Iran’s diminishing leverage

History suggests that strategic leverage is strongest when it remains unused, as efforts to weaponize it often drive investment in alternatives that reduce its long-term value. Iran's use of the Strait of Hormuz follows this pattern, with Gulf states expanding infrastructure to bypass the Strait and diminish its geopolitical importance.

There are moments in history when a nation decides to play its strongest strategic card—whether to assert its power, as with U.S. tariffs, or to defend its position, as Iran has done in the Strait of Hormuz. The immediate payoff can be significant, but the long-term consequences are often the opposite of what was intended. Strategic leverage is often strongest when it is merely possessed. Once it is wielded as a weapon, it creates powerful incentives for customers, competitors, and rivals to build alternatives.

OPEC's 1973 oil embargo remains the clearest example. In response to Western support for Israel during the Yom Kippur War, Arab oil producers cut exports and sent energy prices soaring. Yet by weaponizing their greatest source of leverage, they also galvanized the rest of the world to reduce its dependence on Middle Eastern oil. Strategic Petroleum Reserves were established, nuclear power expanded, North Sea and Alaskan production accelerated, and fuel efficiency standards tightened. The embargo demonstrated that the use of strategic leverage often plants the seeds of its own decline.

The same pattern has repeated itself elsewhere. Russia's use of natural gas exports, China's restrictions on rare earth minerals, and historical control of critical trade routes all prompted governments and businesses to invest in competing infrastructure and alternative supply chains. The lesson is consistent: the more aggressively leverage is exercised, the stronger the incentive becomes to eliminate it.

That process is already underway in the Gulf. By threatening shipping through the Strait of Hormuz, Iran may gain short-term geopolitical leverage. But it has also strengthened the economic case for bypassing the Strait altogether. While many of the projects discussed below predate the recent crisis, the renewed threat of disruption has increased both their urgency and their economic justification.

The response is emerging across four fronts: expanding Saudi Arabia's Red Sea export capacity, increasing the UAE's bypass infrastructure, developing new export corridors through Oman, and, ultimately, investing in refined product infrastructure that reduces dependence on Hormuz altogether.

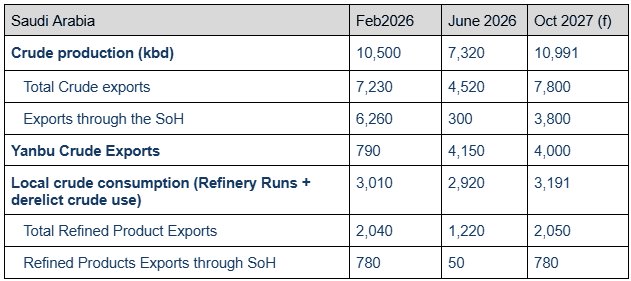

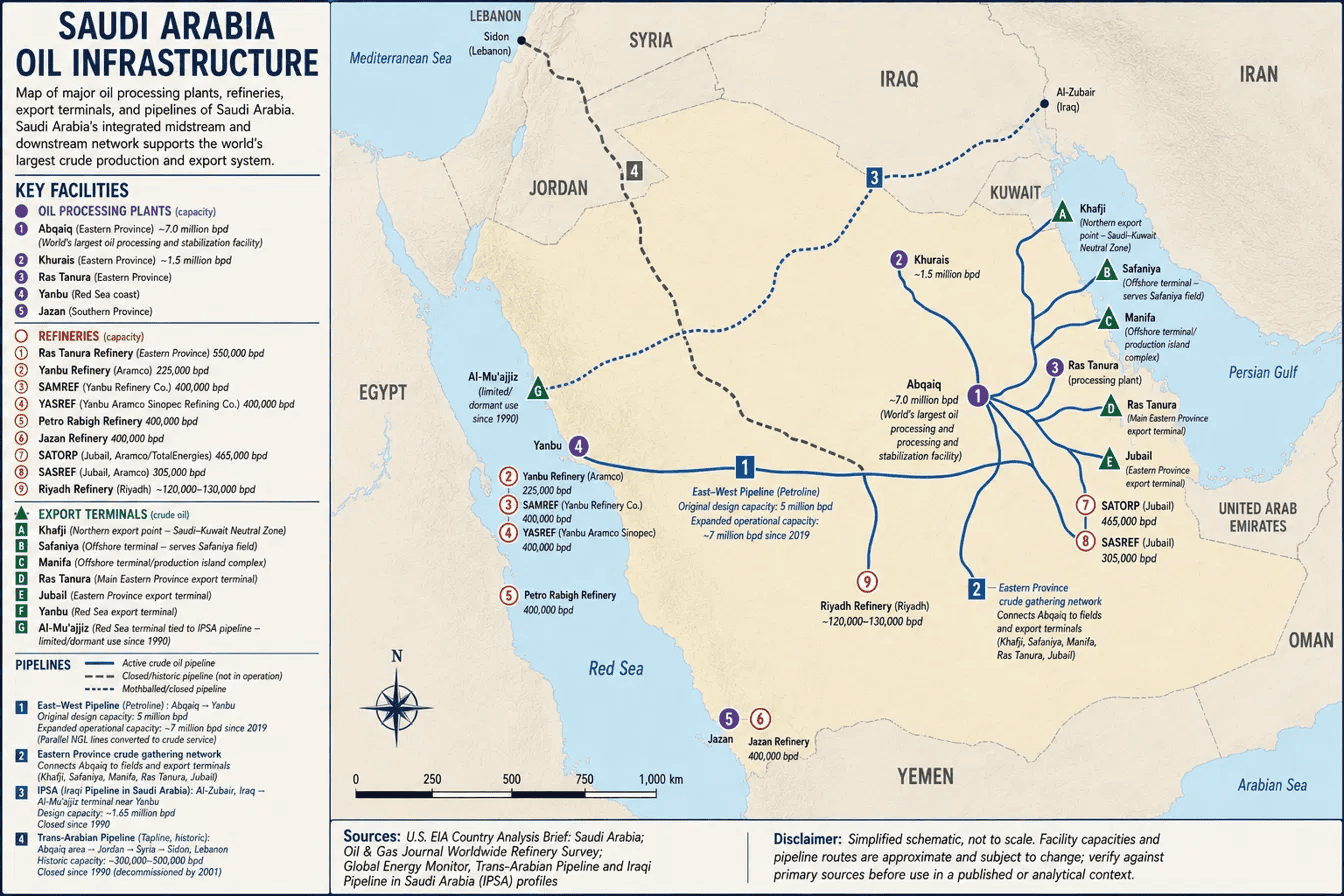

Saudi’s Yanbu Route

The first example is Saudi Arabia. They are already evaluating ways to expand exports through the Red Sea, reducing its reliance on the Strait of Hormuz. While the Kingdom's East-West Pipeline has the capacity to transport roughly 7 million barrels per day of crude from the Persian Gulf to the Red Sea, export infrastructure at the Red Sea terminal can currently only sustainably load about 4 million barrels per day, leaving substantial unused pipeline capacity. Expanding terminal and loading facilities would allow Saudi Arabia to better utilize this existing infrastructure and further diversify its export routes. In May, Aramco Chief Amin Nasser revealed that Saudi Arabia is pursuing plans to increase Yanbu’s export capacity to 5 million barrels per day.

Saudi Arabia also retains a second cross-country pipeline that has been largely idle for more than three decades. Although it is rarely discussed as a viable alternative today, the underlying infrastructure already exists, potentially lowering both the cost and lead time required to bring additional export capacity online.

Source: Kpler

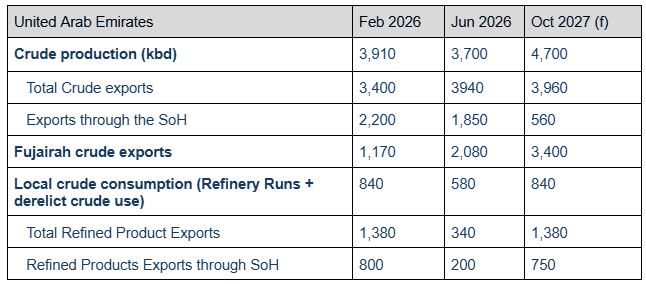

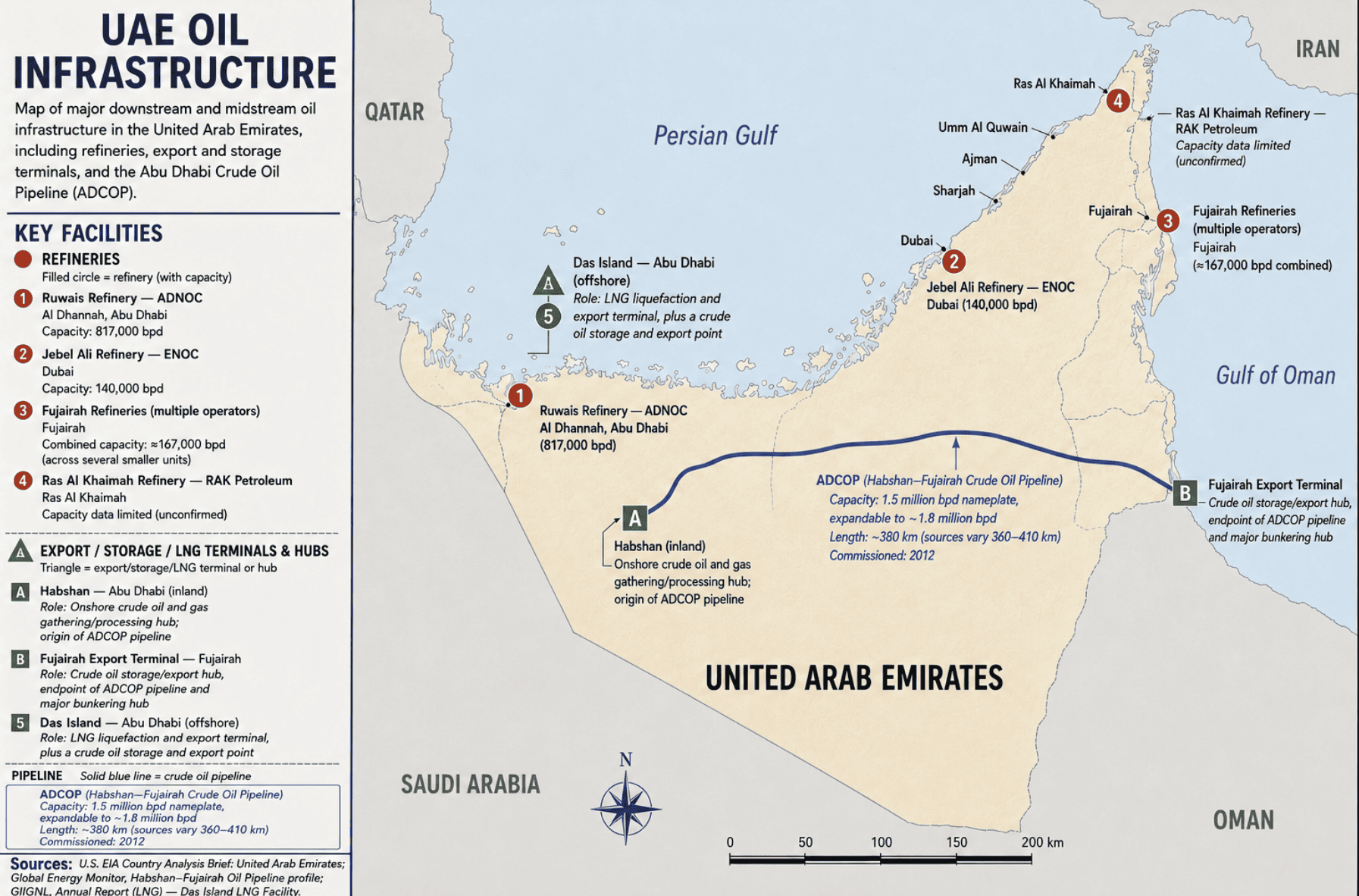

UAE’s Fujairah Route

The UAE has decided to accelerate its plans to double its pipeline export infrastructure as it aims to further reduce reliance on the Strait of Hormuz. The UAE has had a pipeline that bypasses Hormuz since 2012 when Abu Dhabi owned Adnoc opened the Habshan–Fujairah Pipeline, which can transport up to 1.8 mbd to the Port of Fujairah. This May, in response to continued disruptions in Hormuz, Adnoc decided to fast track construction of the previously undisclosed ‘West-East Pipeline’ project. The ‘West-East Pipeline’ will run parallel to the Habshan–Fujairah pipeline and will transport a further 1.8mbd of crude. In mid may, Head of Adnoc Sultan Al-Jaber stated that the project was “almost 50% complete”, with the expectation to become operational in 2027. When complete, the Emirates would have a pipeline capacity to bypass Hormuz of 3.6mbd. In order to maximise this opportunity, the UAE is also accelerating Fujairah’s crude export capacity expansion, aiming to increase it to 4 mbd by 2027.

Source: Kpler

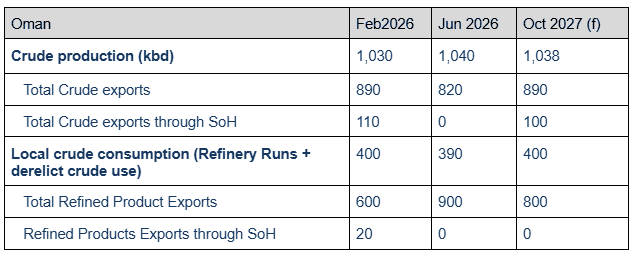

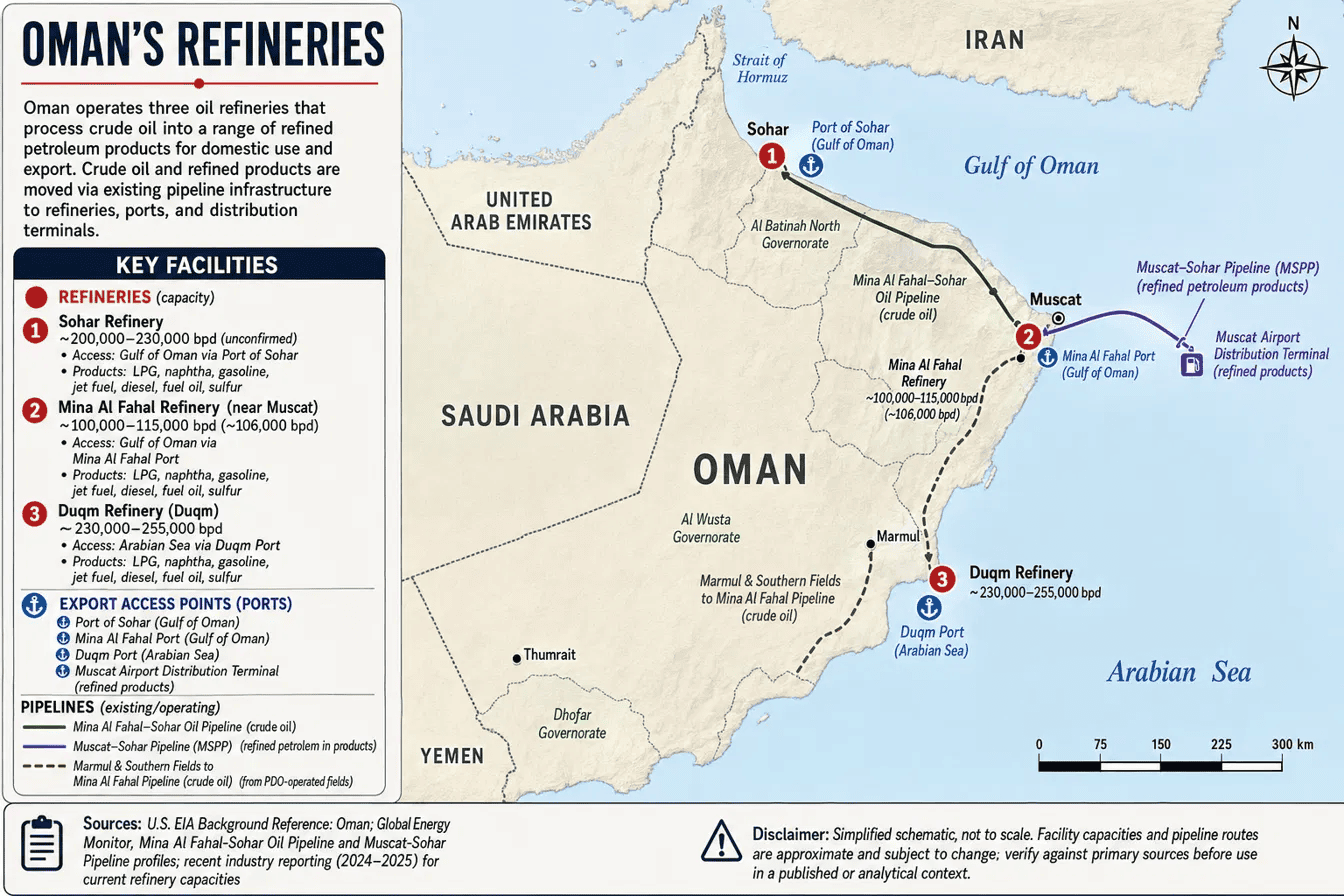

Oman’s Hopeful Route

Oman has also been positioning itself as an alternative export and trade corridor that bypasses the Strait of Hormuz. Over the past decade, Muscat has invested hundreds of millions of dollars in expanding the ports of Duqm and Salalah, marketing them as strategic trade and energy hubs. Located on the Arabian Sea, these ports offer direct access to global shipping lanes without requiring vessels to transit Hormuz. Duqm, in particular, is connected to the Ras Markaz strategic crude storage facility and includes its own refinery and dedicated crude and refined product export terminals.

While no major cross-border oil pipelines have yet been sanctioned to support this vision, Oman is increasingly central to discussions about the Gulf's future energy infrastructure. One example is a preliminary agreement with Iraq to study a pipeline from southern Iraq to Duqm, providing Baghdad with an export route that bypasses both the Strait of Hormuz and Turkey.

The real significance of Oman's investments, however, is that they have created the foundation for future diversification. Decades of political neutrality have made Oman a trusted partner across the region, while its geography places it outside the Strait of Hormuz. Every time Iran threatens to disrupt shipping through the Strait, the economic and strategic case for expanding infrastructure through Oman becomes more compelling. As with every other example of strategic leverage, the more frequently it is exercised, the greater the incentive to invest in alternatives that ultimately diminish its value.

The Refined Route

Taken together, Saudi Arabia, the UAE, and Oman illustrate how the Gulf is gradually reducing its dependence on the Strait of Hormuz for crude exports. Yet one critical route remains largely absent: refined products.

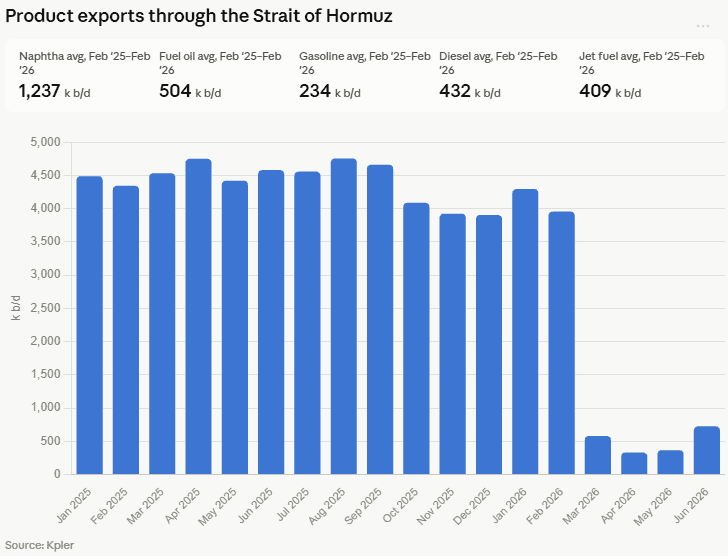

While the prospect of a Strait of Hormuz closure understandably dominated crude markets, the greater risk lay in refined products. Product markets—not crude—faced the tightest supply conditions. Even after crude prices retraced, refined product prices remained elevated relative to Brent, highlighting the continued scarcity of global refining capacity.

The global economy runs on refined products, not crude oil. With little spare refining capacity worldwide, consumers remain dependent on the Middle East not only for crude production but also for gasoline, diesel, jet fuel, and other petroleum products. Before the recent conflict, more than 4 million barrels per day of refined products transited the Strait of Hormuz.

In exposing that dependence, Iran has strengthened the economic case for eliminating it. Gulf producers have spent decades investing in crude export routes that bypass Hormuz, yet investment in refined product pipelines, storage, and export infrastructure has lagged behind. That imbalance is becoming increasingly difficult to justify. Although crude exports remain much larger than product exports, the refined product market is considerably tighter, margins remain attractive, and the economic incentive to capture more value through domestic refining has rarely been stronger.

If Saudi Arabia, the UAE, and Oman represent the first phase of reducing dependence on the Strait of Hormuz, investment in refined product infrastructure represents the next. The first reroutes crude. The second addresses the market's remaining vulnerability. Together they illustrate the same historical pattern: once strategic leverage is exercised, governments and markets begin investing to ensure it can never be exercised as effectively again.

Conclusion

Iran's geographic advantage cannot be moved, but its strategic importance can. Every pipeline built to the Red Sea, every expansion at Fujairah, every investment in Duqm, and every new product export route reduces the value of the Strait of Hormuz as a geopolitical weapon. History shows that leverage is most powerful before it is exercised. Once used, markets adapt, capital flows, and alternatives emerge. In attempting to maximize its leverage today, Iran may have begun the process of permanently diminishing it.

**This note was written the help from our summer intern, Oscar Von Stackelberg.

See why the most successful traders and shipping experts use Kpler