French Power balance is under structural pressure this May

Holiday calendar, decentralised solar growth, and above-seasonal temperatures converge to create a perfect storm for French midday prices in May 2026, demand troughs near 30 GW collide with a must-run nuclear floor and a rapidly expanding solar fleet, raising the spectre of repeated -500 €/MWh episodes through the month.

Executive Summary

- The midday supply-demand mismatch is severe and worsening. On low-demand holiday days, grid demand can fall as low as 30 GW. Demand minima already printed nearly 5 GW below seasonal norms at end-April, in part reflecting the accelerating contribution of behind-the-meter (BtM) solar. On the supply side, price-insensitive solar output reaches 15-20 GW and nuclear baseload holds a technical floor of 20-25 GW. With no export outlet relief, this structural must-run surplus is driving Single Day-Ahead Coupling (SDAC) spot prices to the -500 €/MWh floor during midday hours.

- Holidays and temperatures as near-term catalyzers. France's May holiday calendar is uniquely concentrated this year near weekends as public holidays fall on Mondays, Thursdays or Fridays. This incentivizes long weekends. The temperature outlook amplifies the risk. ECMWF month-ahead forecasts higher than normal temperature anomalies across all of Europe for May 2026.

- Solar capacity increased + 6 GW y/y mostly driven by small scale solar installations. The result is a rise in self-consumption which erodes grid demand, widening the supply-demand midday mismatch. An extra catalyser of negative pricing.

When 30 GW of demand meets a 40+ GW must-run stack

France's power system carries a structural vulnerability during public holidays. From a fundamental perspective the supply-demand balance is shaped by:

- A large and healthy nuclear fleet (+3 GW availability in April 2026 y/y).

- A rapidly growing solar fleet (+ 6 GW y/y).

- A declining demand trend driven by deindustrialization, with the daily profile further compressed during midday hours by behind-the-meter solar growth.

- No export outlet relief during midday hours.

In short, the must-run supply stack is increasing while the demand profile stagnates.

Moreover, neighbouring countries, facing their own solar excess, add pressure by pushing exports into France rather than absorbing it.

Breaking down the factors driving the imbalance:

Load: On a typical low-demand May holiday, French grid demand can fall as low as 30 GW. Demand minima at the end-April printed nearly 5 GW below seasonal norms.

Other than temperatures running 3-4°C above seasonal average, it’s more a story of midday hours suppression and midday-to-edge-of-day load spread widening.

The most plausible explanation is the acceleration of BtM solar self-consumption.

Kpler Insight estimates that solar behind-the-meter growth eroded between 1.5-2 TWh of grid demand in April alone y/y, a structural erosion that does not appear in generation statistics but is visible in net load.

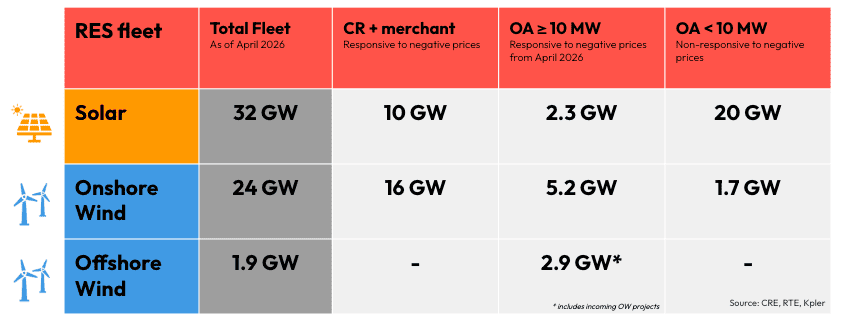

Solar: the total fleet now stands at 32 GW, up approximately 6 GW y/y, driven predominantly by decentralised installations. This creates two compounding effects: grid-injected solar displaces dispatchable generation, while BtM self-consumption simultaneously erodes midday net load.

Despite a September 2024 decree extending TSO curtailment rights over an additional 2 GW of OA contracts, Kpler Insight estimates that price-insensitive solar grid injection still reaches 15-20 GW at peak.

Nuclear: while the dominant pillar of the French power mix supports price formation at the edges of the day, intraday modulation could have touched its limit.

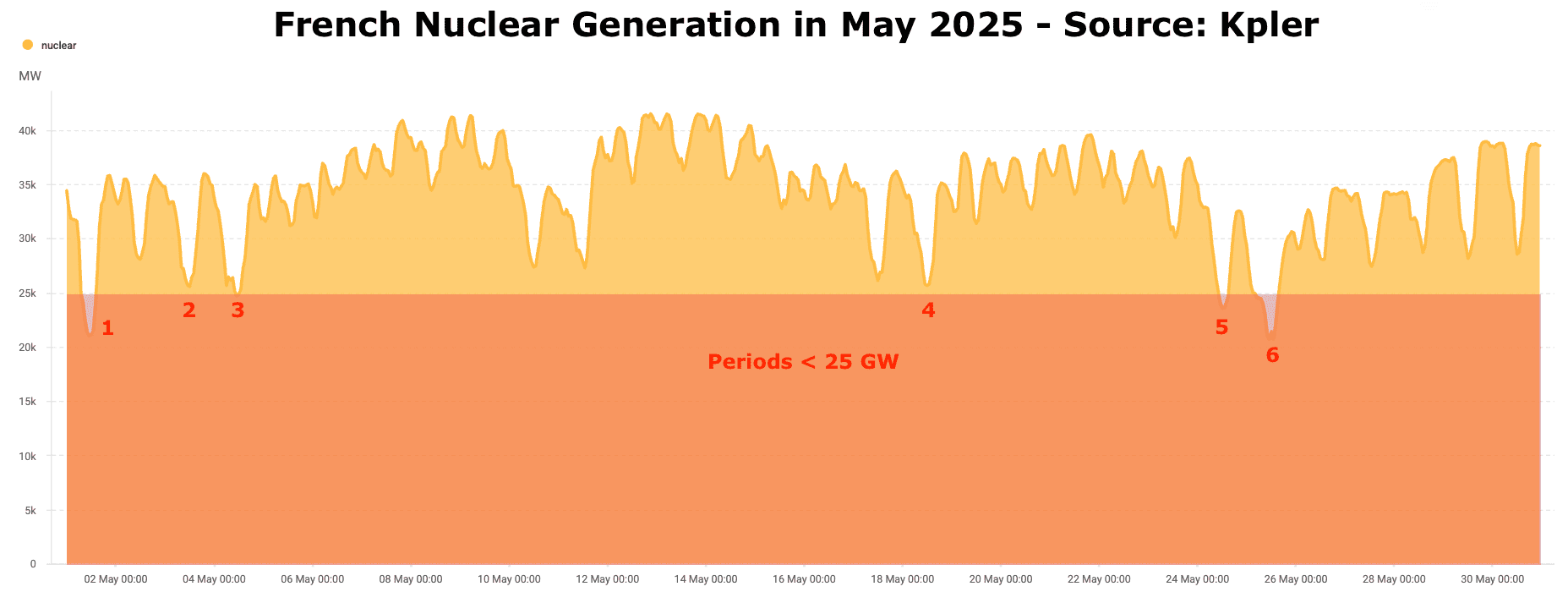

The fleet's minimum technical output realistically floors at 20-25 GW. This year, the floor could be further pushed up following the EDF-RTE voltage security agreement.

In fact, the last two French holidays recorded an unusual nuclear generation floor at 30 GW.

However, falling below a 20-25 GW threshold, according to EDF, would create operational ramp constraints that spill into the evening window, compounding voltage security risks where the spinning reserve is already thin.

Neighbouring landscape: with residual demand levels below 0 GW in almost all neighbouring countries during peak solar hours, cross-border flows provide no relief.

If any, neighbouring countries are themselves net exporters, amplifying (rather than absorbing) the French balancing challenges.

In short, the implied must-run stack already exceeds grid demand before a single dispatchable unit bids into the market.

The result is almost inevitable: during midday hours market prices clear at must-run generation levels, which mostly coincide with the SDAC floor, that is -500 €/MWh.

The system is being forced to clear at price levels it was never designed to reach.

3 converging factors make May 2026 particularly acute

The structural imbalance described above is not new. What makes May 2026 distinctive is the simultaneous alignment of an additional two amplifying factors:

- Holiday calendar concentration: this May, public holidays fall on days that anchor long weekends, meaning consumer behaviour-driven demand suppression extends across multiple consecutive days.

- Hot temperature outlook: the ECMWF month-ahead forecast for May 2026 has shifted to broad positive temperature anomalies across all of Europe. For France in May, above-seasonal temperatures still sit below the cooling activation threshold, leaving net grid demand structurally lower with marginal offsetting effect.

All together, they set the stage for May 2026 to extend and deepen the -500 €/MWh midday episode pattern first observed over Easter and May 1st.

See why the most successful traders and shipping experts use Kpler