Ample Australian wheat stocks water down El Niño threat

With El Niño conditions now present, the market will closely track weather across several key agricultural producers, such as Australia. Under El Niño, the south-east, a key wheat-producing region, typically experiences drier conditions. Australian wheat production is therefore likely to be lower y/y, but heavy ending stocks for 2025/26 will prevent a substantially weaker export campaign in 2026/27.

El Niño conditions are present

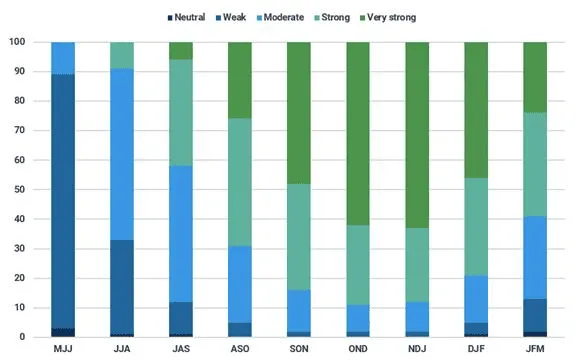

For its June update, the National Oceanic and Atmospheric Administration (NOAA) announced that El Niño conditions are present and are expected to strengthen towards the end of the calendar year. Though a stronger event does not always mean a more pronounced influence on weather, it does increase the likelihood. The emergence of El Niño conditions has been anticipated for several months and so comes as no surprise to the market, but the realisation will now focus the market on weather across several key agricultural producers.

Probability and strength of El Niño emergence (as of June, %)

Source: NOAA

Australia is a key agricultural producer where the impact of El Niño is regularly felt, although it is uneven across states.

Australian wheat production faces drought threat

Across south-east Australia, during August to December, El Niño conditions usually bring drier weather, through both lower rainfall and warmer temperatures. The south-west also sees warmer temperatures, but the impact on rainfall is not usually felt until January to February. Therefore, because harvest of the Australian wheat crop is usually underway by late October, the risk of drought is greater for the south-east crop than the south-west.

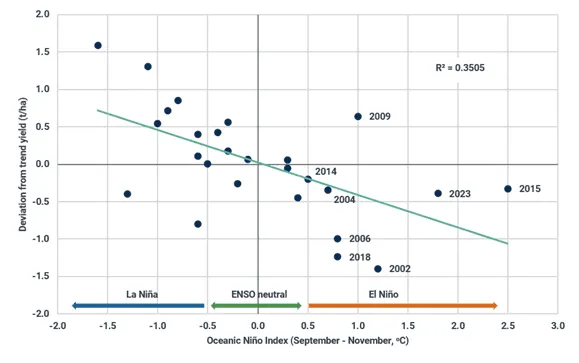

The statistical relationship between wheat yield and the Oceanic Niño Index (ONI) is weak and statistically insignificant for Western Australia but much stronger for South Australia, Victoria, and New South Wales.

Relationship between the Oceanic Niño Index (Niño 3.4) and wheat yield for SA, VIC, and NSW

Source: NOAA, ABARES

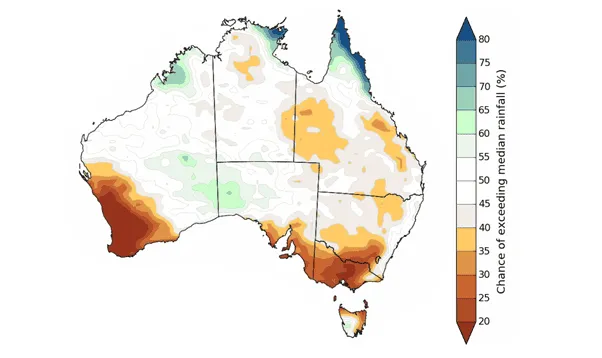

Given the threat of dry conditions during grain-fill later this year, rainfall in the preceding months may help boost soil moisture reserves, acting as a buffer. Currently, soil moisture reserves are favourable across much of the south-east, with reports of waterlogged fields in some parts. However, a recent three-month outlook for below-average rainfall in parts may limit the opportunity for reserves to remain well supplied. Consequently, crops may face El Niño conditions in a more vulnerable position.

Rainfall outlook for July-September (as of 15 June)

Source: Bureau of Meteorology Australia

As production in the south-east comes under concern, output from outside the south-eastern states plays an influential role in the total supply of Australian wheat. In recent years, 40% of total wheat production has come from outside South Australia, Victoria, and New South Wales, most of which is from Western Australia. So similarly unfavourable growing conditions or a smaller planted area elsewhere could compound the national production challenge.

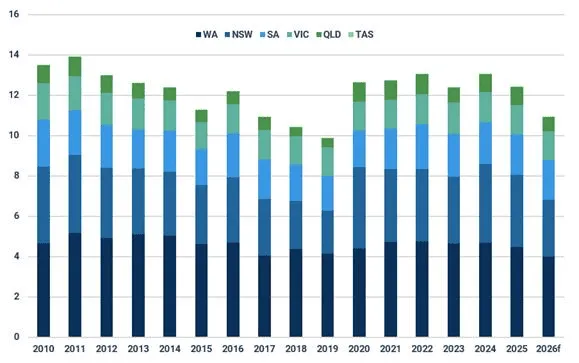

The latest forecasts from the Australian Bureau of Agricultural and Resource Economics and Sciences (ABARES) suggest the wheat area for 2026/27 will decline by 12% y/y. This was in response to less attractive margins than alternative crops such as barley. Most states are expected to see the wheat area decline y/y, with only South Australia remaining unchanged.

Wheat area declining across most Australian states in 2026 (Mha)

Source: ABARES

On balance, the outlook for Australian wheat production is not optimistic. Given the negative correlation between the September-November ONI and wheat production in the south-east, the strength of the El Niño event later this year will greatly influence national production.

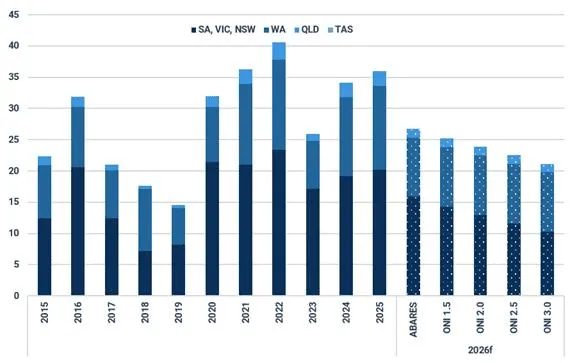

Wheat production scenarios versus El Niño strength (mt)

Source: ABARES, NOAA, Kpler Insight

Heavy stocks cushion supply situation for 2026/27

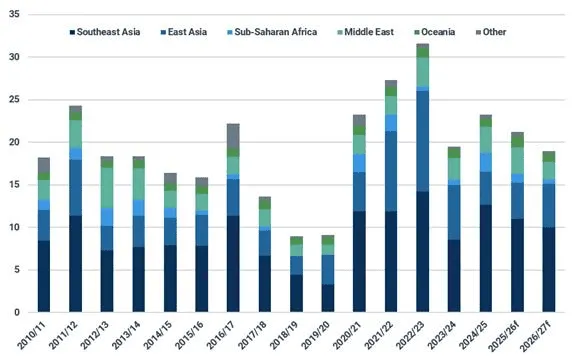

Exports for the rest of 2025/26 marketing year (until September) are likely to soften due to Northern Hemisphere competition. As a result, Australia is expected to carry ample stocks into 2026/27. Its export campaign is unlikely to drop to lows seen before following an El Niño event, such as 9 mt for 2018/19. Instead, the scenario appears more closely aligned with 2023/24, when a strong El Niño event occurred, but record production the year before alleviated supply pressure.

Australian wheat exports will retain a relatively strong global presence, but not at levels that significantly displace rival Northern Hemisphere exporters.

High ending stocks cushion 2026/27 exports (mt)

Source: Kpler Insight

See why the most successful traders and shipping experts use Kpler