Chinese economy enjoys a healthy energy supply buffer

China's oil inventory cushion and refined product export ban insulate the domestic market from the Hormuz closure. However, China's core growth model remains imbalanced.

Summary

- Healthy Energy Supply: Ahead of the Iran conflict, China was better positioned than most major energy importers. Onshore oil inventories stood at roughly 1.2bn barrels, providing 113 days of seaborne import cover, rising to 250 days when measured against domestic transportation fuels alone.

- Export Ban: A ban on refined product exports enacted on March 12 further insulates the domestic market, but at the cost of widening supply shortages across the broader Asia-Pacific region. Seaborne clean product exports have collapsed from 640 kbd to just 90 kbd since the bank took effect. Refinery output will fall more than 1 Mbd y/y in April, albeit domestic fuel demand will remain largely stable.

- The 4.5% Growth Target: We expect China to grow at 4.5% this year, at the low end of the growth target range. The mode of growth continues to exacerbate longstanding imbalances. The government leaned heavily on infrastructure investment in Q1, with expenditures up 8.9% y/y, while manufacturing investment also recovered to 4.1% y/y. We have revised headline inflation up 40bp to 1.2% on Iran energy price concerns, though weak underlying consumption limits broader price pressures.

- Consumer Disappointment: our calculation of Chinese inflation-adjusted retail sales growth managed just 1.4% y/y in Q1, well below industrial production growth of 6%, the latter of which reaccelerated from Q4 2025. Until household demand begins to show signs of outpacing production expansion, China’s structural reliance on external demand and investment to drive growth will persist.

Market Analysis

China has plenty of headroom to absorb a longer-run energy supply shock, but it comes at expense of the rest of East Asia.

Over the past six weeks, our regular cadence of country and region level economic updates has been disrupted by the Iran war. As the threat of an extended Strait of Hormuz closure reshapes the outlook for global growth and inflation, much of our focus has centered on scenario analysis given the unknowns around the conflict between the United States and Tehran. It is our view that the duration in which the Strait of Hormuz remains closed is the ultimate determinant of how bad things get across the global economy. In this week’s macro update, we check in on the state of the Chinese economy and provide our forecasted outlook for growth and inflation as the war in Iran continues.

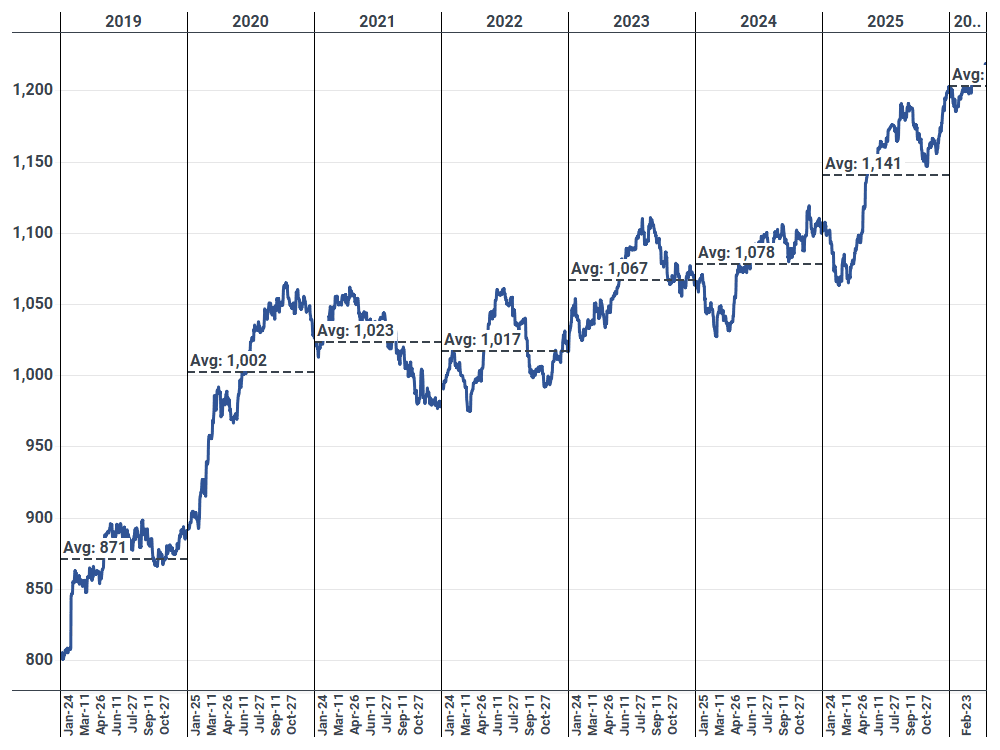

Domestic Chinese Onshore Oil Inventories (Mb)

Source: Kpler

Coming into the Iran conflict, China was better off than most other major energy importing nations. Chinese onshore oil inventories on February 28 were roughly 1.2bn barrels, equating to 113 days of seaborne oil import cover. Our days cover calculation rises to an impressive 250 days when accounting solely for Chinese domestic transportation fuels demand (~9.3 Mbd). Of the major East-Asian economies, only Japan is in a similarly advantageous supply position.

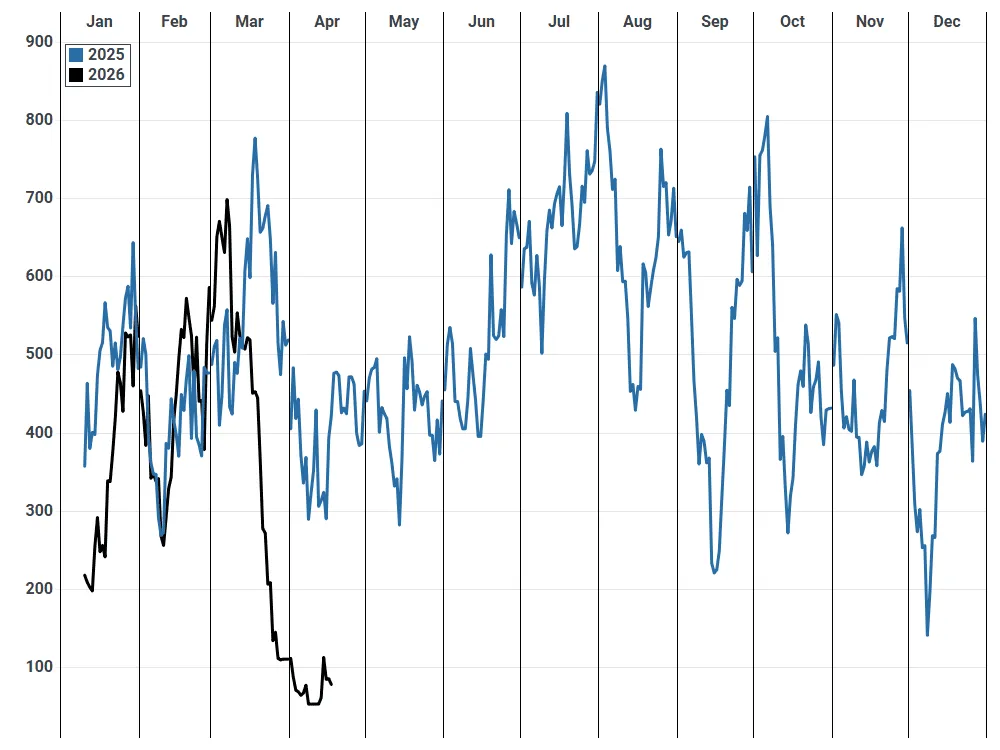

On March 12, a bit over a week after the US began combat operations in Iran, the Chinese government took action to restrict refined product exports. This was a major move. In 2025, combined gasoil/diesel, gasoline, and jet exports leaving China finished at 640 kbd. The move to restrict exports was unsurprising – the Chinese government tends to emphasize energy supply security when making policy decisions. On a 15-day moving average, Chinese seaborne exports of gasoline/naphtha, gasoil/diesel, and jet/kero have fallen to just 90 kbd, down from 640 kbd in the days before the export ban. The Chinese government has only allowed a few shipments to Australia, the Philippines, Singapore, Malaysia, and Japan, among a few others since the ban went into effect.

Daily Chinese Seaborne Core Clean Product Exports (kbd, 10-day ma)

Source: Kpler; volumes exclude shipments to Hong Kong

The export ban is having a big impact on domestic refinery runs, an unsurprising outcome as China’s refinery capacity far outpaces consumption. We currently expect Chinese throughput to finish at just 14.17 Mbd in April, down from 15.7 Mbd in February, and lower 1.1 Mbd against year earlier levels. However, domestic demand is only expected to decline slightly for reasons unrelated to the Iran war. This dichotomy effectively limits adverse supply and price impacts within China, while widening supply shortages throughout the broader Asia-Pacific region.

China’s growth model remains highly imbalanced as the government presses for infrastructure investment in Q1.

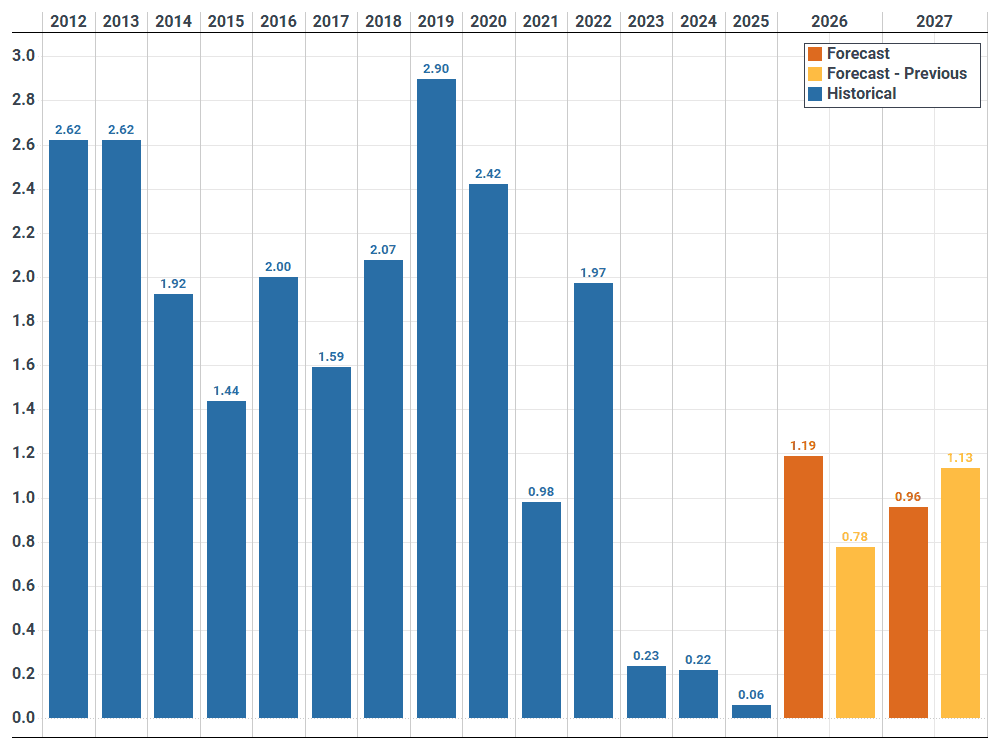

Ample Chinese oil inventories, and a ban on exports limits the pressure on the Chinese economy. Our forecast, which assumes the Strait of Hormuz begins reopening in early- to mid-May implies that China will hit the low end of its growth target (4.5%), as laid out by the government in early-March. Remember, Chinese GDP targets are not a suggestion, but a policy tool that require adherence. Ultimately, local and municipal governments will deploy a lot of uneconomic investment if that’s what is required to meet said target. We have revised up our expectation for Chinese headline inflation to 1.2% this year (+40bp), albeit this is less of a problem than in other major economies given underlying economic weakness in consumption, which limits broader inflationary pressures.

Yearly Chinese Headline Inflation with Forecast (%)

Source: Kpler, various international organizations

Our core thesis on the Chinese economy remains unchanged from the past several years. China remains too reliant on manufacturing and infrastructure investment, net exports, and inventory stocking to meet overly aggressive growth targets. Chinese industrial policy effectively limits wage appreciation relative to productivity growth, and a limited social safety net acts to keep the national savings rate at levels that are far too elevated. Corporate income taxes are also too low, limiting redistribution to households. These policies limit the much needed shift to a consumption-based economy that relies less on importing demand from abroad.

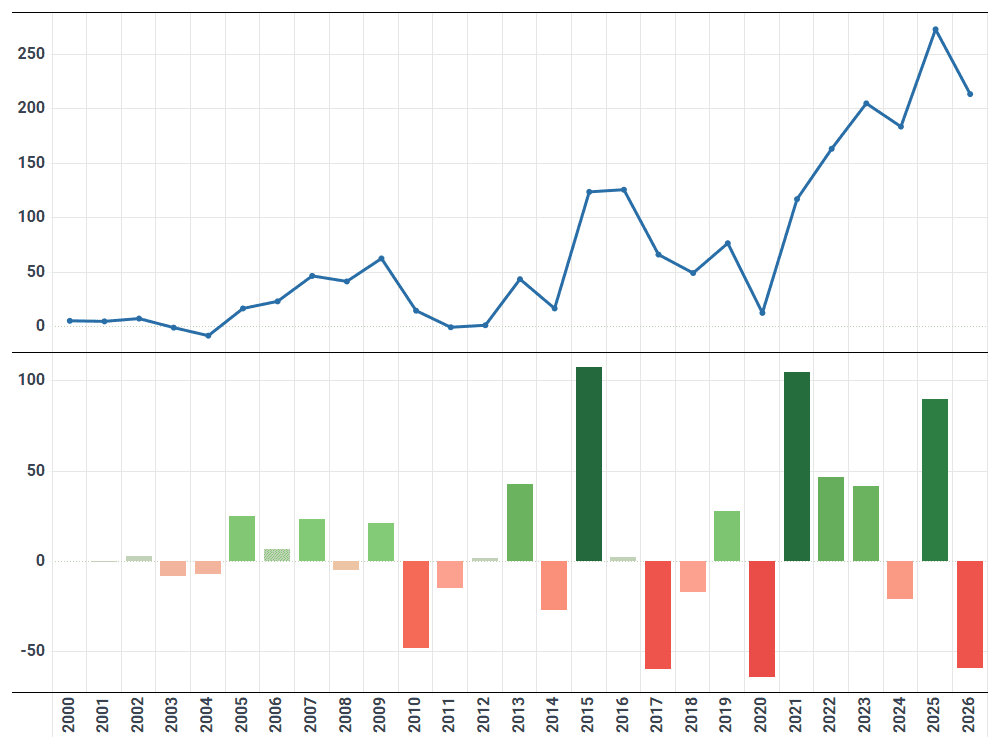

In 2025, China leaned heavily on external demand to prop up growth at home, reflecting wide imbalances within the economy. Net exports of goods surged to a new record high $1.19tn, marking a gain of $201bn against levels a year earlier, with nearly all of this gain a result of rising exports alongside a slight decline in imports. A rising trade surplus was the result of excessive overcapacity, and weak consumption at home, particularly through the second half of the year. By our calculations, inflation-adjusted consumer spending growth was outpaced by industrial production growth by a sizeable 3.1pp. Such a reliance on exports speaks to the reasons China is anticipating talks with the White House in May. America is by far the largest absorber of surpluses from abroad.

Q1 Chinese Goods Net Exports (USD bn, top) and Y/Y Delta (USD bn, bottom)

Source: GACC

The imbalances have continued into Q1 of 2026. While net exports narrowed in Q1 to $214bn, down from $273bn in Q1 2025, and $316bn in Q4 2025, the government leaned heavily on infrastructure investment as an offset with expenditures up 8.9% y/y through the first three months of the year. We expect infrastructure growth will remain at or above current levels through at least Q2. Manufacturing related investment growth also recovered to 4.1% y/y in Q1 after steadily declining through H2 2025. The uptick in manufacturing fixed investment will likely provide plenty of upside for more net export growth later this year, albeit we are not convinced the pace of increase across manufacturing outlays will be able to maintain for long given involution efforts, and an already overbuilt manufacturing sector.

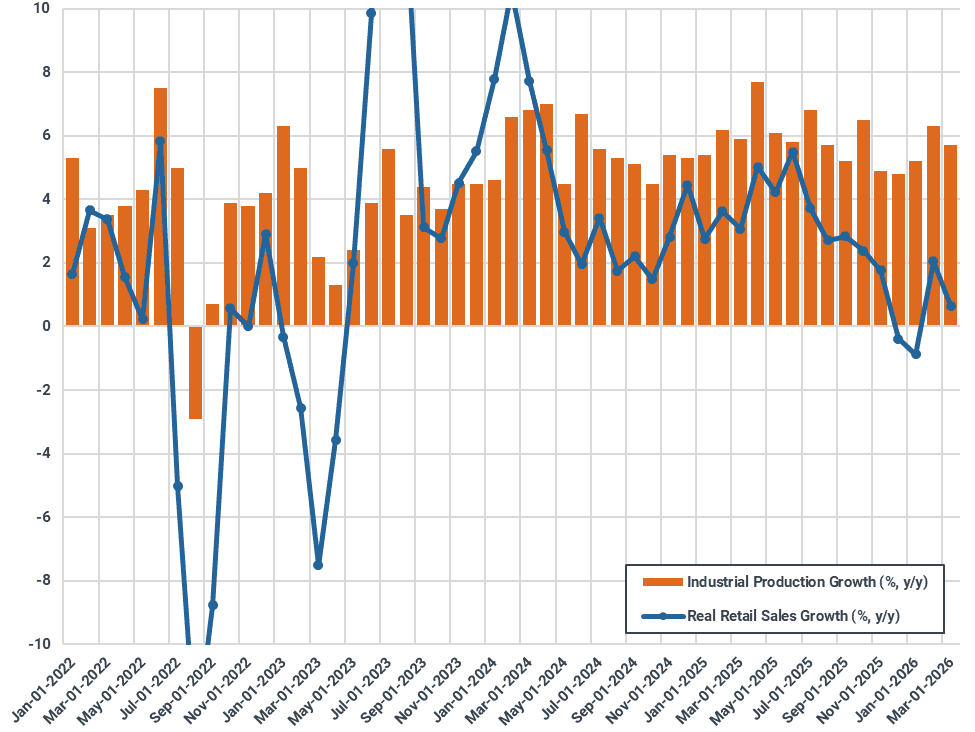

The Chinese consumer remains disappointing, a trend that was clearly true through H2 of last year. After dropping into negative territory in November and December, real goods retail sales growth, calculated with the help of government reported headline inflation figures, managed to climb back into the green through Q1 (+1.4% y/y). However, this still paced well below industrial production growth of 6%, the latter of which was a notable pickup from Q4 2025. This will have to translate into continued export growth, and inventory stocking.

As has been true for several years, China remains heavily reliant on investment and external demand to support aggressive growth targets. For now, there is little evidence of a shift towards a consumption-based model of growth.

Monthly Chinese Inflation-Adjusted Retail Sales and Industrial Production Growth (%, y/y basis)

Source: NBS, Kpler calculations; data for February are an average of the first two months of the year; real retail sales calculated by using headline consumer inflation

See why the most successful traders and shipping experts use Kpler