The Illusion of Reopening: What if Iran maintains control?

To restore flows to pre-conflict levels, a full reopening of the Strait of Hormuz must occur without Iranian-imposed conditions on the freedom of vessel movement. This remains unlikely under current dynamics. If Iran retains operational control, transit volumes may increase from current levels but will fall short of full normalization.

Market & Trading Calls

- A full reopening of the Strait of Hormuz requires unconditional access. Current dynamics do not support this outcome.

- Iranian control is absolute, limiting upside for transit recovery despite reduced military activity in the Gulf.

- Under a long-term Iranian Control scenario, transits could rise to 40-50% of export capacity but normalization is not achievable.

- For crude this could be tolerated but other market face persistent supply pressure and price inflation.

Our previous reopening scenarios assumed Iran would become operationally ineffective or would step back to preserve is military capability and trade relationships, allowing a phased normalization. Two months into the conflict, this assumption is weakening. There is growing evidence that Iran may seek to retain strategic control of the Strait for as long as possible. At the same time, the US may tolerate this outcome. A reduction in Iranian attacks and the lifting of US naval pressure would allow flows to increase, easing crude prices and reducing political pressure on the US administration. However, at least for now, the White House continues to maintain a blockade with no timetable for removal.

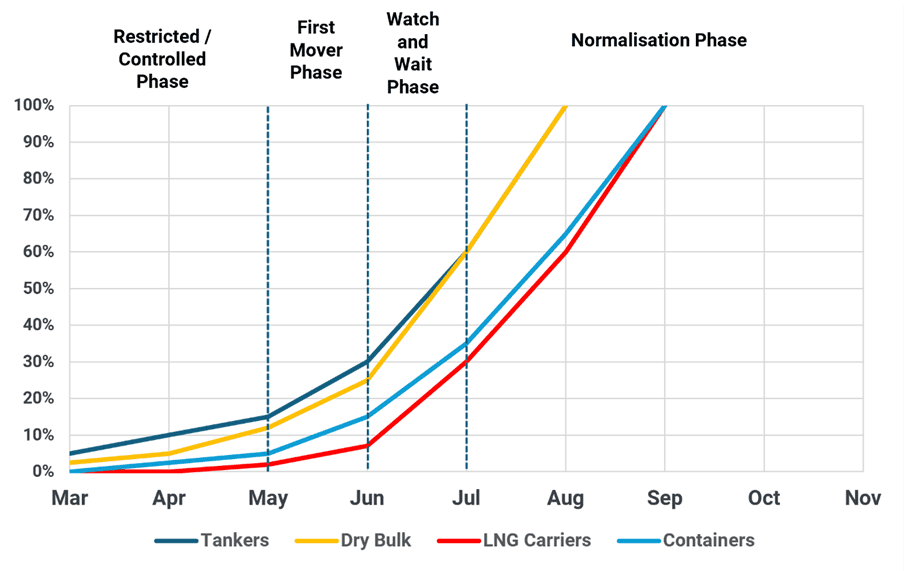

Phased return of Hormuz transits for tankers (% of MEG export capacity)

Source: Kpler

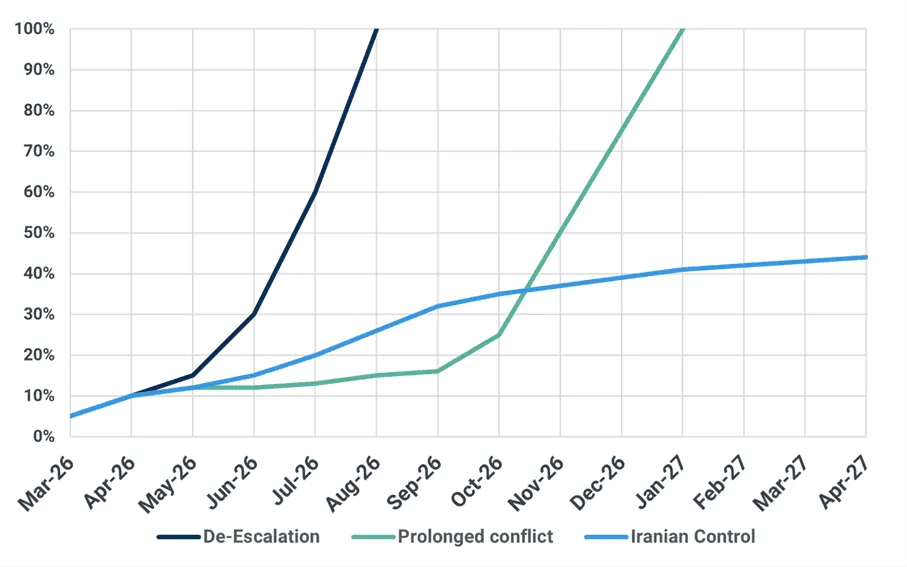

Our base case (De-escalation) assumed attacks would cease in April, enabling a phased recovery in flows by July. While not fully realized, conflict intensity has declined significantly. Iranian strike activity has reduced, and broader military engagement from the US and Israel has also eased.

Despite this, vessel transit data shows only a limited response. Transits increased from approximately 5% of pre-Iran transits in March to around 10% following the initial ceasefire. However, progress has stalled. Recent gunboat attacks and vessel seizures over the past two weeks have reinforced market caution. There remains a clear disconnect between reduced kinetic military activity and a meaningful recovery in commercial shipping flows. Ultimately, a broader peace deal between the US and Iran will be required to see our De-escalation scenario occur. De-escalation remains our most optimist scenario and is reflected in our balances.

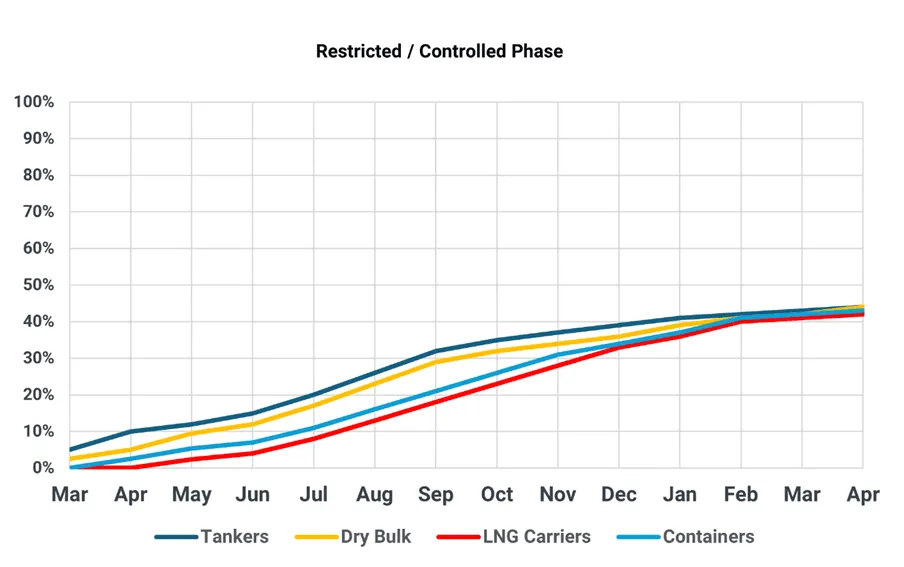

Operationally, the Strait remains under strict Iranian control. This aligns with Phase 1 of the reopening framework, defined as “Restricted/Controlled”. Under this regime, access is conditional, navigation is constrained, and risk premia remain elevated.

De-escalation: Phased return of Hormuz transits (% of MEG export capacity)

Iranian Control Scenario

If the status quo persists, or the United States simply walks away without an agreement with Iran, there will only be limited progress beyond the Restricted/Controlled Phase. Under this framework, transits may rise as owners become more comfortable with the concept of dealing with Iran, but full normalization is not achievable.

Iranian Control: Phased return of Hormuz transits (% of MEG export capacity)

A fully open Strait is incompatible with unilateral Iranian control with logistical and legal hurdles acting as barriers to full throughput. These include:

- Approval processes for transit clearance, which introduce delays and uncertainty

- Mandatory routing through Iranian waters, increasing insurance and compliance issues

- Potential toll payments to the IRGC, a US-designated entity

- More complex navigation relative to the established IMO traffic separation scheme

These constraints impose a hard ceiling on transit volumes. While flows will recover incrementally, capacity utilization will remain structurally capped.

We estimate that transits could reach a peak of approximately 40-50% of Middle East Gulf export capacity under this scenario. Beyond this level, operational friction and commercial risk will limit further gains.

Crude markets can partially absorb disruption due to alternative export routes such as Yanbu. However, other commodities lack this flexibility. As a result, partial reopening is sufficient to stabilize crude balances but will sustain inflationary pressure across refined products, LNG, and dry bulk markets.

The final scenario, Prolonged Conflict, assumes a return to a kinetic ‘hot war’ in which the US re-engages Iranian targets to take control of the Strait. Under this scenario, exports from the Mideast Gulf remain effectively shut-in for the majority of the year. Not only would the Strait remain effectively closed, but upstream production infrastructure would also take heavy damage from Iranian counter-attacks. For this reason, the Iranian Control scenario may be more appealing to the market over the short term. All effort should be taken to limit the length of the conflict, but it would be an error to assume Iranian control is the least worst option.

See why the most successful traders and shipping experts use Kpler