Friday's risk-off and the IPO supply wall

Friday handed equities their roughest session in more than a year. The Nasdaq 100 fell around 5% — its steepest one-day drop since spring 2025 — while Bitcoin slipped below $60,000 and Treasury yields jumped.

Semiconductors were the epicentre and by far the biggest single drag on the index, with chip bellwethers shedding double digits and on the order of $1 trillion in market value wiped from the complex in a day. The immediate trigger was a stronger-than-expected May payrolls report (172,000 jobs added, unemployment steady at 4.3%), which reaffirmed the rate narrative: the market has been pricing a rate hike for a while, but it has taken time for the equity market to absorb this reality. Counterintuitively, good economic news has become bad market news, since it strips away the rate relief that had underwritten months of gains.

The setup was fragile. After nine consecutive weekly advances and positioning stretched near maximum long, the market had little margin for a hawkish surprise.

A finite pool of capital, an unprecedented supply of paper

The more structural story is a historic convergence of equity issuance onto the same speculative dollars. SpaceX is marketing what would be the largest IPO ever — roughly $75 billion raised at $135 a share for a valuation near $1.8 trillion, with a sizeable slice aimed squarely at retail. Alphabet has unveiled an $80 billion equity package to fund AI infrastructure; Meta is reportedly weighing its own raise; and OpenAI and Anthropic are expected to bring mega-listings of their own before year-end.

Each of these is, in effect, a competing claim on a fixed pool of risk capital. With a record pace of new fund launches layered on top — more than 600 ETFs in six months — the marginal investor is being pulled in too many directions at once. The question is no longer whether demand exists; it is whether the market can absorb the backlog without cannibalising existing positions.

Q1 earnings were strong — but the valuation bar keeps rising

This lands against the backdrop of a Q1 2026 earnings season that was, on the whole, robust, with mega-cap tech once again carrying the index. The problem is that beats alone no longer move the needle; the market now trades on the scale of AI capital expenditure rather than on this quarter's print. Alphabet has signalled 2027 spending well above its roughly $190 billion 2026 budget — with some estimates approaching $300 billion — while Meta has lifted its own capex guidance toward $145 billion. At that magnitude, outlays are beginning to exceed operating cash flow, which is precisely why these names are now turning to equity markets. The result is dilution, a higher hurdle for future returns, and valuations that leave almost no cushion for a rate scare.

Bitcoin's slide is partly the rates story, but it is also a competition-for-capital story. Crypto, the most liquid and speculative pocket of the retail book, is the path of least resistance for raising cash. Friday's move erased much of Bitcoin's post-election gains.

Monday: a narrow bounce, not an all-clear

The selloff looks less like a verdict on fundamentals than a liquidity and positioning event: too much paper, too little dry powder, and a rate narrative that turned at the worst possible moment. Whether it proves a healthy reset or the start of something more serious hinges on the mid-June Fed meeting and on how cleanly the IPO pipeline clears in the weeks ahead.

Equities steadied at Monday's open, with the Nasdaq 100 recovering around 1.5% and the S&P 500 roughly 0.8% as semiconductors led the way back; A renewed Israel–Iran exchange — the first direct one since April — pushed crude higher (Brent near $95, WTI near $92), adding an energy-led risk vector worth watching alongside the rates story. Recovering barely a third of Friday's loss does little to resolve the supply-and-rates overhang; it confirms that dip-buying reflexes remain intact, not that the inflection point has passed.

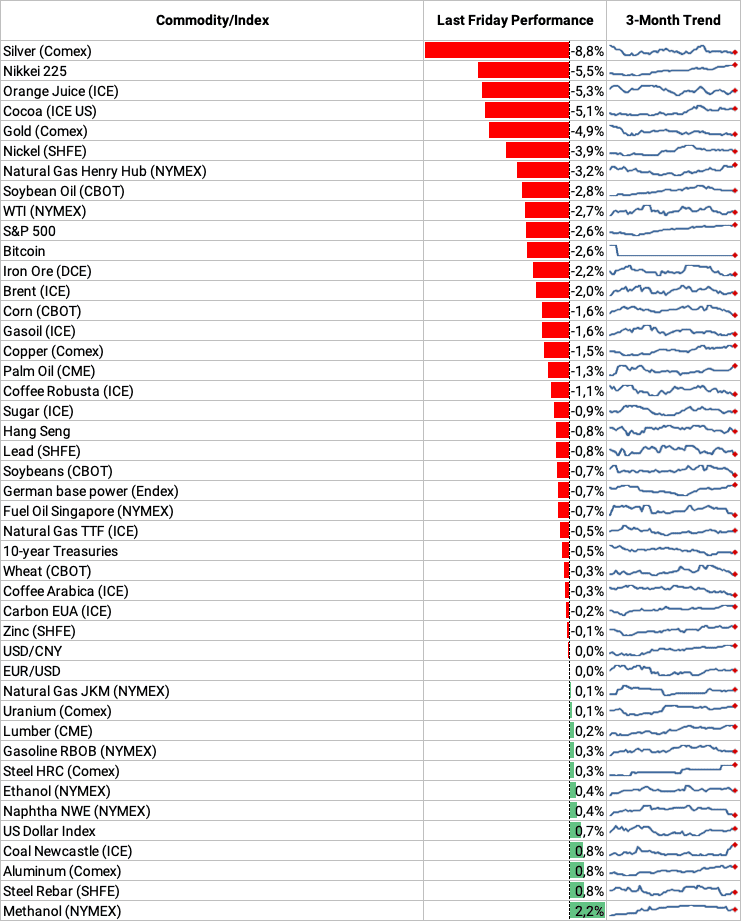

Friday commodities and Indices performance

See why the most successful traders and shipping experts use Kpler