US export controls scenario: How would the market react?

US export controls could offer temporary domestic price relief, but would likely fracture global crude and product markets just as constrained Hormuz flows make US barrels most critical. A product ban would hit Latin America first and tighten Atlantic Basin distillates, while a crude ban could violently widen WTI-Brent as Midland barrels back up and Brent-linked replacement grades reprice higher. The core risk is that Washington softens visible Gulf Coast pressure while worsening global scarcity, freight dislocations and refinery run-cut risks.

Why would the US consider export controls?

The oil market has become increasingly fragile. Total oil on water, excluding the Mideast Gulf, has fallen by roughly 250mmbbls since the start of the conflict, while onshore inventories excluding China continue drawing. The longer Hormuz remains constrained, the more dependent the global market becomes on the US to keep oil flows balanced.

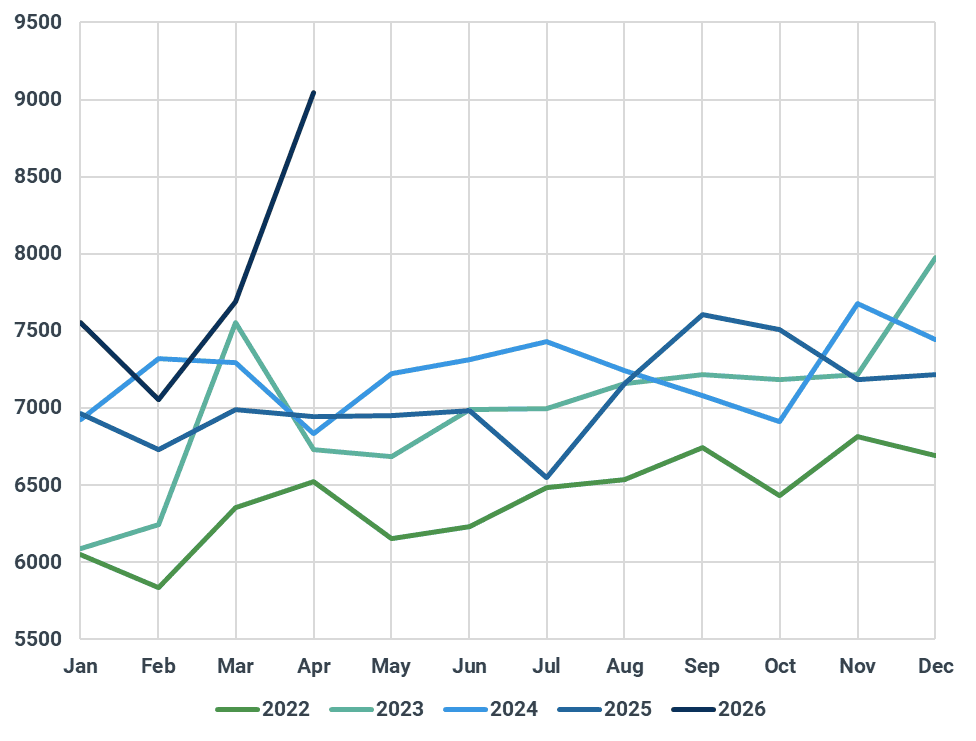

The USGC is now balancing both Atlantic Basin and Asian deficits at the same time, while SPR barrels and inventory drawdowns are helping smooth the immediate shock. Total US liquids exports reached record highs of over 9mbd in April, sharply above the 3-month average of around 7mbd before the start of the US/Israel-Iran conflict.

The problem for Washington is that those same exports, particularly refined products, are tightening domestic supply and increasingly feeding into higher gasoline prices. US consumers have so far absorbed higher prices without a major policy response, but if national pump prices continue moving towards $5/gal, the political pressure changes materially. At that level, gasoline becomes a highly visible inflation signal, weighs more directly on household budgets, and starts to pressure the administration’s economic approval.

That leaves the White House facing the same question that surfaced in 2022: should exports be restricted to protect domestic consumers? Publicly, officials deny it. But the market is already beginning to price the risk. A low-probability but increasingly priceable scenario is now emerging: what happens if the US imposes restrictions on crude and/or refined product exports to shield domestic consumers from rising fuel prices? More importantly, how would global flows, arbitrage relationships and refinery economics respond once the world’s key swing supplier starts restricting exports?

Combined US Seaborne Exports of Crude and Petroleum Products (kbd, monthly)

Source : Kpler

Crude, Products, or both?

So why would the US restrict both crude and products? Gasoline prices are what voters see every day, so refined product exports are the obvious first target. A product-only restriction appears to make sense: stop gasoline, diesel and jet fuel leaving the Gulf Coast, trap more product barrels domestically and pressure consumer prices lower.

The case for a product-only ban is that it targets the molecules consumers actually buy. It could push Gulf Coast gasoline cracks lower, build local inventories and deliver some near-term relief in regions directly connected to Gulf Coast supply. But the US fuel system is not one unified market.

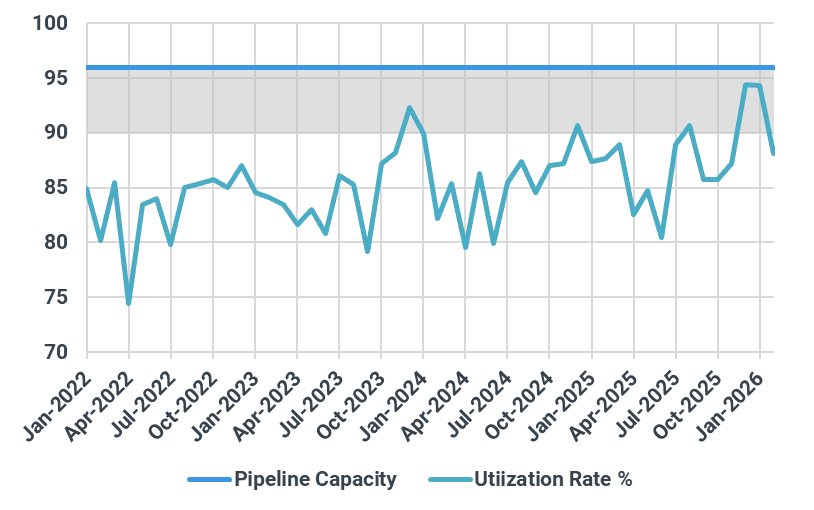

A product-only ban would weaken Gulf Coast prices as export barrels back up into storage, but PADD 1 would remain tied to international replacement costs. Colonial Pipeline is already near practical capacity, Jones Act shipping is expensive and limited, and Eastern Canadian refiners retain a freight advantage into the Northeast. So the East Coast may still face elevated gasoline, heating oil and diesel prices even as Gulf Coast inventories build.

PADD 1 to 3 Total Products Pipeline Utilization (%)

Source : EIA

The bigger risk is refinery utilization. If Gulf Coast refiners lose the export outlet that clears surplus production, product inventories rise, cracks compress and margins can move toward uneconomic levels. At that point, refiners cut runs. That matters because run cuts do not only reduce gasoline; they also reduce diesel, jet fuel and heating oil supply. So a product-only ban can create an awkward split: surplus gasoline trapped in the Gulf Coast, but tighter middle distillate balances across PADD 1, Europe and Latin America.

That is the argument for going further and restricting both crude and products. A combined restriction would try to protect refinery economics by cheapening domestic crude feedstock while also keeping refined products at home. In theory, that lowers refinery input costs, supports runs and limits product export leakage. But it also carries much larger risks.

The US refining system was not designed as a closed domestic loop. Gulf Coast refiners still need heavier imported crude to optimize yields, while domestic shale production is dominated by lighter barrels. Restricting both crude and products risks trapping too much light crude and too many finished products in the wrong region, while PADD 1 and other import-dependent markets remain tight.

So the conclusion is this: a product-only ban is politically cleaner but risks crushing Gulf Coast margins and forcing run cuts, while a combined crude and product ban is more coherent on paper but far more disruptive in practice.

On Products : Who suffers the most, and at what cost?

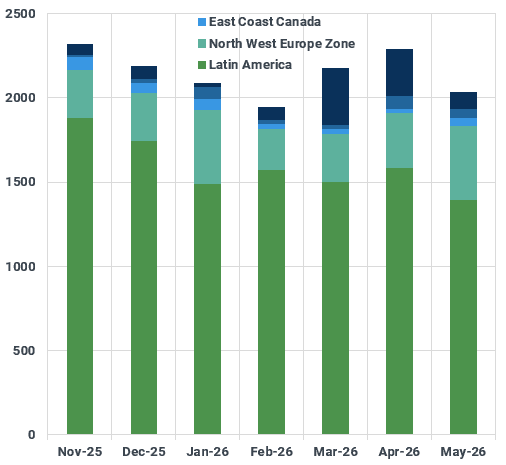

On products, Latin America is hit first and hardest. Mexico, Brazil, Chile and Central American markets rely heavily on US Gulf Coast gasoline and diesel because it is the shortest and cheapest supply route. If those exports are restricted, replacement products need to come from Europe, India or further east at materially higher freight costs and longer voyage times.

Europe becomes the next pressure point, especially in diesel. The region has already been balancing the loss of about 450 kbd of middle distillates through higher imports from the US, India and limited Middle Eastern barrels loading outside the Strait of Hormuz. Remove US exports and Europe is forced to compete much more aggressively for an already constrained pool of Atlantic Basin distillates.

Asia feels the gasoline impact less immediately, but still tightens through distillates and crude substitution. As Europe and Latin America bid for replacement products, Asian buyers face stronger competition for diesel, jet and non-Middle Eastern crude while Hormuz flows remain constrained. The disruption would not stay confined to pricing for long. Ships already underway would need rerouting, freight markets would tighten sharply, and buyers would start securing replacement supply ahead of actual shortages. Trade routes can reprice in hours, but physical flows take weeks to adjust.

The market response :

- European diesel cracks rally sharply.

- Gulf Coast gasoline cracks weaken materially.

- NYH heating oil and transatlantic distillate spreads strengthen.

US Product Exports by Destination Region

Source: Kpler

On Crude : What happens to spreads?

An export control would not happen instantly. There would likely be extensive consultations with industry participants and stakeholders, and that is where the speculation and price move would begin: before any official announcement.

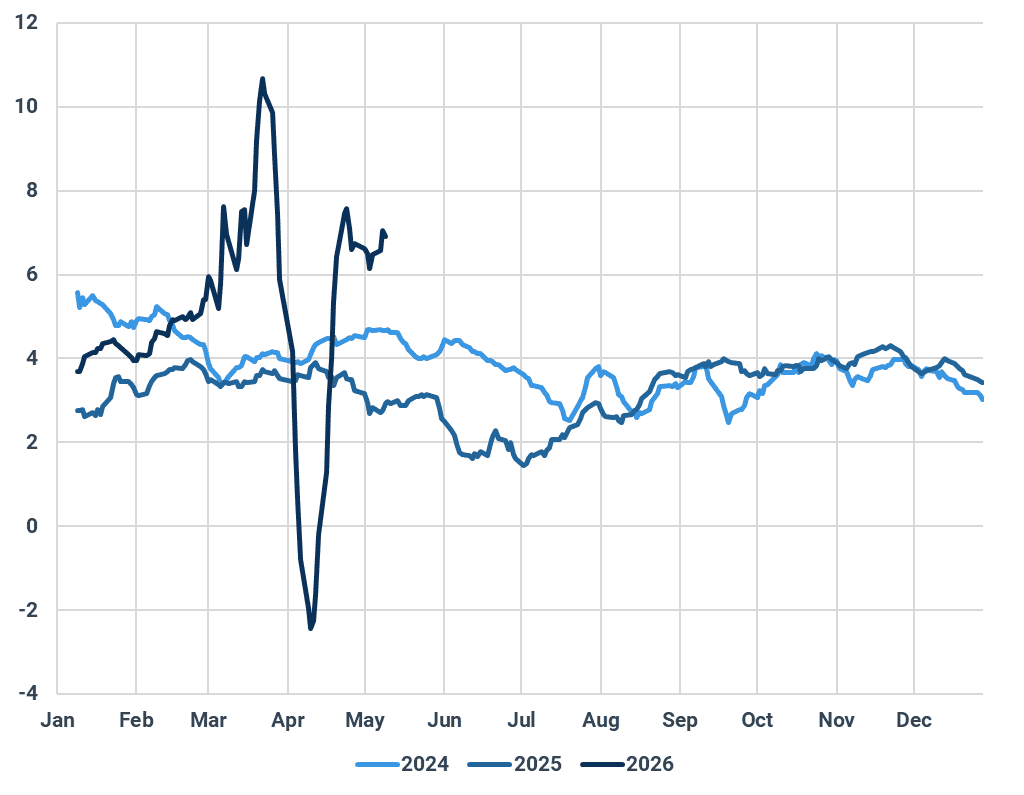

The market would start discounting the expectation of reduced Midland availability into the waterborne market, while pricing greater scarcity around Brent-linked barrels. The first expression of that risk would likely be a sharp widening in WTI-Brent. Diamondback’s Q1 results showed the company had bought WTI-Brent basis puts for Q2 and Q3 2026 struck around -$42/bbl. That does not mean the market is pricing an export ban today, but it does show producers are willing to hedge the tail risk of export disruption, and that WTI-Brent is the cleanest place to express that risk.

Under normal conditions, a wider WTI-Brent spread would pull more Midland into Europe and Asia. This time, the spread would be sending the opposite signal. WTI would be cheap because barrels are trapped, not because the export arb is improving. The arb signal would therefore break: the spread would say “export more,” but policy would prevent the barrels from moving.

In March, WTI-Brent widened sharply in a single session, moving toward -$10/bbl on the back of the US/Israel-Iran conflict, versus a more typical -$2 to -$5/bbl range. This setup would be more extreme because US exports are now larger, and global dependence on those exports is higher. In our view, a crude export-control scenario could push WTI-Brent into a much wider stress range, potentially toward -$15 to -$20/bbl if storage fills, USGC congestion builds and Brent-linked scarcity intensifies. The -$40/bbl level should be treated as a tail-risk hedge rather than the base case, but it shows how violent the repricing could become if the export outlet is impaired.

WTI-Brent Spread vs Export Ban Risk

How do Crude Trade Routes Start Rewiring?

The whole crude map changes. European and Asian refiners would be forced to compete more aggressively for non-US Atlantic Basin barrels as Midland availability declines and Middle Eastern supply remains constrained. WAF, North Sea, Brazil, Guyana, CPC and other replacement grades would all need to clear at stronger premiums as refiners prioritize security of supply over normal landed-cost economics.

Similar to the Hormuz disruption, refiners would likely keep lifting barrels even when arbs look closed or margins look poor. The issue is not whether the arb screens well. The issue is whether the refinery can secure crude at all.

That is where margins become vulnerable. Replacement crude costs could rise faster than product cracks, especially in Europe, where refiners are already exposed to high landed crude costs and weaker flexibility. If crude premiums stay elevated, some refiners would eventually cut runs toward minimum sustainable levels rather than chase uneconomic barrels.

That creates a feedback loop back into products. Lower refinery runs would tighten diesel, jet and gasoline balances further, especially across import-dependent regions. So even as the market finds replacement crude, product availability can still deteriorate.

Key arb relationships would move sharply:

- WTI-Brent widens violently on Brent-linked scarcity.

- Atlantic Basin replacement crude premiums strengthen as Europe and Asia compete for the same barrels.

- Dirty freight strengthens on longer replacement voyages and tighter vessel availability.

Light Sweet replacement crude costs into NWE

Source : Kpler

The Irony

The longer Hormuz remains constrained, the more politically attractive export controls become for Washington. But that is exactly when the global market needs US barrels most.

The US cannot fully replace the barrels lost through Hormuz. It can only slow the adjustment by exporting more crude, exporting more products and drawing down inventories. Product controls would weaken Gulf Coast prices locally, but remove the relief valve for Latin America, Europe and parts of Asia. Crude controls would go one step further, trapping light shale domestically while forcing the rest of the world to bid harder for non-US replacement barrels.

So the policy may soften visible Gulf Coast pressure while making global scarcity worse. That is the contradiction underneath the market today: the more important the US becomes as the swing supplier, the more damaging it becomes if Washington restricts that role.

The key political question is therefore simple: if gasoline prices keep rising, does Washington prioritize the US voter or the global market it is currently helping to balance?

See why the most successful traders and shipping experts use Kpler