A violent stalemate to prevail

Until Israel disrupted diplomatic talks, the U.S. and Iran were in a tense stalemate that, while dangerous, had largely avoided direct U.S.-Iran military confrontation. Escalation increased in early June, culminating on June 8 when a U.S. Apache helicopter crashed near the Strait of Hormuz. The Trump administration subsequently blamed Iran for the incident, triggering U.S. retaliatory strikes and a new round of direct U.S.-Iran conflict.

While there are reports that the United States and Iran remain close to a negotiated settlement, the two sides still appear far apart on their core objectives. Iran is seeking meaningful sanctions relief, access to its blocked finances, preservation of the regime, and the ability to maintain leverage over shipping through the Strait of Hormuz, its most important strategic waterway. But Iran is also seeking to end the war under its own terms and, in the process, a humiliation of Trump. The United States, meanwhile, is demanding significant concessions on Iran's nuclear program, guarantees for maritime security, and limits on Tehran's regional influence.

Perhaps in Iran’s calculus the longer the conflict is dragged out, the better negotiating position they are in, while, on the other hand, Trump appears to be in more of a rush to reach a deal, and his bursts of frustration with the Iranian officials translate into more targeted military interventions.

In the meantime, the US is maintaining military and economic pressure in the hope that it forces Iran to agree to all their conditions. Counterbalancing the pressure, Tehran continues to use Hormuz as its biggest leverage, knowing very well that the United States and the broader global economy have limited tolerance for prolonged disruptions to energy flows through the Gulf, particularly given the potential loss of up to 15 million barrels per day of oil exports and transit volumes.

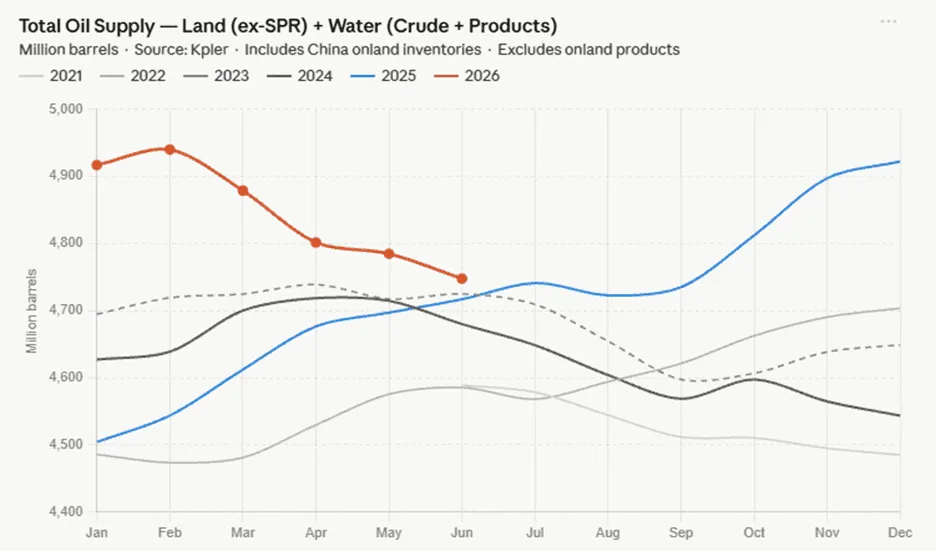

Kpler data suggests that the oil market is currently absorbing the disruption through inventory drawdowns in addition to a level of demand erosion. According to Kpler's satellite-based monitoring, global crude oil inventories on land (excluding the U.S. Strategic Petroleum Reserve) and crude and refined products stored on water are declining at approximately 2 million barrels per day. These figures include China's visible crude inventories but exclude global onshore refined product inventories, indicating that the market is relying on stored barrels to offset supply constraints.

Another important buffer has been the coordinated release of crude from global strategic petroleum reserves. The current program totals roughly 400 million barrels, of which 172 million barrels are scheduled to come from the U.S. Strategic Petroleum Reserve. U.S. SPR releases began in April, and approximately 70 million barrels have been delivered to the market so far. According to EIA data for the week ending June 5, SPR releases are currently contributing more than 1 million barrels per day of supply into the market, helping offset the loss of Gulf exports and moderating price pressures.

The inventory drawdowns, SPR releases, and the resilience of global oil markets suggest that Washington does not yet feel compelled to compromise, while Iran's continued willingness to threaten energy flows and absorb economic pressure indicates that Tehran also believes it retains meaningful leverage and can improve its position through continued confrontation. In other words, neither side has yet reached a mutually hurting stalemate—the point at which the costs of continuing the confrontation clearly outweigh the benefits of holding out for a better outcome. To a large degree, many in the market have underestimated the extent to which oil markets could adapt to supply shocks; however, this still does not take away from the gravity of supply shocks, which will be even more pronounced if the Strait remains restricted.

As a result, the most likely near-term outcome is continued managed escalation rather than compromise leading to a peace deal. The probability of an all-out regional war is less likely (given that Gulf states in the region want to avoid a return to that), although the scenario must be included given how fragile the situation is, and that means any miscalculation of either side could easily break the containment.

So for now we just witness more of the same, or what we call a violent stalemate, where neither side is prepared to make the concessions necessary for a durable agreement, yet neither believes the costs of continued confrontation are high enough to justify compromise. Until one side concludes that further pressure is unlikely to improve its position—or that the costs of escalation have become intolerable—both parties are likely to continue testing each other's resolve through military, economic, and diplomatic means. In that sense, the current confrontation appears less like a march toward a final settlement and more like a contest over who reaches its pain threshold first.

See why the most successful traders and shipping experts use Kpler