Hormuz escalation puts middle distillates at the center of supply risk

Escalating tensions around the Strait of Hormuz have reintroduced a geopolitical premium into distillate markets, with prompt gasoil structure firming sharply in response. Roughly 10% of global gasoil and 20% of jet fuel trade depends on uninterrupted Hormuz transit, leaving supply chains acutely exposed to disruption risk. With Atlantic Basin supply already constrained by refinery maintenance, distillate balances remain structurally sensitive to further escalation.

Key takeaways:

- Hormuz exposure is material, with 10% of global gasoil trade directly at risk of disruption

- Atlantic Basin constraints – USGC turnarounds, persistent PADD 1 demand, and potential Brazilian competition – are compounding upside risk for compliant barrels.

- Jet fuel markets face even greater vulnerability, with 20% of global jet/kero flows exposed to Hormuz transit risk

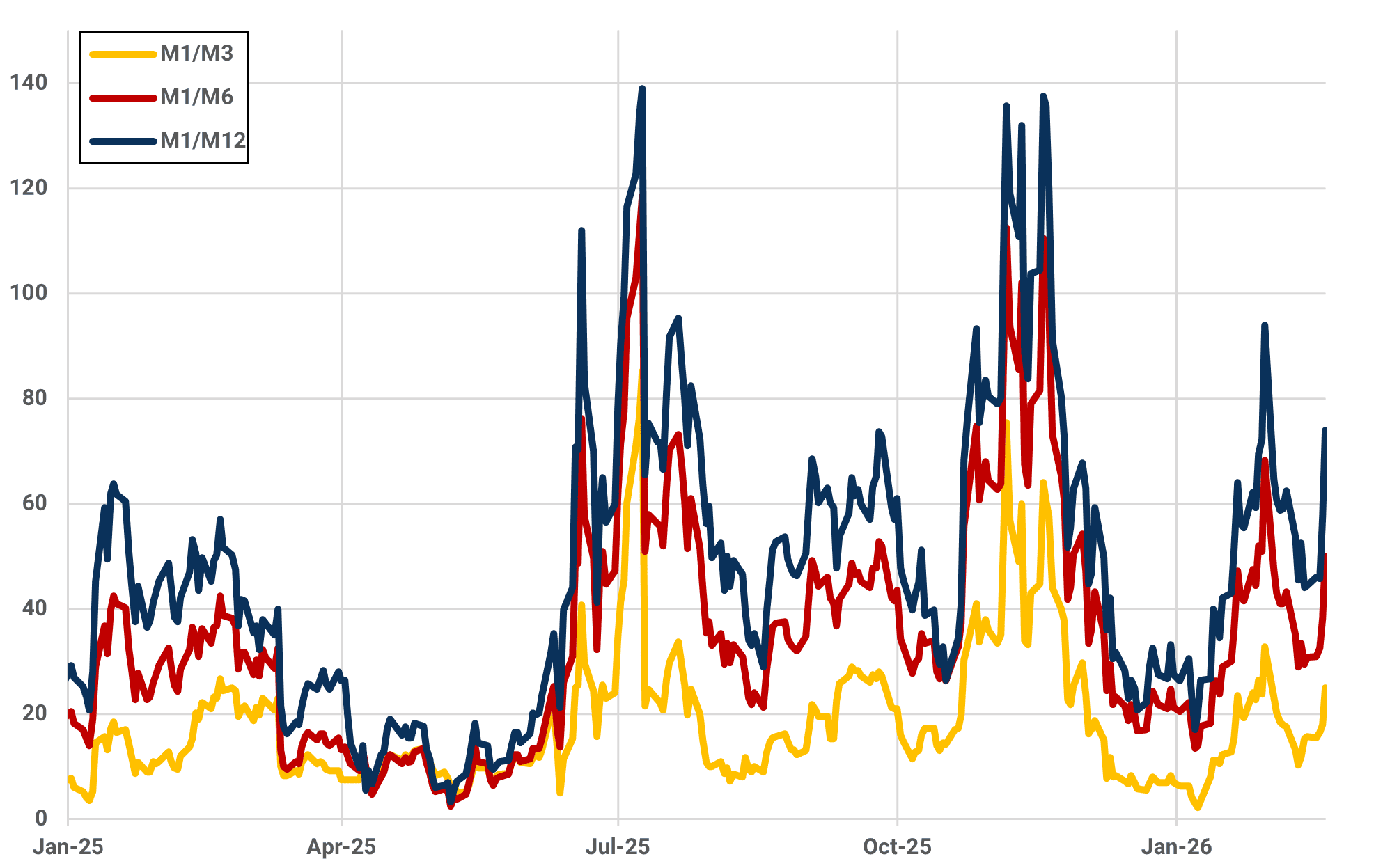

ICE Gasoil market structure excluding expiry days ($/t)

Source: Kpler using Marketview

Escalating US – Iran tensions have reawakened distillate markets. Live-fire drill closures around the Strait of Hormuz, joint Iran-China-Russia naval exercises, and increased US naval deployments have injected a renewed geopolitical premium into pricing. ICE gasoil structure has responded decisively, with prompt time spreads widening sharply as traders begin to price in the risk of disruption to Middle East distillate exports. This aligns with our earlier view that geopolitical escalation would represent a material upside risk to gasoil prices, given the market’s structural reliance on uninterrupted Middle East exports.

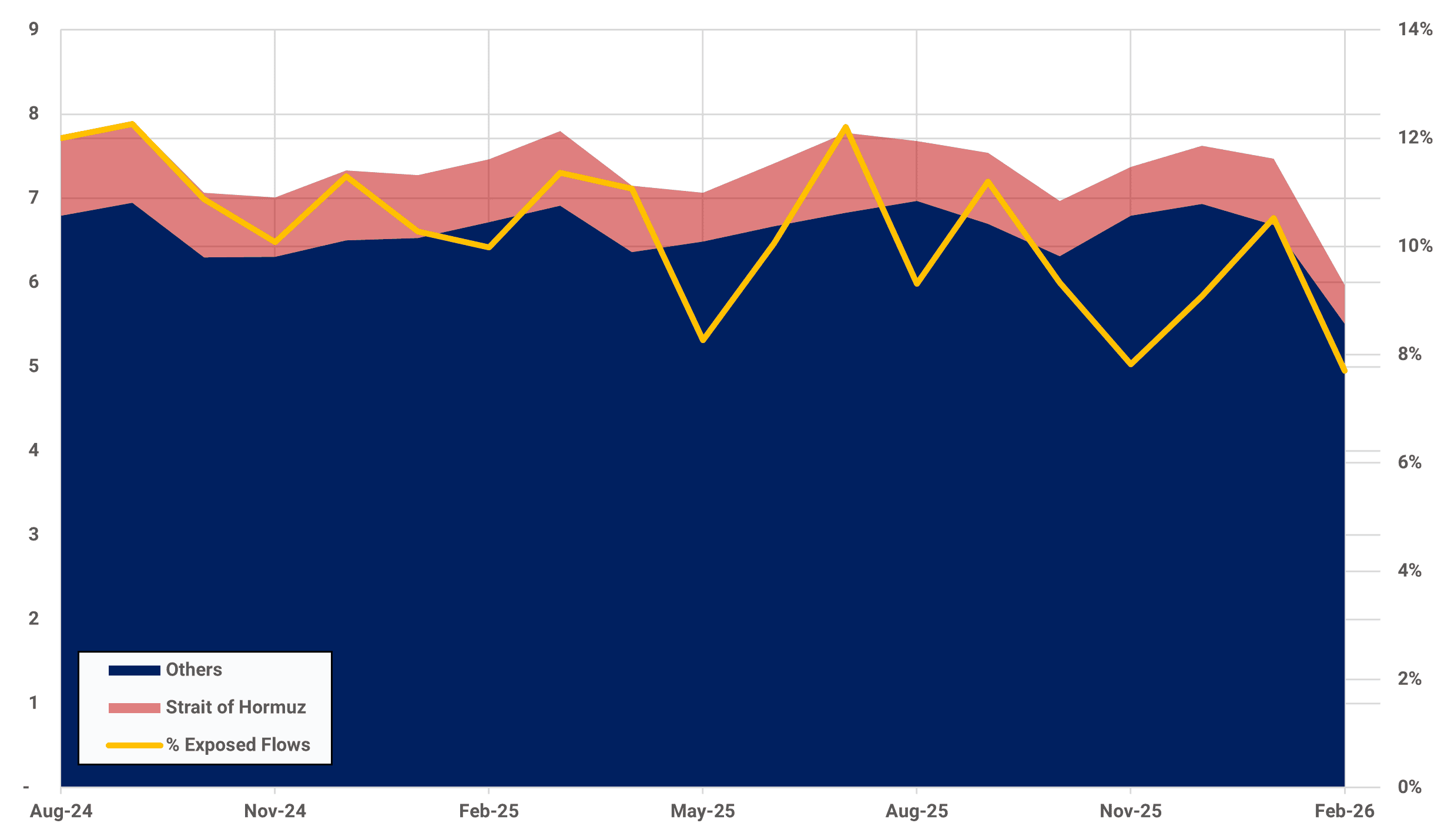

Fundamentals justify the market’s sensitivity to escalation. Kpler flows data indicates that exports loading via the Strait of Hormuz account for roughly 10% of global gasoil trade, averaging 750 kbd. This volume represents immediate disruption risk, and any protracted closure of the Strait – whether through deliberate Iranian retaliation or because of active military conflict – would materially tighten prompt availability and reinforce strength in the global gasoil markets.

Global gasoil flows by region (Mbd) vs flows at risk (%)

Source: Kpler

Northwest Europe remains particularly exposed. Ongoing regulatory ambiguity surrounding the enforcement of EU Article 3ma continues to encourage cautious procurement behavior, raising the risk of excessive “self-sanctioning” even as compliant cargoes continue to discharge without incident. This leaves the region structurally reliant on uninterrupted Middle East supply, increasing its sensitivity to any disruption scenario. The timing could not be more inopportune, with NWE maintenance set to intensify next month, taking approximately 1.2 Mbd of CDU capacity and 276 kbd of hydrocracking capacity offline and further tightening regional distillate availability.

Competition for compliant barrels is set to intensify further. While US runs remain elevated, approximately 660 kbd of US Gulf Coast refining capacity remains offline due to seasonal maintenance, limiting export availability. At the same time, PADD 1 continues to draw barrels amid persistently low onshore inventories, with severe winter weather across the US Northeast likely to accelerate inventory draws and delay resupply. This has reduced spot export availability and tightened supply for marginal buyers. This dynamic reduces the system’s ability to offset any disruption to Middle East supply and leaves Atlantic Basin balances increasingly sensitive to further supply shocks.

Brazil could emerge as an additional source of incremental demand. Any renewed disruption to Russian refining capacity – including through further drone strikes – would likely curtail export availability and force Brazil to source replacement barrels from the US Gulf Coast. This would further tighten Atlantic Basin supply and intensify competition for compliant barrels.

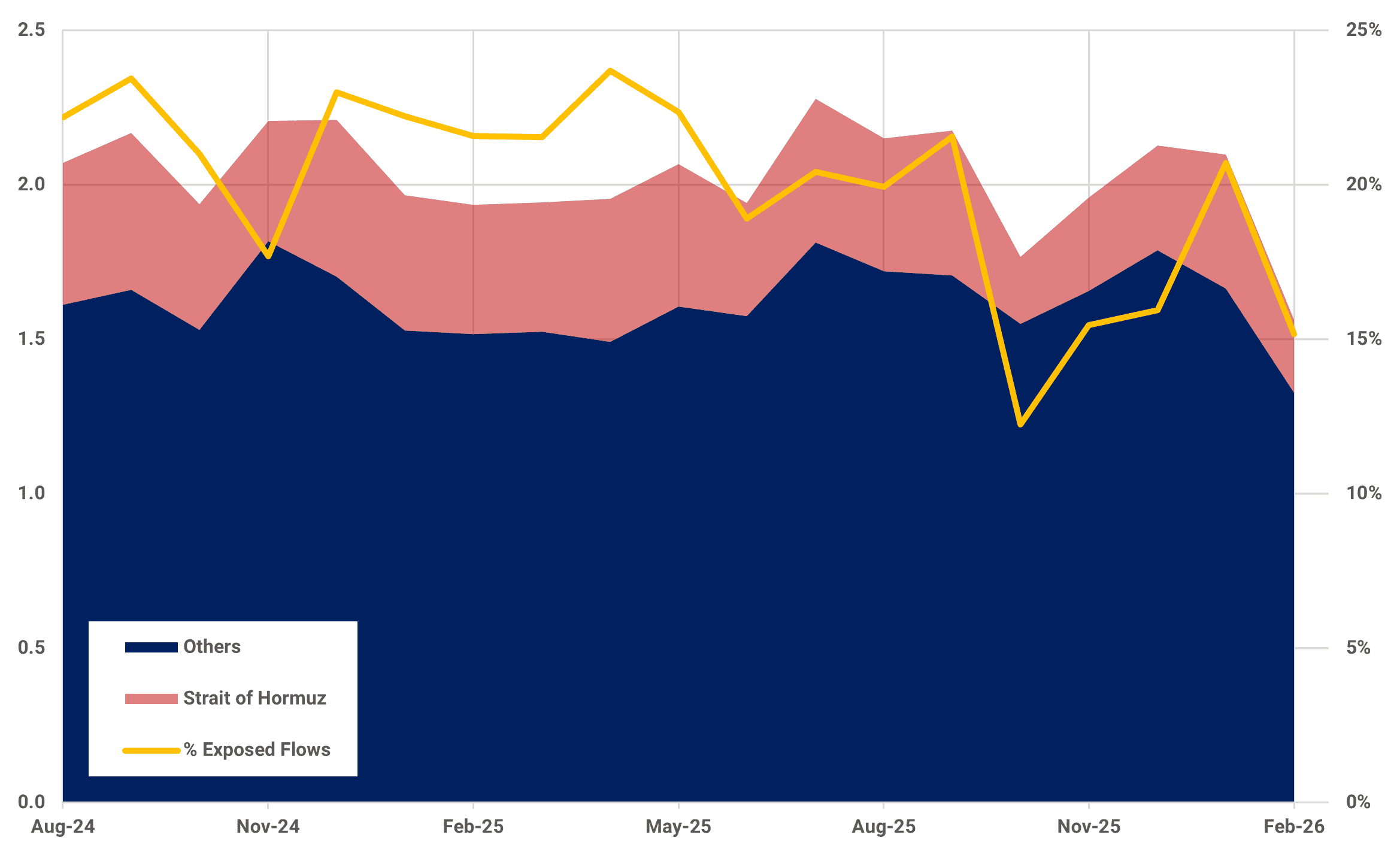

Global jet/kero flows by region (Mbd) vs flows at risk (%)

Source: Kpler

The stakes are arguably even higher for jet fuel and kerosene. Approximately 400 kbd – or 20% of global jet/kero trade – transits the Strait of Hormuz, leaving a significant share of supply directly exposed to disruption risk. The challenge extends beyond absolute volumes. Jet fuel procurement is typically structured through term supply agreements with strict delivery schedules, limiting buyers’ flexibility to rapidly pivot toward alternative suppliers.

Replacement is further complicated by stringent product certification, traceability, and regulatory requirements governing aviation fuel. Barrels must meet tightly controlled specifications and approved supply chains and cannot always be substituted interchangeably with spot cargoes. As a result, any disruption to established Middle East export flows risks creating localized shortages and disproportionately tightening jet fuel balances, even if headline global supply remains unchanged.

While geopolitical escalation remains the most immediate catalyst, it is unfolding against a backdrop of already constructive distillate fundamentals. The risk of US military intervention in Iran is adding to a market already on edge due to ongoing refinery maintenance, structurally tight supply, and continued competition for compliant barrels. This leaves the prompt well supported and reinforces the market’s sensitivity to any further deterioration in regional security, with risks continuing to skew to the upside.

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you to track critical crude oil market developments for your own analysis. Our precise forecasting empowers smarter trading and risk management decisions.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

.jpg)