Heatwave drives 34% y/y increase in European gas generation in Week 26

The late-June heatwave pushed gas generation above 5-year seasonal averages for the first time in Q2 across Europe. GB and Italy accounted for 59% of the generation increase, shifting interconnector flows across Europe. With temperatures set to spike again during Week 28, evening tightness and high prices look set to return, boosting gas generation.

Executive Summary

- European gas generation rose 34% y/y and 28% w/w in Week 26, as low wind generation, record heat, and nuclear outages drove gas demand across Europe.

- GB and Italy accounted for 59% of the increase in gas generation. GB burn more than doubled (+123%) y/y as falling imports alongside a +2% y/y rise in demand drove up gas generation.

- Gas supplied the evening ramp: generation exceeded 80 GW during evening peaks in Week 26 as solar faded and wind remained well below seasonal levels.

- Hotter temperatures look set to return from 6 July, potentially lifting gas generation further as hydro stocks are rationed and drought risk rises across Europe.

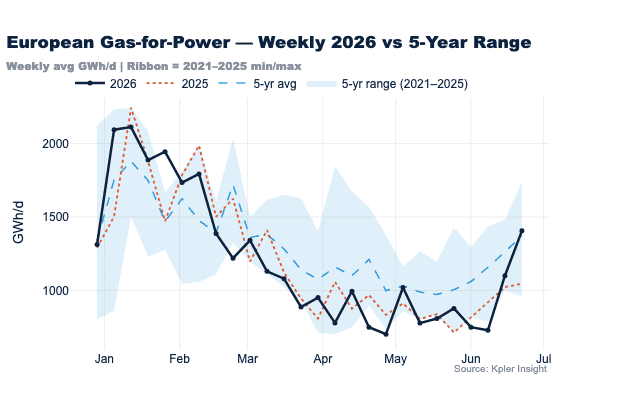

The heatwave through Weeks 25 and 26 snapped Q2's sluggish gas generation, taking gas-for-power demand up 34% y/y and 28% w/w in the week to 28 June, above the 5-year seasonal average for the first time this quarter.

Higher demand, lower wind and temperature-related nuclear outages drove gas generation to the highest level since Week 10.

Increased gas generation in GB and Italy accounted for 59% of the total European increase y/y. GB saw the biggest y/y increase on the continent, up 148 GWh/d (+123% y/y), while Italy saw a 106 GWh/d increase (+35% y/y).

Other gas-capable markets moved too: the Netherlands increased 47 GWh/d (+80% y/y), France increased 45 GWh/d (+155% y/y), while Belgium also grew 33 GWh/d y/y (+109% y/y).

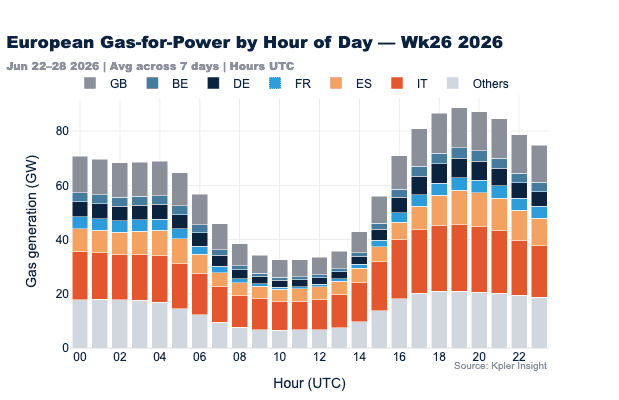

Gas burn was particularly notable during evening hours, when solar's share of the power mix fades. Gas ramped from a midday low of 32.5 GW to exceed 80 GW during peak windows, providing key flexibility to the European power system.

Demand rose across Europe

The heatwave lifted consumption across Europe. France led y/y demand growth (+4 GW, +9%), with Germany (+2.4 GW, +5%), Poland (+1.7 GW, +10%) and Belgium (+1.3 GW, +15%) also seeing increased demand.

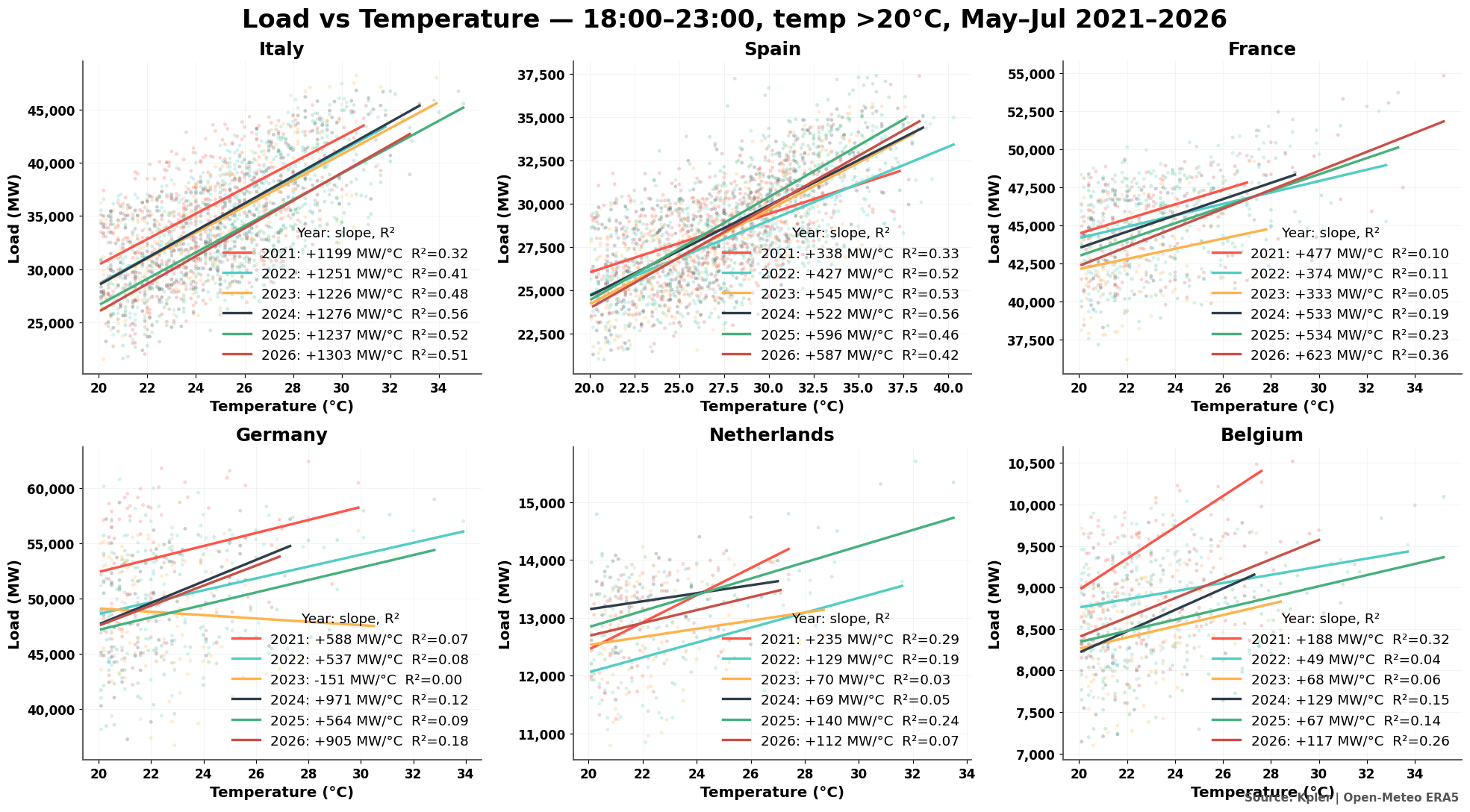

Evening temperature sensitivity (particularly in Southern Europe) is gradually increasing as air-conditioning (A/C) penetration rises, with France’s demand-temperature sensitivity strengthening in both magnitude (477 MW/°C to 623 MW/°C) and statistical fit (R² 0.10 to 0.36) since 2021.

Supply and interconnector flows in Week 26

Increased gas generation concentrated in markets that are gas-heavy and typically import during high renewables periods.

Wind generation collapsed across the continent: German wind fell to just 16% of seasonal during the 24 June evening block, with similar weakness across the CWE and CEE zones.

French nuclear also derated, with availability falling as much as 6.5 GW over the week amid high river temperature and low-flow constraints along the Garonne, Rhône and Seine. While the overall nuclear fleet availability is still up y/y, increasing French demand and falling nuclear output reduced French exports by 6.5 GW in Week 26.

GB’s net imports fell 64% (2.8 GW) w/w as cross-border supply tightened, while Italy's import position also fell by 6% (0.4 GW) w/w, forcing both onto their domestic gas stacks.

Tight supply drove prices sharply higher across Northern Europe, with Belgium hitting 1,000 €/MWh during the evening peak.

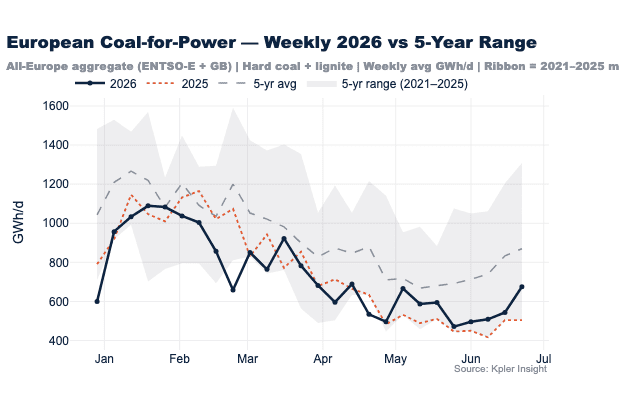

European coal generation also rose 24% w/w, driven by increased generation in Central and Eastern Europe. However, its absolute increase was a fraction of gas’s w/w increase (132 GWh/d versus 305 GWh/d) as the coal fleet increasingly shifts towards winter peaking.

Structural risks build beyond Week 28

Elevated temperatures look set to return around 6 July (Week 28) over France, before gradually shifting eastwards, according to our latest temperature outlook.

Sustained high temperatures will reduce European hydro stocks and shift French nuclear constraints from high-temperature limits toward drought-related constraints.

While nuclear availability looks strong in July, river flows continue to weaken, increasing the risk of drought-driven derating, potentially boosting gas generation through Q3.

Power Insights you can trust

Beyond a weekly report, Power Insight also includes:

- Ongoing market updates as events develop

- A monthly deep-dive report covering structural trends across European power markets

Interested in a demo to see everything Power Insight has to offer? Request a 30minute demo of Power Insight.

See why the most successful traders and shipping experts use Kpler

.jpg)