SPR & GoM grades drive on record US crude exports, but downside awaits

US crude exports set a fresh record in May, averaging 5.6 Mbd, but the composition of those barrels tells just as interesting a story as the headline figure itself.

Key Takeaways

- US crude exports hit a record 5.6 Mbd in May, aided by SPR and GoM grades

- Around one third of 58 Mbbls of SPR releases have been exported

- Cushing inventories approaching operationally low levels have tightened price spreads

- As a result, US crude exports in June are set to be closer to pre-conflict levels

- Total US crude inventories have fallen by 86 Mbbls since late March, with consistent draws set for June despite lower US crude exports

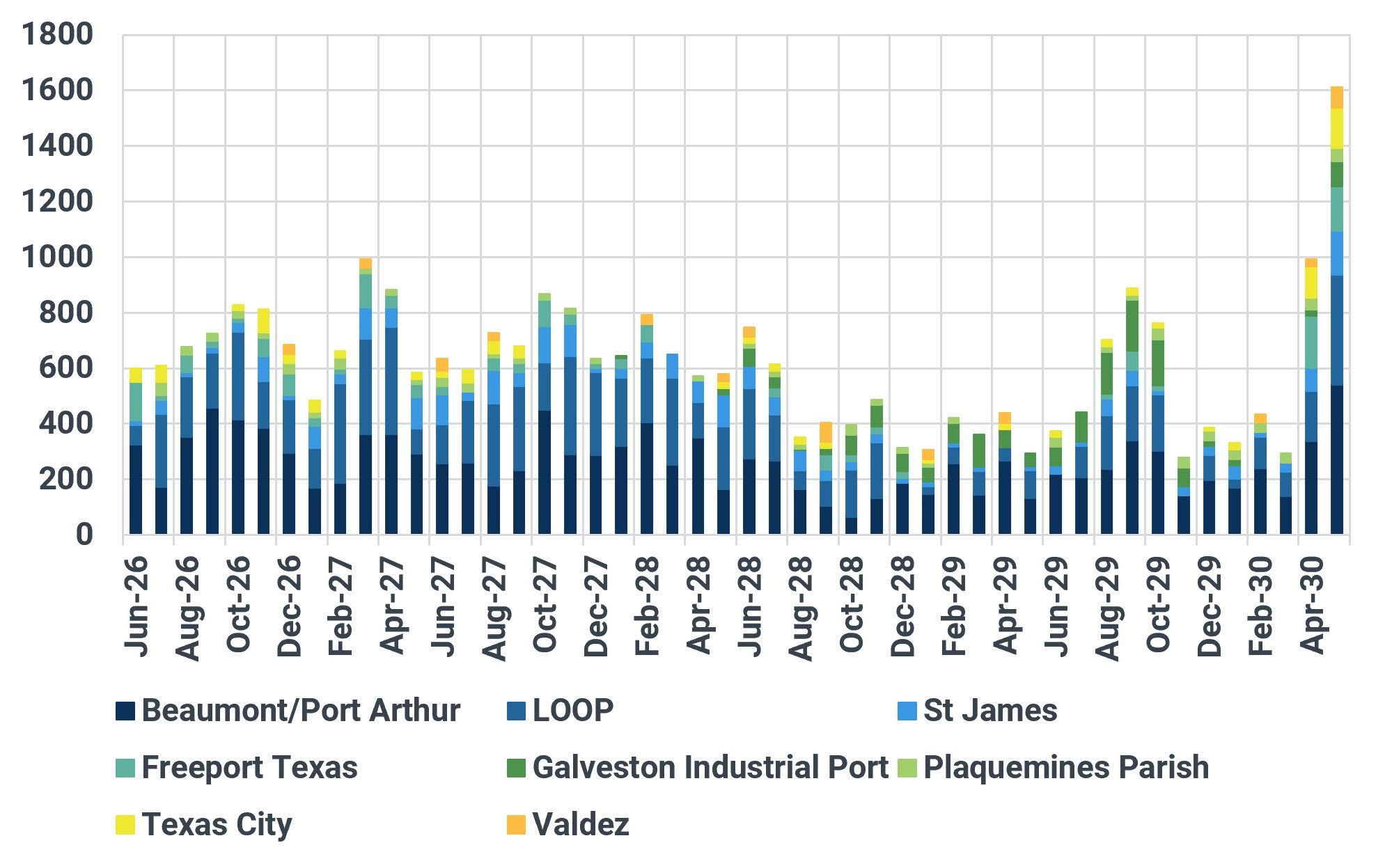

Historically, Corpus Christi and Houston dominate US crude exports, together accounting for roughly 85% of outbound volumes, largely consisting of light sweet shale barrels. In May, however, their combined share fell to just 70%, despite overall exports reaching all-time highs. This confirms what we have highlighted previously: Corpus Christi continues to face pipeline constraints, while Houston remains constrained by dock capacity.

The growth instead came from less prolific sources. Exports from US ports outside Corpus Christi and Houston surged to 1.6 Mbd during May, supported primarily by Strategic Petroleum Reserve (SPR) releases and elevated Gulf of Mexico (GoM) grade exports:

US crude exports: all ports ex Corpus Christi and Houston, kbd

Source: Kpler

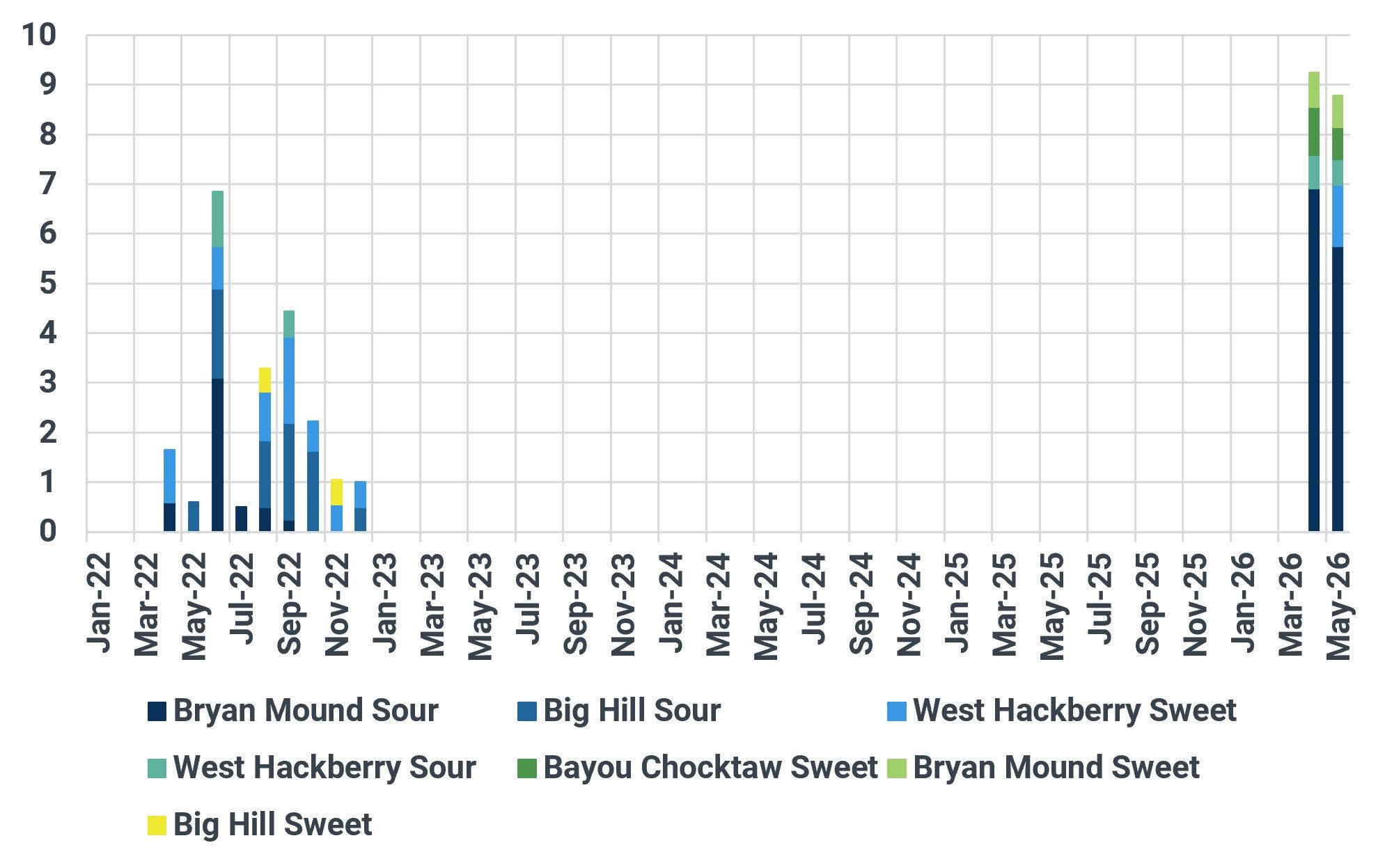

According to EIA data, approximately 58 Mbbls of crude have been released from the SPR since late March. Roughly one third of those barrels have been exported, with Europe emerging as the primary destination. The SPR barrels comprise five different grades sourced from multiple storage caverns, providing refiners with a broader slate of medium and sour crude grades, in contrast to what is available from US shale production.

At the same time, Gulf of Mexico exports have accelerated sharply. More than 28 Mbbls of GoM crude were exported during the last two months, approximately three times the normal pace. Unlike SPR barrels, these volumes have been distributed relatively evenly between Europe and Asia.

The relationship between these two flows appears significant. SPR barrels are being consumed by US Gulf Coast refiners, effectively displacing domestically produced offshore crude and freeing up those GoM barrels for export markets. This dynamic has boosted US exports to a record monthly pace. However, the sustainability of these export levels is increasingly questionable with SPR releases set to slow and inventories drawing.

US SPR crude exports by grade, Mbbls

Source: Kpler

Total US crude inventories have fallen by 86 Mbbls since late March, including a substantial 28 Mbbl draw over the last two weeks as refinery runs increase ahead of peak summer driving season. Inventory depletion is becoming particularly acute at Cushing, where stocks continue to trend toward historically low levels: our latest drone data for the week ending Friday 5 June indicates Cushing has drawn another 1.4 Mbbls this week – within a few million barrels of operationally low levels.

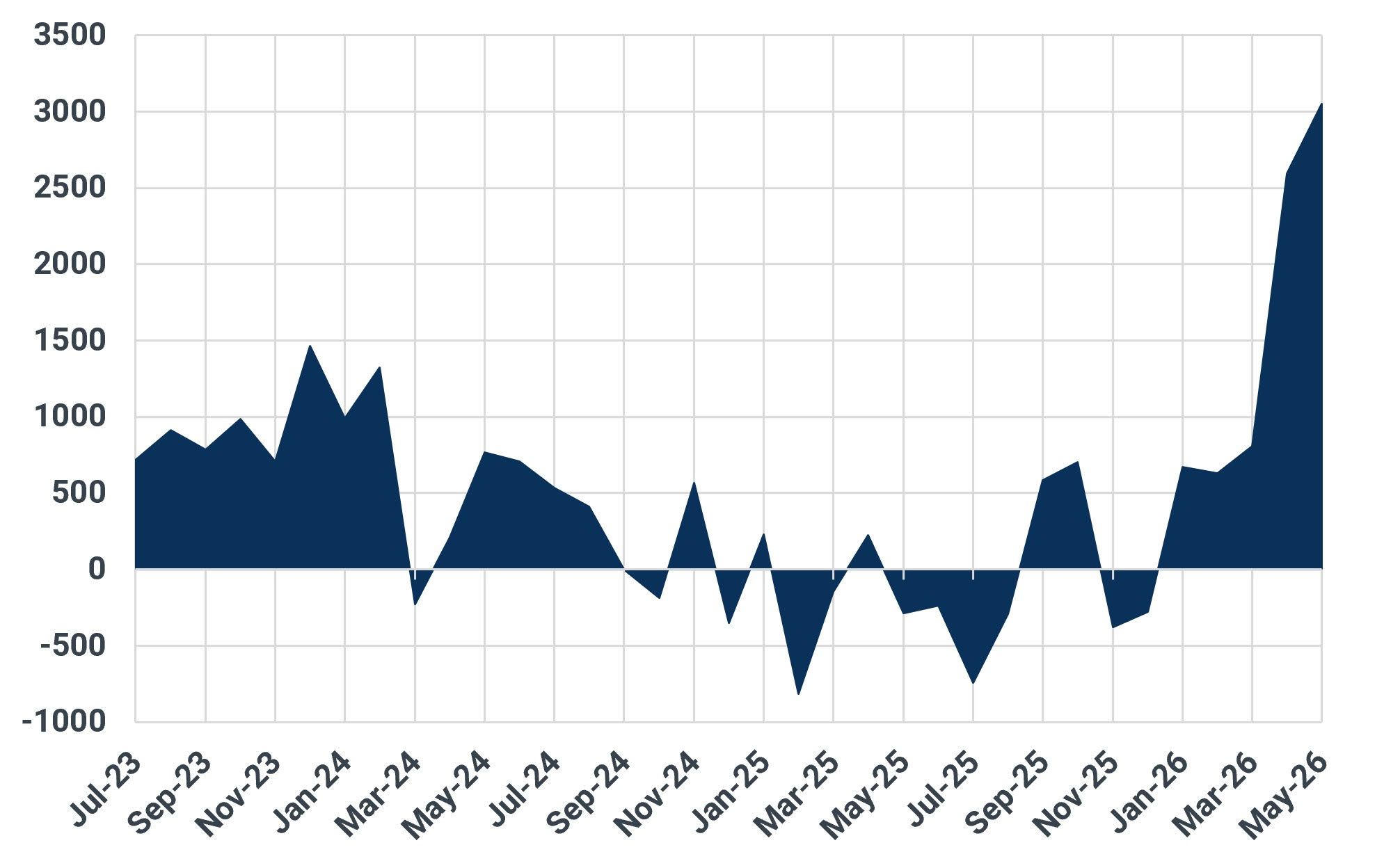

The strength of US hydrocarbon exports extends beyond crude. Compared with May 2025, crude exports last month were higher by 2 Mbd, while LPG and refined product exports were each up approximately 500 kbd. The combined impact is placing significant pressure on domestic inventory balances – although LPG inventories remain comparatively comfortable. Given the backdrop of draining inventories and Brent spreads tightening versus WTI benchmarks, our predictive indicator suggests the pace of US crude exports in June is going to be closer to pre-conflict levels, rather than the exceptional rates recorded over the last two months.

Y/Y change in US crude, clean product & LPG exports, kbd

Source: Kpler

See why the most successful traders and shipping experts use Kpler

.jpg)