EIA Digest: Crude inventories continue to draw; jet fuel stocks hit new ytd high

The latest EIA data release for the week ending 29 May showed a sixth consecutive weekly draw in crude inventories amid elevated exports, while crude intake eased slightly and utilization edged up w/w. Total product stocks were up as all product groups posted builds, with implied demand easing w/w but continuing to surpass year-ago levels on a four-week average basis. The latest data on retail prices showed a cooling in both gasoline and diesel pump prices to below 2022 levels for a second consecutive week.

Market and Trading Calls:

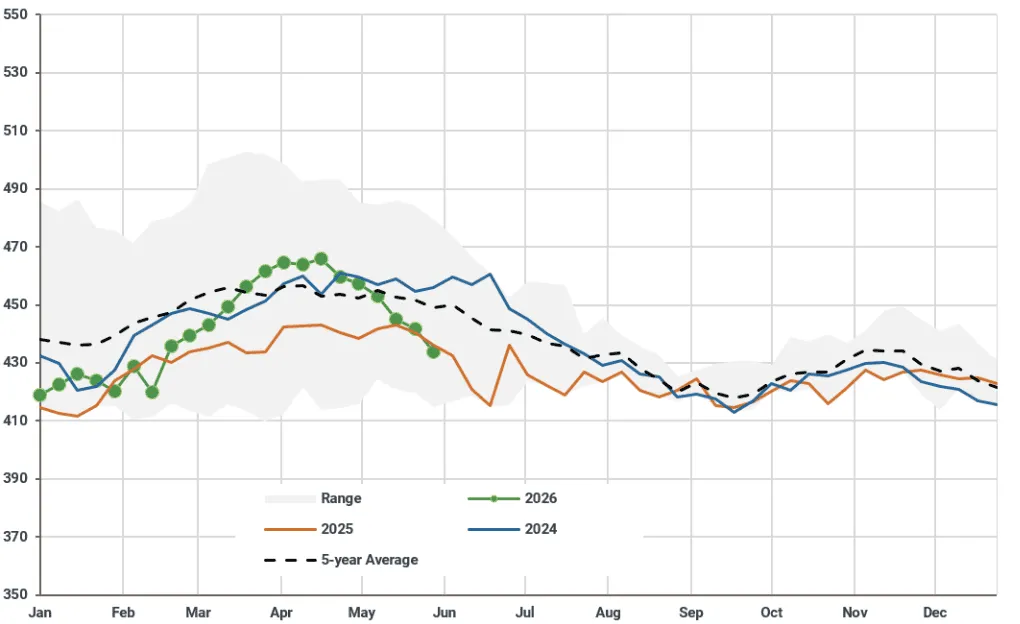

- US commercial crude inventories recorded an 8Mbbl w/w draw, a sixth consecutive weekly decline, standing 3% below the seasonal five-year average.

- Refinery intake decreased by 90kbd w/w, but utilisation rates edged up 0.2pp w/w to 94.7%, remaining at the upper end of the seasonal range.

- Product inventories were all up, as total implied demand eased on the week, although it continues to overshoot year-ago levels on a four-week average basis by 3%.

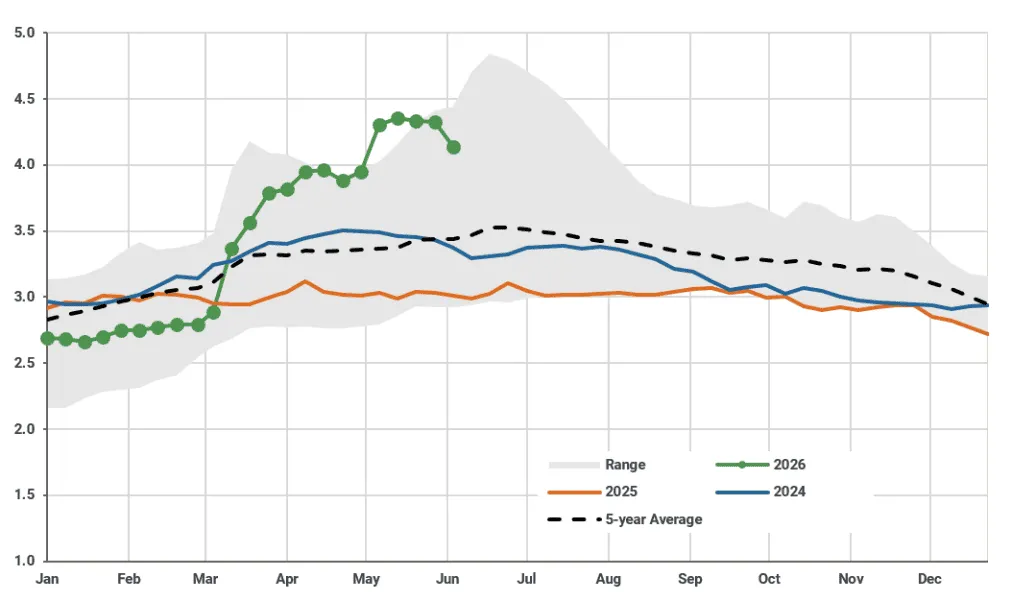

- Yesterday’s data on retail prices showed the largest fall in gasoline pump prices ytd, with diesel prices also continuing to ease. Although retail prices remain seasonally elevated, the latest data showed prices remaining below comparable 2022 levels for a second week in a row.

Today’s EIA Weekly Petroleum Status report for the week ending 29 May showed nationwide commercial crude stocks up by 8Mbbls to 433.7Mbbls, some 3% below the five-year average, as US crude exports remain elevated.

Refinery runs stood at 16.9Mbd, down just 90kbd w/w, while refinery utilisation edged up 0.2pp w/w to 94.7%, as maintenance activities are set to be negligible through to end-Q3, helping refiners maintain strong run rates over the summer season.

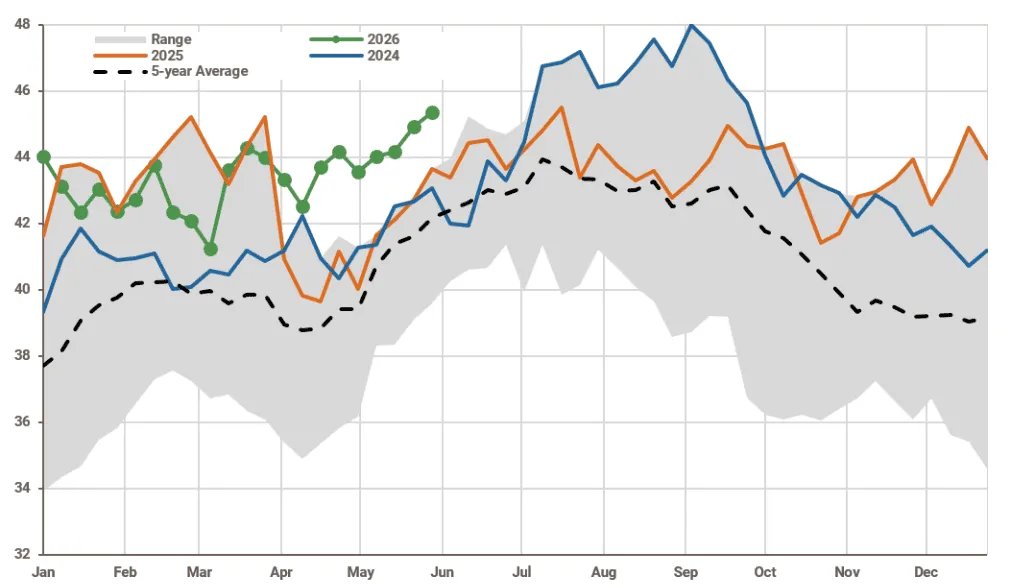

Indeed, elevated run rates and a weaker week for demand meant all product inventories were up, marking the first build for gasoline since February (+3.4Mbbls), and a new ytd high for jet fuel stocks at 45.4Mbbls. Despite a w/w dip, the four-week average of total products supplied stood at 20.4Mbd, overshooting year-ago levels by 3%, as transportation fuels demand remains resilient notwithstanding elevated retail prices.

Yesterday’s retail price data showed regular conventional gasoline prices down by 18.9cts/gal, the largest ytd fall, and diesel prices down by 17.3cts/gal, with much of the decline linked to falling crude prices over the past week, marking a second consecutive week of prices falling below corresponding 2022 levels. Still, the sustainability of these falls is fragile as a breakthrough in US-Iran negotiations remains elusive.

US: Weekly nationwide crude stocks (excluding SPR) (Mbbls)

Source: EIA

US: Weekly jet fuel inventories (Mbbls)

Source: EIA

Weekly US Regular Conventional Retail Gasoline Prices (Dollars per Gallon)

Source: EIA

Market insights you can trust

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler