America’s siren song: Supplier of last resort

The piece argues that the United States has become the world’s “supplier of last resort” after the closure of the Strait of Hormuz, with global markets increasingly relying on American crude and refined product exports to stabilize supply shortages. It warns that as U.S. inventories tighten and gasoline prices climb toward politically sensitive levels, pressure for export controls could grow — but cutting exports after allies and markets have reorganized around U.S. supply risks triggering even greater global shortages and price shocks.

“All of those countries that can’t get jet fuel because of the Strait of Hormuz… I have a suggestion for you: Number 1, buy from the U.S., we have plenty…”

— President Donald J. Trump, March 31, 2026

The Siren’s Song

It has been 67 days since the United States and Israel launched their war on Iran, and 67 days since the Strait of Hormuz was effectively shut. As the world grows increasingly anxious about fuel shortages, the President has called on nations to buy from the United States.

And while the United States is an energy powerhouse — if you did not know that before the war, you certainly know it now — it cannot fully replace the energy flows lost through the Strait of Hormuz. And it certainly cannot attempt to do so without imposing enormous costs on the American consumer.

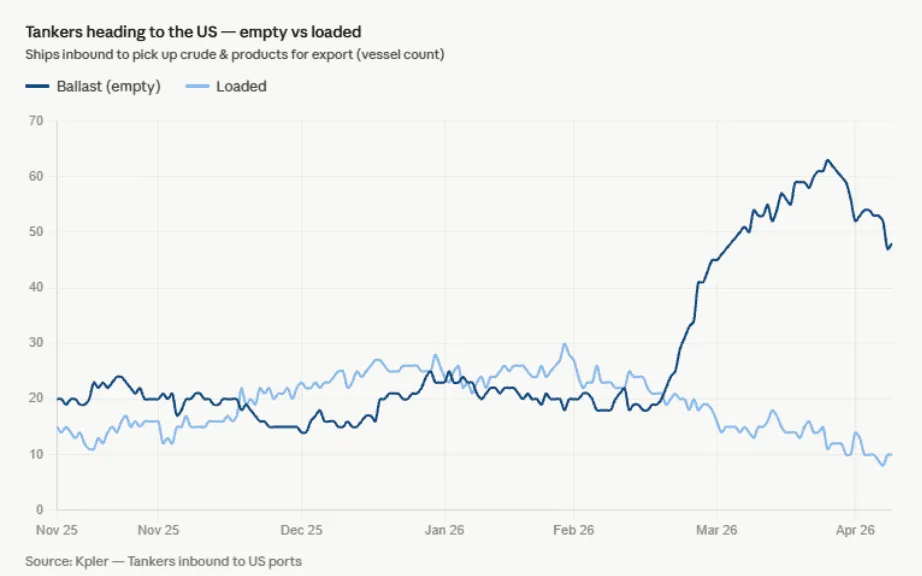

But the President sang the Siren’s song, and the empty ships have turned toward the music.

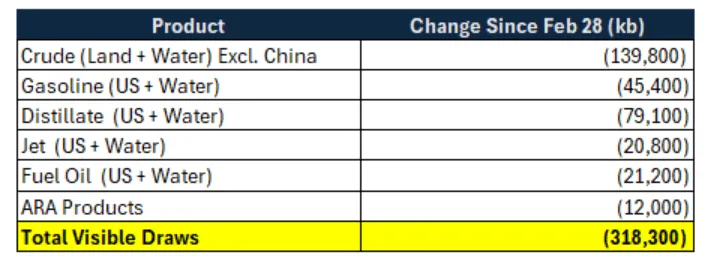

Over the last 67 days, global liquid inventories have drawn at a rate exceeding 6 million barrels per day, amounting to more than 400 million barrels and counting. We can observe much of this drawdown in near real time through declining crude inventories outside China, falling US and ARA stocks, and the steady depletion of oil on water, which together account for more than 300 million barrels already removed from the system. The remaining draws are occurring in countries that report inventory data far more slowly.

Headed toward the Rocks

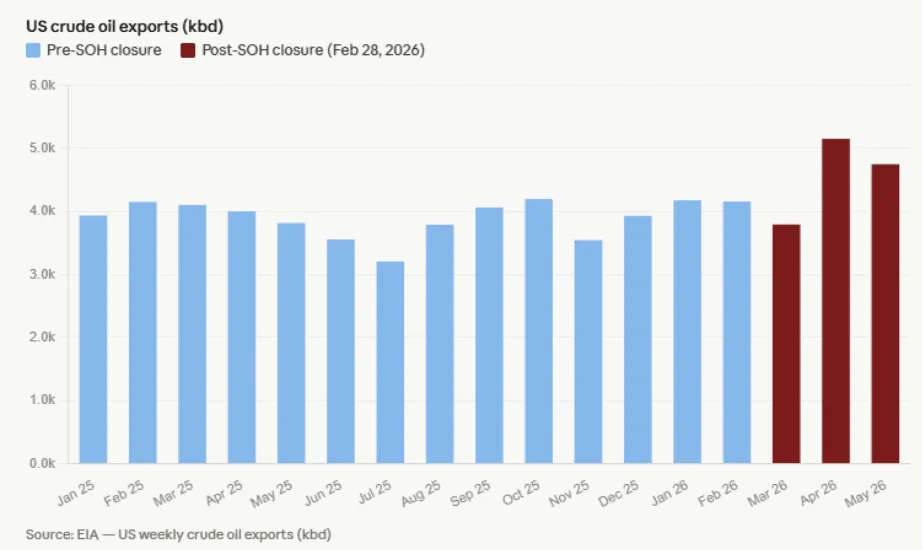

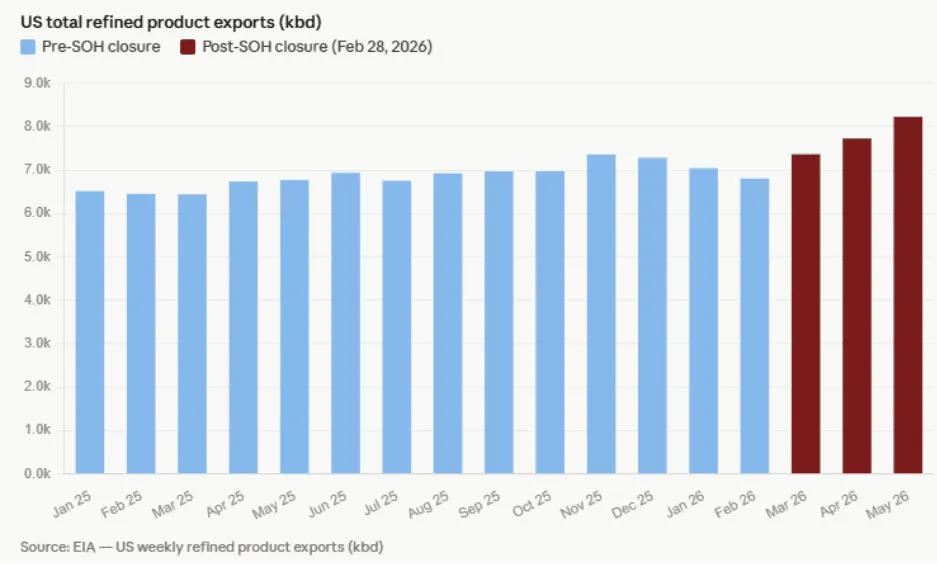

The fastest inventory drawdowns occurred first on the water before moving onto land, where we are now seeing both US export rates and the drawdown of US inventories accelerate sharply.

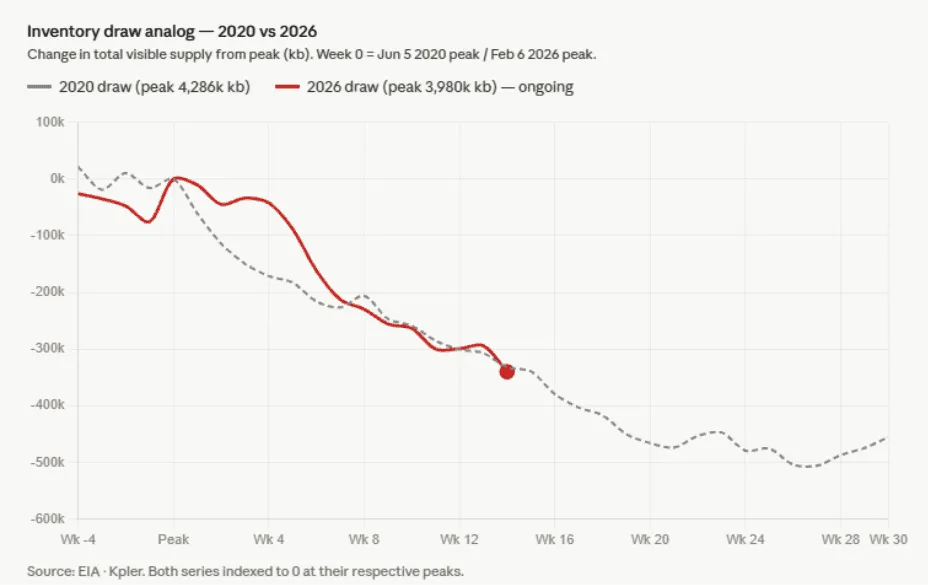

The pace of the current drawdown is comparable to what we witnessed in 2020 after the world effectively came to a standstill and inventories had risen so dramatically that oil prices briefly turned negative. By the time inventories began drawing in 2020, OPEC had already implemented deep production cuts, global supply had collapsed under the weight of negative prices, and economies around the world reopened simultaneously, unleashing a powerful recovery in demand.

There is one critical difference between then and now. In 2020, the world began drawing inventories from an enormous surplus. Global stocks were nearly 300 million barrels higher than where they stood at the start of this war. The market was working through excess inventories accumulated during the collapse in demand.

Today, the world is drawing from a far smaller buffer. The draws are feeding directly into rising prices in the United States. As tankers continue arriving at US ports empty, loading crude oil and refined products for export abroad, while domestic inventories continue to tighten. In effect, the United States is essentially exporting relief to the global market while importing pain to the US consumer.

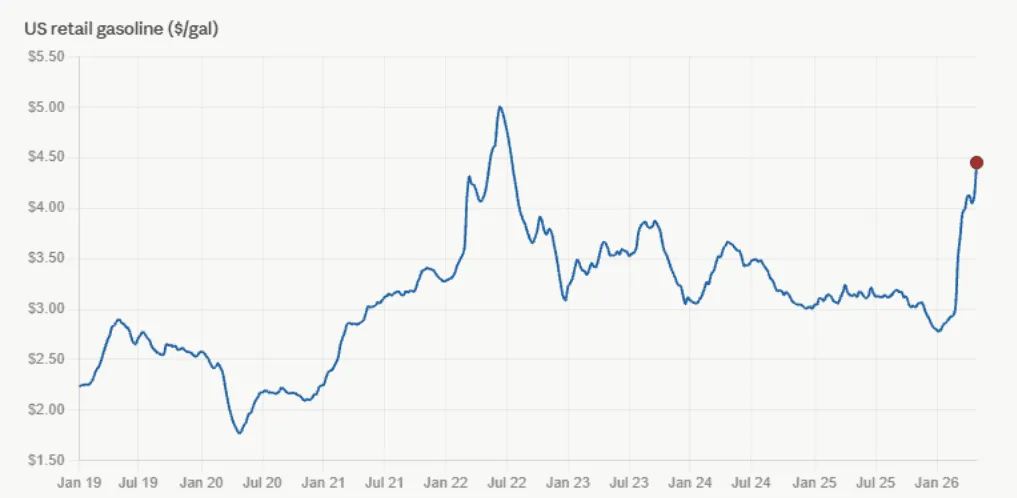

Last week, the national average price for gasoline in the United States rose above $4.50 per gallon and is now inching toward the psychologically important $5 threshold. At the current pace of inventory drawdowns and rising oil prices, the United States is on track to reach $5 gasoline by Memorial Day, making summer travel plans increasingly expensive for American households.

Source: FRED

Restraint at the Helm

As gasoline and diesel prices continue rising and the Federal Reserve works to contain another inflationary wave from spreading through the US economy, the political pressure on the White House will intensify dramatically.

The closer gasoline moves toward $5 per gallon — and the closer the country moves toward the midterm elections — the stronger the temptation will become to intervene directly in energy markets. Export controls, refined product restrictions, gas tax holiday, additional SPR releases, or other emergency measures will increasingly be discussed as ways to shield American consumers from rising fuel prices.

And politically, the argument will sound compelling.

Why should the United States continue exporting crude oil, gasoline, diesel, and jet fuel abroad while domestic consumers face rapidly rising prices at home?

But this is where the global oil market becomes dangerous politically. The apparent solution can easily deepen the underlying problem.

The President sang the Siren’s song and the ships answered.

“All of those countries that can’t get jet fuel because of the Strait of Hormuz… I have a suggestion for you: Number 1, buy from the U.S., we have plenty…”

Tankers from around the world are now turning toward the United States. The global market is reorganizing itself around American exports because the United States has become the supplier of last resort. Europe and Asia have already drawn down much of their available inventories, oil on water has fallen sharply, and there are few remaining buffers elsewhere in the system capable of absorbing the loss of Middle Eastern supply.

And for a time, the system will continue functioning.

But there is a danger embedded in the promise of abundance.

The United States cannot fully replace the energy flows historically moving through the Strait of Hormuz. It can only partially bridge the gap by drawing down inventories, releasing strategic reserves, and exporting barrels that would otherwise remain inside the domestic system.

That is why export controls become so dangerous. Rising domestic fuel prices will make restricting exports increasingly attractive politically. But once the ships have turned toward the United States, sending them away again risks intensifying the very shortages and price shocks the market is already struggling to contain.

The longer the Strait of Hormuz remains closed, the more dependent the global market becomes on continued American exports and continued US inventory drawdowns to hold the system together. Allies have already reorganized supply chains around US flows. Inventories elsewhere have already been reduced in reliance on continued American supply.

The United States cannot fully replace the energy flows lost through the Strait of Hormuz. It can only slow the adjustment by consuming the inventories and strategic buffers that once protected the global market from sustained disruption.

Now that the ships have turned toward the song, the world is drifting toward the rocks.

To understand more about the mechanics of US exports click here.

Market insights you can trust

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

See why the most successful traders and shipping experts use Kpler