlantic LNG supply in recent weeks and sustained competition from Asian players.

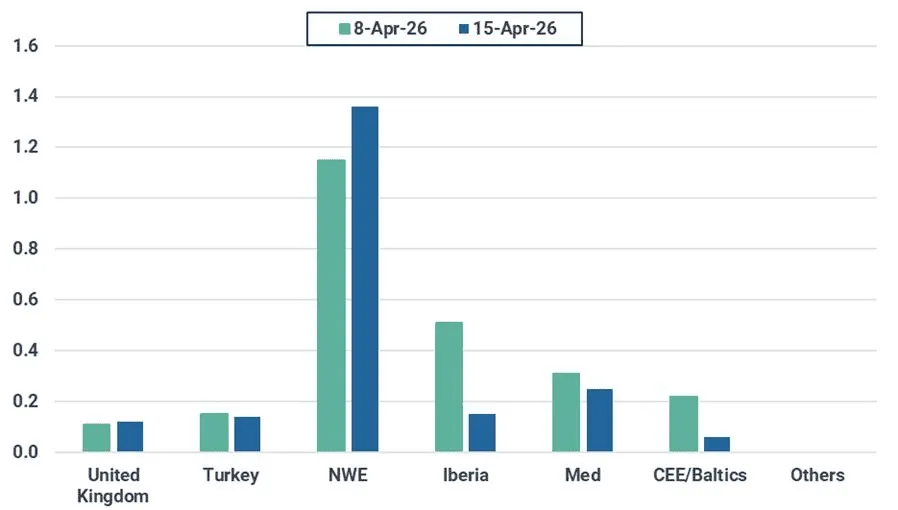

European weekly LNG imports by region (mt)

Source: Kpler Insight. Data represents week commencing 01/04 and 08/04. NWE=FR, BEL, NL, GER. Iberia=ESP, POR. Med=ITA, HVR, GRE. Baltics/CEE=FI, LT, POL. Others=SWE, MT.

On the demand side, aggregate local distribution consumption across 16 EU countries declined by 16% w/w to an estimated 2.09 bcm. Consumption fell w/w in all countries except in Greece, which saw a 19% gain w/w on the back of lower-than-average temperatures. Looking ahead, Kpler Insight expects heating demand to decrease slightly next week as anticipated declining temperatures in the Northern part of the continent should be more than offset by warmer trends in the South of Europe.

EU-16 weekly consumption in the local distribution sector (bcm)

Source: ENTSOG, ENAGAS, Eustream, AGCM, Kpler Insight. The EU-16 perimeter includes AT, BE, DE, CZ, FR, HU, GR, IT, NL, LU, PL, PT, RO, SL, SK, and ES.

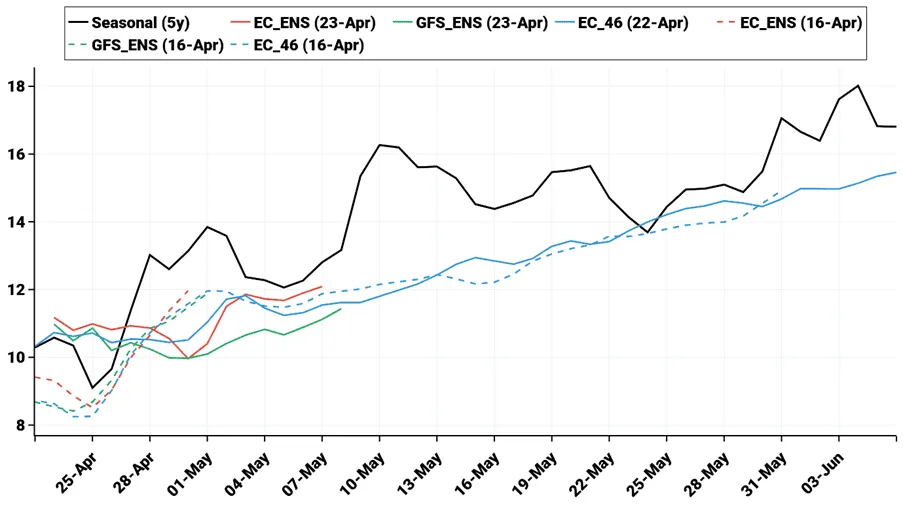

Average forecast temperatures for NWE, excluding the UK (°C)

Source: Kpler Insight. Run comparison 23/04 (solid) vs. 16/04 (dotted), 00:00 UTC. Seasonal is a five-year average. NWE includes BE, NL, FR, DE

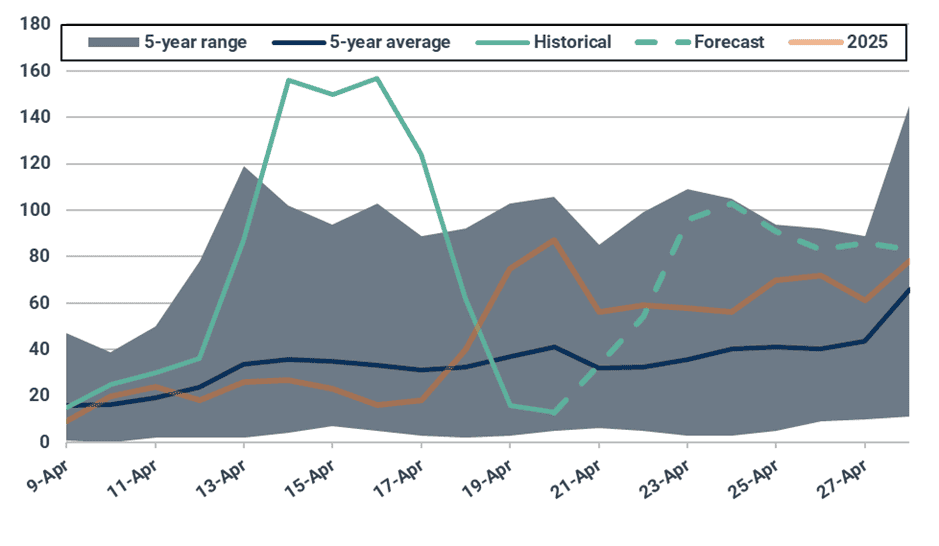

Turning to the power sector, EU-25 gas-fired generation decreased to 5.3 TWh (-6% w/w), driven by a reduction in power demand as well as strong solar generation. Looking ahead, we anticipate a stable outlook for gas-fired generation driven by a sharp decline in wind speeds across the continent, which could be balanced by strong solar generation.

EU-25 weekly gas-fired generation (TWh)

Source: Kpler Power, Kpler Insight.

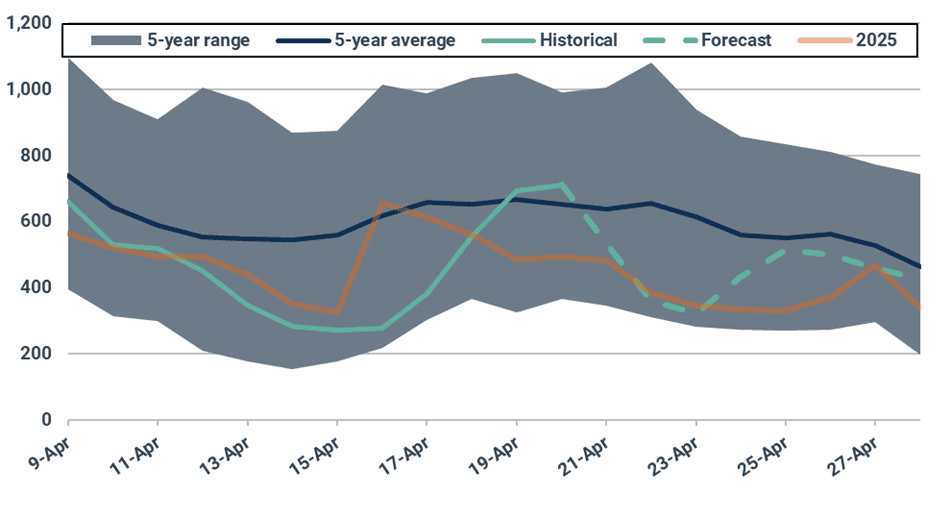

EU-27 underground gas storage levels rose to 30.7% (5.8 percentage points lower y/y), with a slowdown of net UGS injections towards the end of the week driven by lower supply and a decline in temperatures in parts of Europe. So far, cumulative net injections have been above the five-year average and April last year. Looking ahead, Kpler Insight expects this trend to continue into next week as more supply is added to the system while demand is anticipated to remain capped.

EU-27 net cumulative daily injections (bcm)

Source: GIE, Kpler Insight. Latest data as of 21 April 2026.

Asia: LNG prices to stay stable as weather-related demand offsets nuclear gains and soft Northeast Asia fundamentals

Asian LNG prices fell sharply to $16.13/MMBtu on 22 April from $19.20/MMBtu on 15 April, with the decline largely driven by the contract rollover on 16 April and a more cautious, wait-and-see market stance rather than a fundamental shift in balances. Expectations for near-term demand—particularly for June—were pushed back, delaying buying interest. Since then, prices have stabilized in the $15–16/MMBtu range, as weak spot demand and sidelined buyers offset ongoing geopolitical risks around the Strait of Hormuz.

Asian LNG prices are expected to remain stable next week, as forward weather-driven demand—notably in Japan and Thailand—balances soft near-term fundamentals elsewhere. While higher temperatures are expected to support summer cooling demand, this is offset by Korea’s nuclear ramp-up, stable Chinese demand, and weaker Singapore LNG needs, keeping spot activity muted across Northeast Asia.

On the supply side, incremental LNG supply additions from US’ Golden Pass and recovering Australian exports, alongside steady LNG Canada flows, are increasing Pacific Basin availability, but ongoing Hormuz disruptions limit the net bearish impact. At the same time, security-driven buying and supply risks provide a floor, keeping the overall balance tight and prices rangebound.

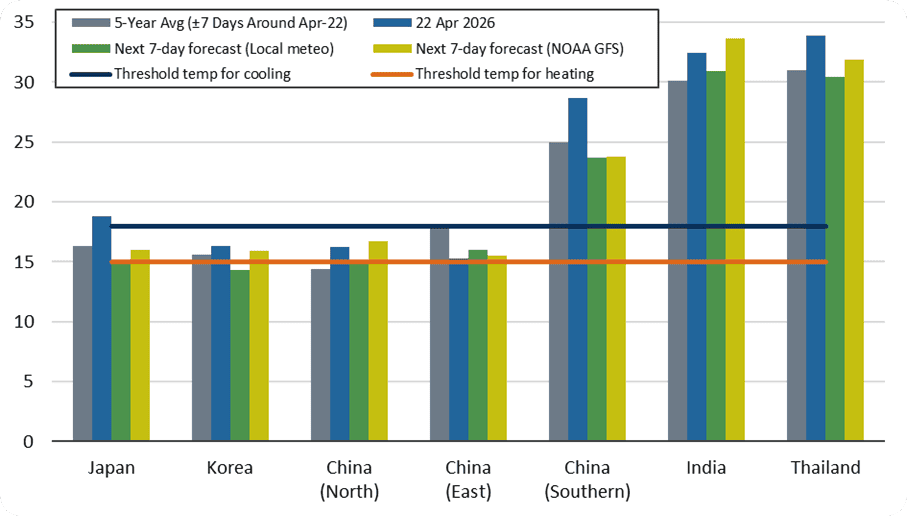

Next week, near-term temperature signals remain soft, limiting immediate demand upside. Northeast Asia stays slightly below seasonal norms, with Japan and Korea near the heating threshold—insufficient to trigger cooling demand. China and Thailand remain warm but milder than usual, capping heat-driven consumption, while only India stays above normal, offering limited offset. This keeps prompt LNG demand muted in the week ahead.

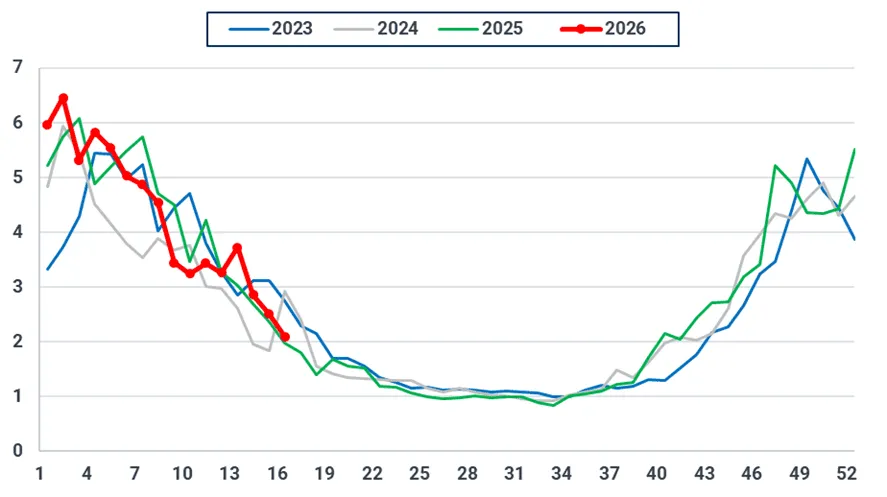

Forecasted average temperatures for Asian countries (°C)

Source: Meteostat, Kpler Insight. As of 23 April 2026 00:00:00 UTC. Population-weighted average temperature of selected major cities across a country is shown for both historical and forecast.

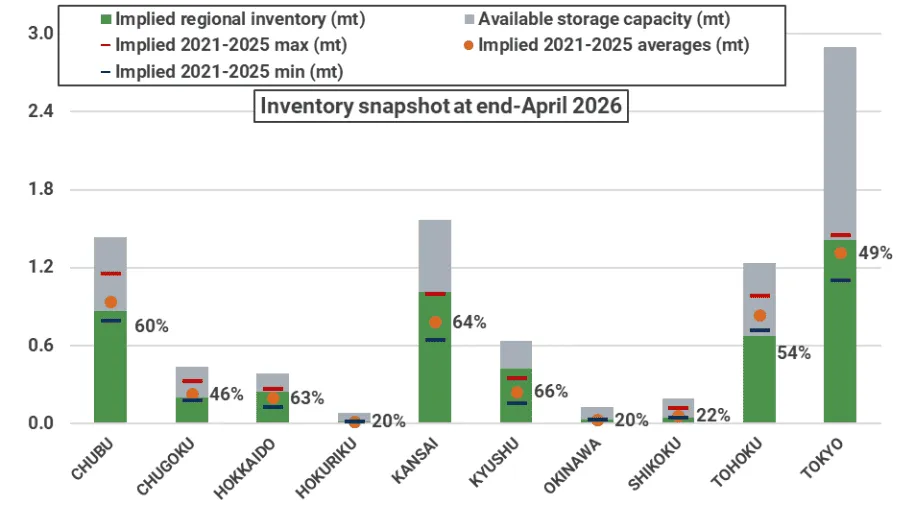

Japan’s major utility LNG stocks remain comfortable at 2.22 mt, down 3% w/w, with the draw reflecting lower imports rather than stronger consumption. Implied total inventories are projected at 4.9 mt by end-April, above seasonal norms, despite localized tightness in Tohoku prompting some incremental buying. Hotter and more humid weather is expected to lift LNG demand through May-July, but the commercial restart of the Kashiwazaki-Kariwa Unit 6 nuclear unit and healthy inventory levels are set to limit additional spot buying. As a result, Japan provides underlying demand support regionally, but not enough to trigger a sustained rally, keeping Asian LNG prices broadly rangebound.

Implied total LNG inventories in Japan (mt)

Source: METI, Kpler Insight

Japan’s implied total LNG inventories by region – April 2026 snapshot (mt)

Source: METI, Occto, Kpler Power, Kpler Insight

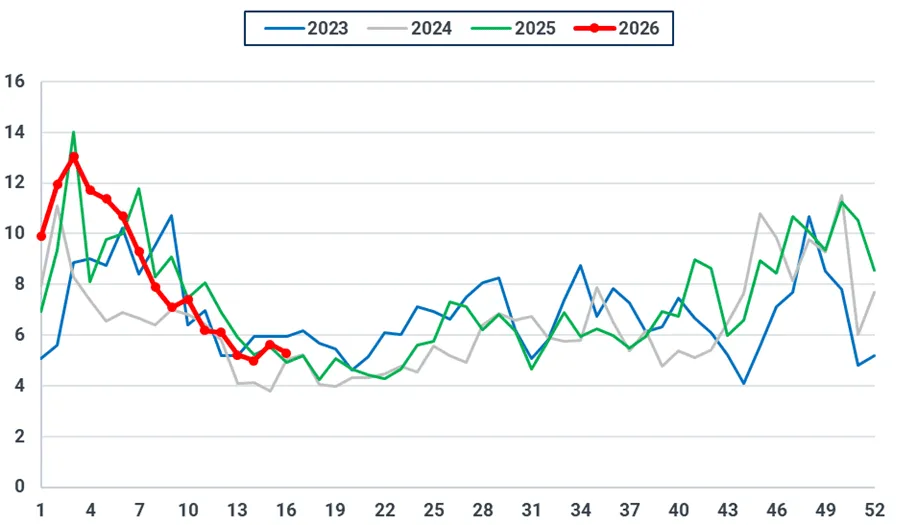

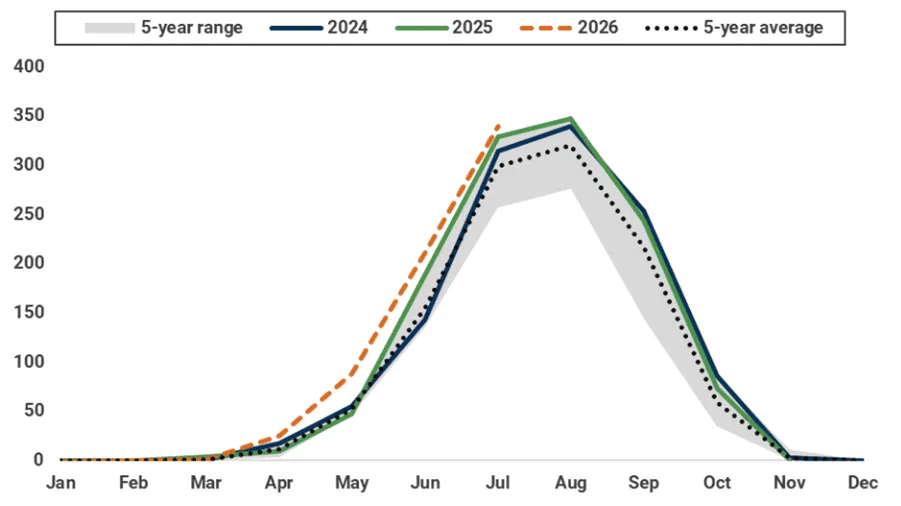

Population-weighted apparent CDDs in Japan (degree-days)

Source: Meteostat, Kpler Insight. Note: Population-weighted CDD of selected major cities across Japan is shown for both historical and forecast.

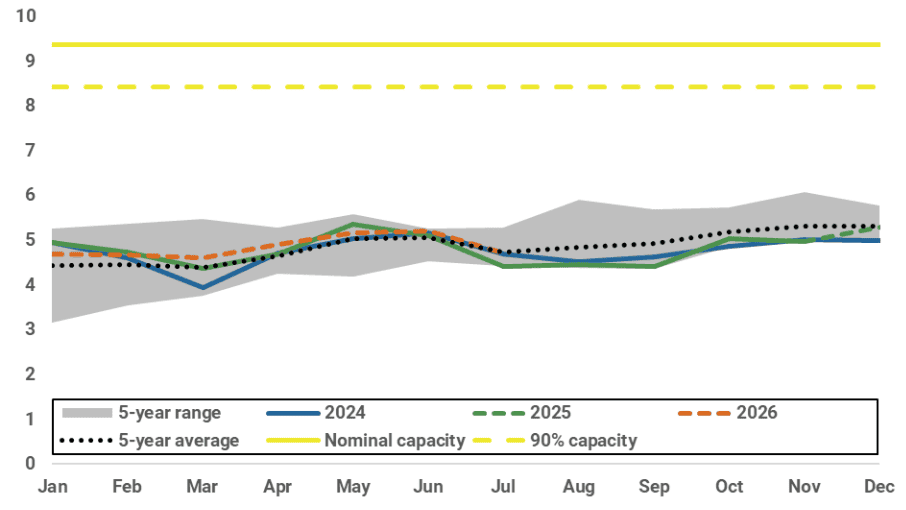

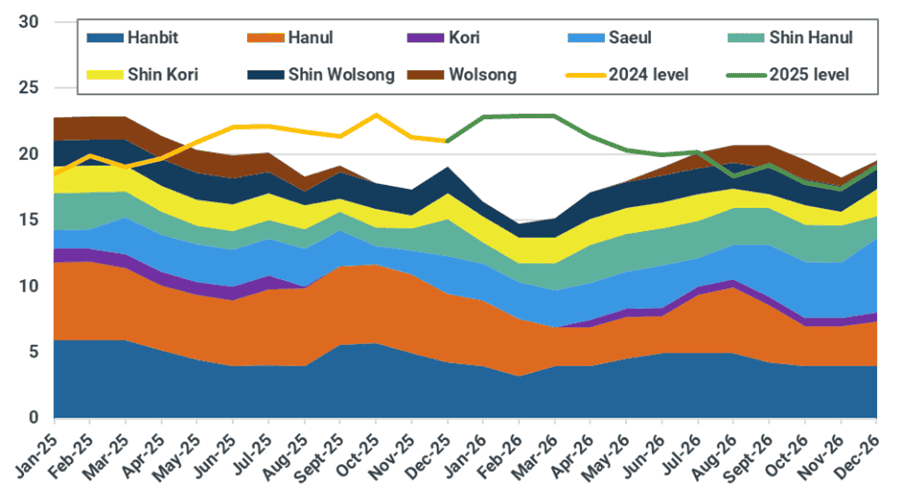

In South Korea, the LNG demand outlook has been revised down by 0.3 mt, as deferred nuclear maintenance and the ramp-up of the Saeul 3 nuclear unit largely offset stronger summer cooling demand. Implied LNG inventories are expected to rebuild from 2.8 mt at end-April to 3.2 mt by July, moving closer to five-year averages. This reduces urgency for spot procurement, with Korean buying likely to slow into mid-summer and cap upside into Q3.

Korea available nuclear capacity by plant (GW)

Source: KHNP, Kpler Insight. Note: Forecast period starts from April 2026.

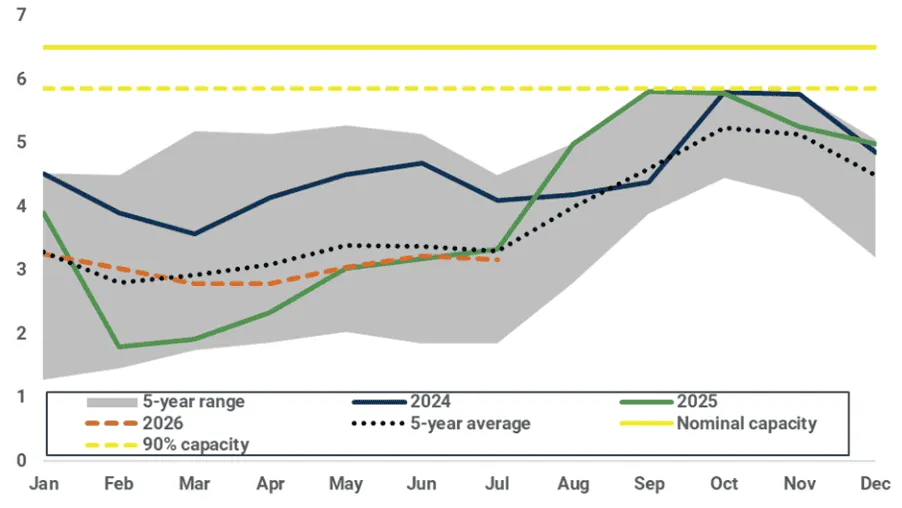

Implied total LNG inventory in Korea (mt)

Source: Kpler Insight, KESIS

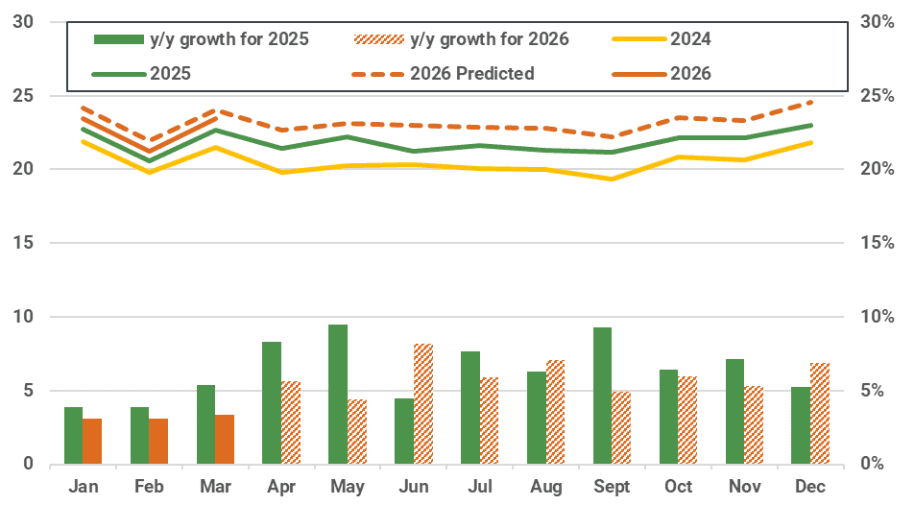

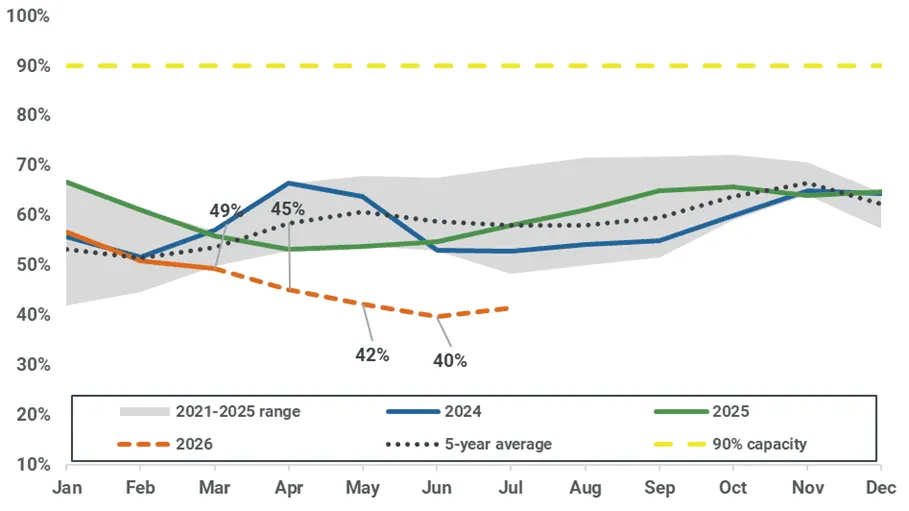

In China, LNG demand remains unchanged at 62.5 mt, supported by steady domestic gas production, resilient pipeline imports, and a stable macro outlook (4.5% GDP growth). This continues to cap near-term spot demand, but the softness is temporary: inventories are expected to fall below the five-year range, prompting a return to spot buying from June–July. China therefore shifts from a near-term drag to a key source of early Q3 price support.

China monthly gas production forecast and year on year growth (LHS bcm, RHS %)

Source: NBS, Kpler Insight

Estimated China pipeline monthly gas imports by country (bcm)

Source: China Customs, Kpler Insight *Note: Data from 2022/1/1 onwards are Kpler Insight estimates, as China Customs stopped publishing pipeline gas import volumes by country

China implied LNG inventory forecast (%)

Source: Kpler Insight

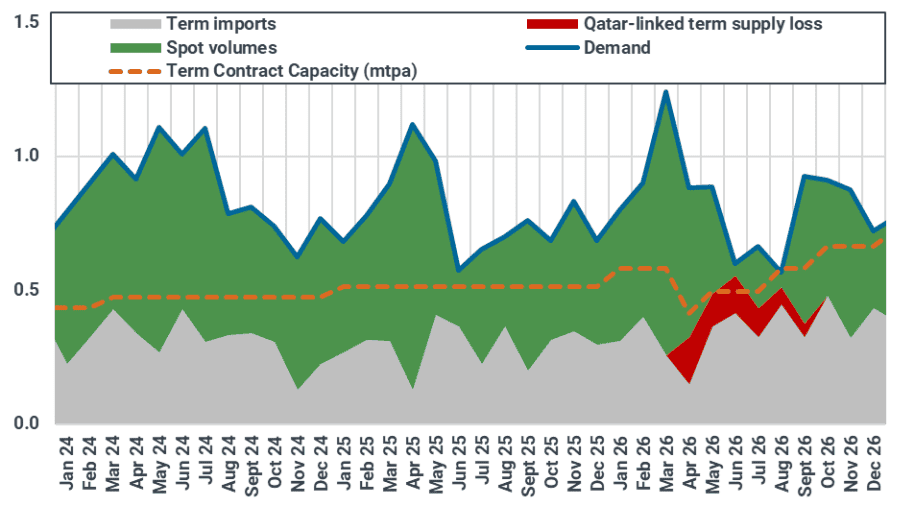

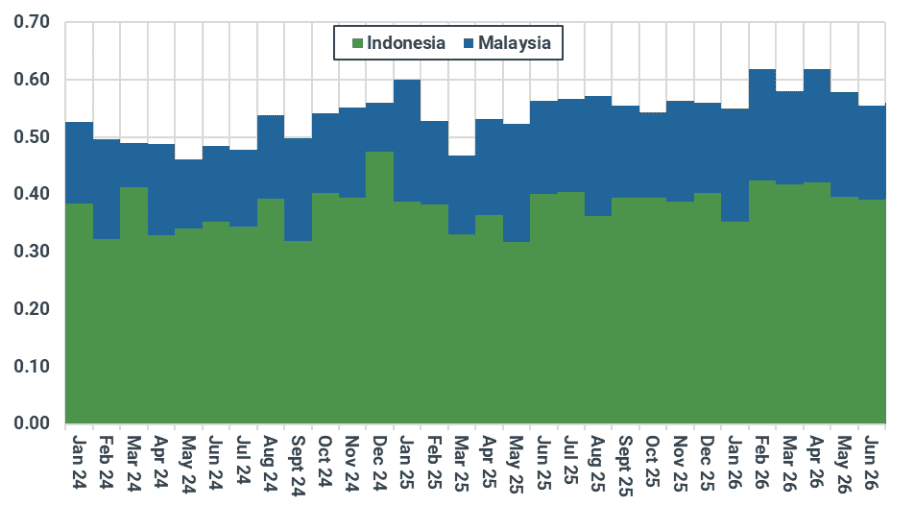

In Southeast Asia, Thailand’s 0.3 mt LNG demand increase is driven by stronger cooling demand, flat domestic gas supply, and declining pipeline imports from Myanmar, pushing incremental demand directly into LNG and back into the spot market. Singapore’s LNG demand is revised lower (-0.2 mt), driven by stronger short-term pipeline inflows from Indonesia and Malaysia, but ongoing Hormuz-related risks are forcing continued spot buying to secure replacement cargoes. As a result, the region provides a demand floor through weather-driven and security-driven procurement, supporting prices.

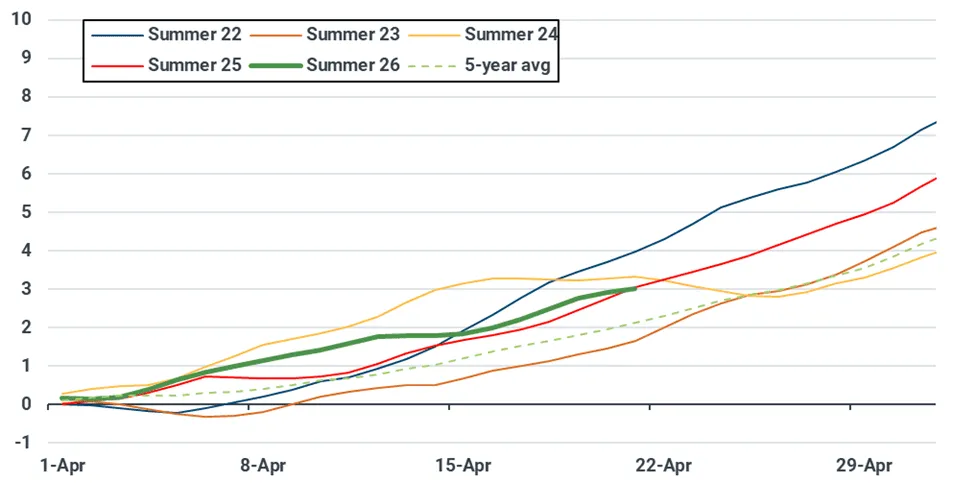

Population-weighted dry-bulb CDDs in Thailand (degree-days)

Source: Meteostat, Kpler Insight. Note: 1) Population-weighted CDD of selected major cities across Thailand is shown for both historical and forecast. 2) Dry-bulb CDD is based off the actual air temperature measured by a thermometer

Thailand’s LNG imports by trade type (mt)

Source: EPPO, Kpler Insight. Note: 1) Orange dotted line represents the overall SPA contract capacity in mtpa; 2) The Qatar-linked term supply loss (red area) due to Hormuz-linked disruptions is expected to be replaced by spot imports (green area).

Additional support is emerging from South Asia, where Pakistan’s return to the spot market (three prompt cargoes)—alongside continued buying from Bangladesh—reflects supply disruptions linked to reduced Middle East flows. This price-insensitive, security-driven demand is tightening prompt availability and reinforcing a floor for spot Asian LNG offsetting weaker fundamentals in Northeast Asia.

Overall, the market remains rangebound: near-term demand softness and high inventories cap upside, while weather-driven demand, security buying, and supply risks provide a firm floor, with upside risks building into early Q3.

Singapore’s monthly pipeline imports by country (Bcm)

Source: JODI, UN Comtrade, Kpler Insight

Singapore’s LNG imports by trade type (mt)

Source: JODI, Kpler Insight. Note: 1) Orange dotted line represents the overall SPA contract capacity in mtpa; 2) The Qatar-linked term supply loss (red area) due to Hormuz-linked disruptions is expected to be replaced by spot imports (green area).

US: Henry Hub to hold near current levels as weak demand offsets lower supply, bargain buying

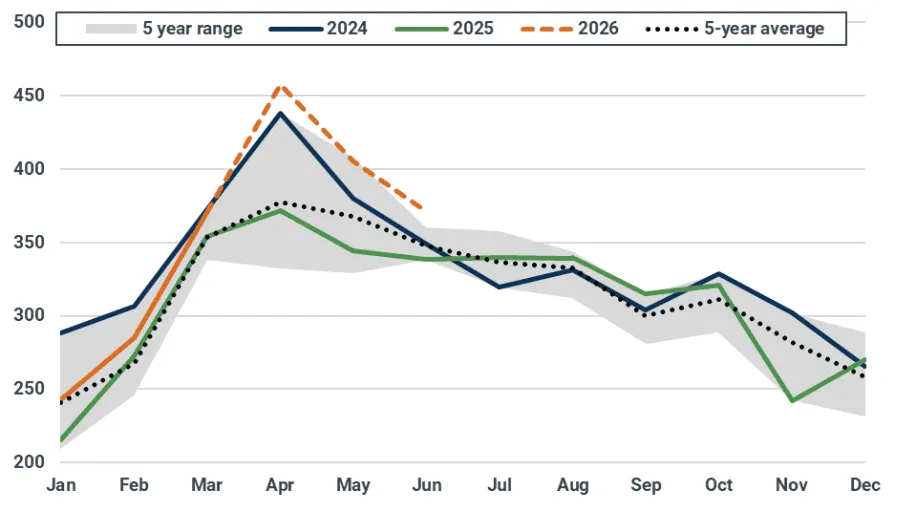

US Henry Hub front-month prices settled at $2.71/MMBtu on 22 April, up from $2.61/MMBtu on 15 April. While near-term cold in the Midwest and Northeast alongside lower production led to modest price gains throughout last week, overall bearish fundamentals continued to drive the market. A moderate rise in heating demand in the north was mostly offset by milder temperatures in the Southwest curtailing early season cooling requirements. Additionally, another above-consensus net injection into underground storage limited upside even as numerous traders took up short positions.

Henry Hub prices are expected to remain rangebound between $2.60-2.80/MMBtu for the coming week as weak shoulder season demand and robust storage injections counteract slightly lower domestic production and the start-up of Golden Pass LNG, which exported its inaugural cargo on 23 April.

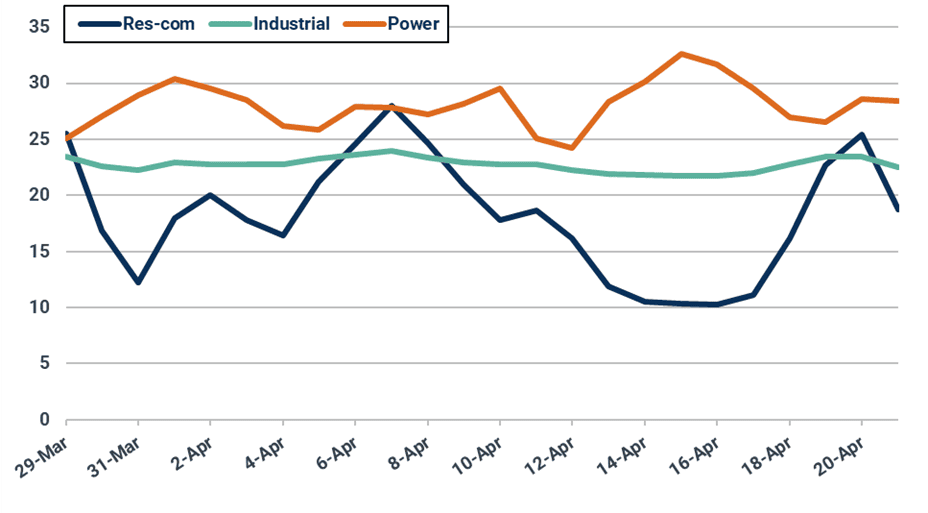

US domestic gas consumption by sector (bcf/d)

Source: EIA

Residential and commercial heating demand rebounded from recent lows near 10 Bcf/d to 25 Bcf/d over the weekend as a cold front drifted over the Midwest and Northeast. Though heating needs are set to fall in the coming days, lingering cold in the Northeast is expected to keep demand near 15 Bcf/d through the end of the month and into early May. While cooling degree days are forecast to trend near the top end of the 5-year range, cooling needs are unlikely to meaningfully impact national demand.

Forecast of residential and commercial demand (bcf/d)

Source: National Weather Service

Forecast of heating degree days

Source: National Weather Service

Forecast of cooling degree days

Source: National Weather Service

Dry gas production fell by 1 Bcf/d to 109 Bcf/d over the last week as pipeline maintenance and low prices brought output lower. Some producers have announced modest near-term supply curtailments, citing unsupportive prices and soft demand. Kpler Insight expects production to average between 108-109 Bcf/d over the next seven days.

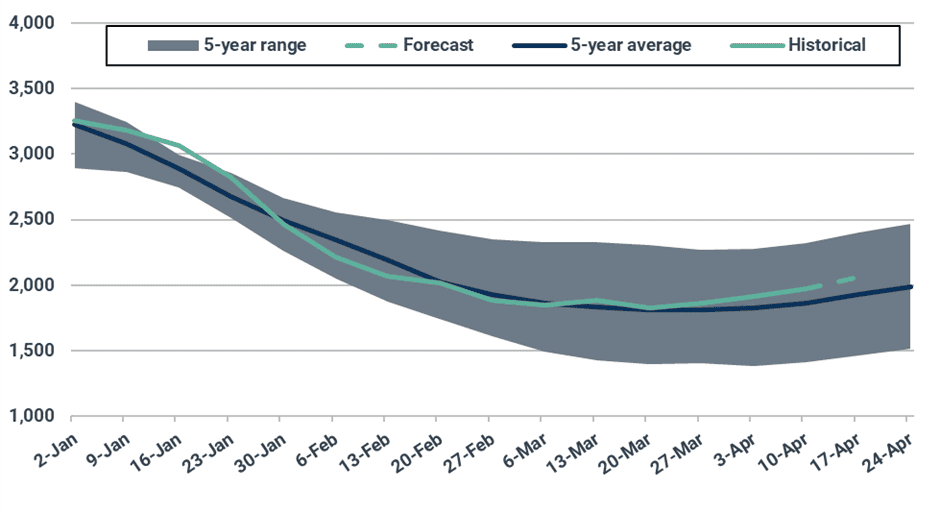

Forecast of natural gas volumes in underground storage (bcf)

Source: EIA, Kpler Insight

The US injected 59 Bcf into underground storage for the week ending 10 April, coming in above consensus and bringing inventories to a 5.8% surplus to the 5-year average. Subdued national demand and robust production during the week ending 17 April are expected to lead to another above average net injection, with Kpler Insight projecting a build of 91 Bcf.

Global LNG Supply: US’ Golden Pass ships first LNG cargo, though feedgas indicates 50% utilization at T1

Global LNG exports held relatively steady last week, increasing by just 0.05 mt to 7.52 mt. Australian LNG loadings rose by 0.39 mt w/w, as facilities on the western coast affected by Cyclone Narelle in late March have returned to full production. This was slightly offset by a reduction in supply from Russia (-0.21 mt w/w), largely stemming from lower loadings at Yamal. Nigeria and Oman LNG exports also slipped by 0.09 mt and 0.07 mt w/w, respectively. Global LNG supply is expected to remain broadly stable next week, only rising once the US’ Golden Pass ramps up and/or Middle Eastern LNG exports restart.

Alongside ongoing monitoring of the Strait of Hormuz transit, Kpler Insight continues to assess feedgas into the 6 mpta US’ Golden Pass T1 which has exported its first cargo, the upcoming restart of production at Australia’s 3.7 mtpa Darwin plant and potential strike action at Australia’s 8.9 mtpa Ichthys plant.

Global LNG exports (mt, 10-day moving average)

Source: Kpler

In the Atlantic Basin, the US’ Golden Pass T1 facility, with a capacity of 6 mtpa, exported its first cargo on board the QatarEnergy-controlled Al Qaiyyah. The impact of one additional cargo on the global gas balance is marginal, with a more meaningful contribution expected as the project ramps up exports.

The start-up of the projectwill provide QatarEnergy with access to more LNG supply following the shutdown of Qatar’s 77 mtpa Ras Laffan facility. Kpler Insight continues to monitor feedgas into the Golden Pass facility. At full LNG production, the train should take in around 0.8 bcf/d, however feedgas is coming in at half of those levels currently. On 22 April, the facility consumed 0.35 bcf of gas.

Kpler Insight expects the two subsequent 6 mtpa trains at the Golden Pass facility to come online in 2027, with delays stemming from the bankruptcy of lead contractor Zachry Holdings in May 2024.

In the Pacific Basin, Australian LNG exports recovered to levels within the five-year range (see chart below). This follows disruption to supply on the western coast in late March due to Cyclone Narelle.

Looking ahead, Kpler continues to monitor the restart of Australia’s 3.7 mtpa Darwin project following maintenance, with a resumption in loadings now expected to take place in early May. According to project operator Santos, the Barossa floating storage and offloading facility (FPSO) is expected to commence ramping up production in the next week, with LNG production expected to commence a few days after. However, there are downside risks to Australian LNG supply if workers at the 8.9 mtpa Ichthys project ballot to take strike action amid ongoing negotiations around pay and workers’ rights. “Members are now getting ready for their next ballot, and we are confident of securing strong support for industrial action,” the Offshore Alliance said. The timeline for a potential strike vote and any subsequent action has not yet been confirmed.

Australia LNG exports (mt, 10-day moving average)

Source: Kpler

Meanwhile in the Pacific basin, loadings at the 14 mtpa LNG Canada plant continue at full speed with a cargo exported every 2 days. This has been the case since 7 April and follows a number of production difficulties at the plant since coming online.

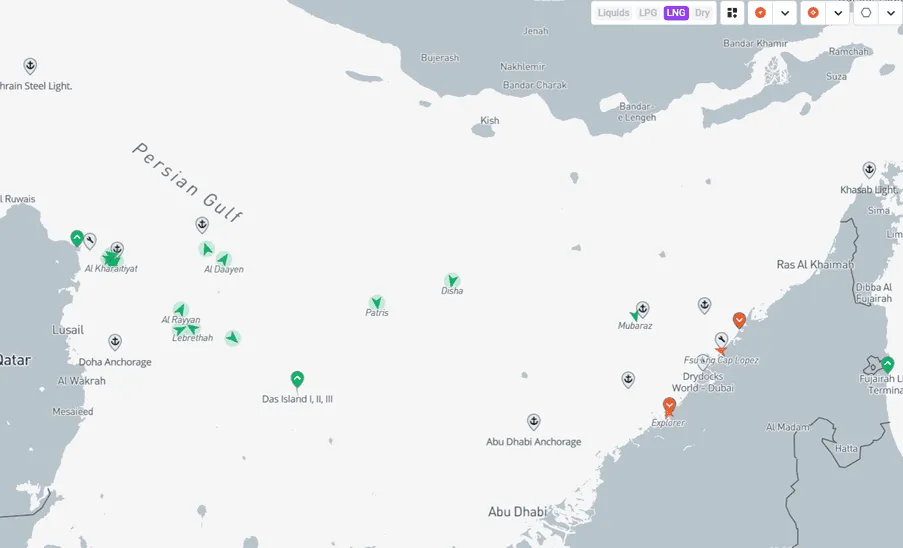

In the Middle East, no LNG tankers have passed the Strait of Hormuz since the ballast Sohar LNG crossed on 2 April. Despite Iran’s claims that the Strait of Hormuz was open to commercial traffic on 17 April, the 5 laden QatarEnergy vessels that approached the entrance of the strait by 18 April failed to transit due to Iranian gunboat attacks. These vessels have now moved away from the Strait of Hormuz entrance back towards Ras Laffan. QatarEnergy has restarted some production at the north site, but there has been limited activity at the south site.

LNG tanker positions in the Persian Gulf

Source: Kpler. Screenshot from 23 April 2026 11.00am BST.

Market insights you can actually trust

Kpler delivers unbiased, expert-driven intelligence that helps you to track critical LNG market developments for your own analysis. Our precise forecasting empowers smarter trading and risk management decisions. In times of conflict and geopolitical uncertainty, our real-time data keeps you ahead of supply disruptions and price volatility.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler