Qatar LNG arrivals ease Pakistan’s gas stress, but shortage to persist

Pakistan is set to receive its first Qatari LNG cargo since 2 March aboard the Al Kharaitiyat, ending a two-month disruption that severely tightened the domestic gas market. During the interruption, Pakistan secured only one spot LNG cargo from the US, forcing widespread demand destruction across the industrial and power sectors. Although three additional Qatari cargoes are expected in the coming weeks, incoming supply is still likely to remain below seasonal requirements, meaning industrial curtailments and pressure on the power sector will persist, albeit at a reduced intensity.

Market & Trading calls

- Pakistan LNG import forecast: Increased by 0.3 mt to 4.9 mt in 2026 in our latest LNG monthly report. This reflects improved access to Qatari term supply, facilitated through a government-to-government deal.

- Asian LNG prices: Stable, as incremental Pakistani LNG imports are expected to be met largely through facilitated term cargoes, capping upside to prompt spot demand.

The Al Kharaitiyat has become the first Qatari LNG cargo vessel to transit the Strait of Hormuz since the Middle East crisis started in late February. The ship passed through the waterway on 9–10 May and is bound for Pakistan under a reported government-backed arrangement aimed at easing the country’s LNG supply shortage. Sources indicate that three additional Qatari vessels are expected to undertake the same route in the coming weeks, though there are risks to the downside if vessels are unable to successfully transit the Strait of Hormuz.

Pakistan’s gas balance is expected to ease modestly in May, with assumed Qatari arrivals lifting LNG availability from 0.07 mt in April to ~0.3 mt and supporting higher gas-to-power burn ahead of peak summer cooling demand. However, the system remains structurally short: imports are expected to track well below normal summer requirements of 0.6–0.7 mt/month (9–10 cargoes), implying a deficit of ~five cargoes versus typical demand. As a result, the additional LNG is expected to alleviate demand destruction rather than restore normal gas availability.

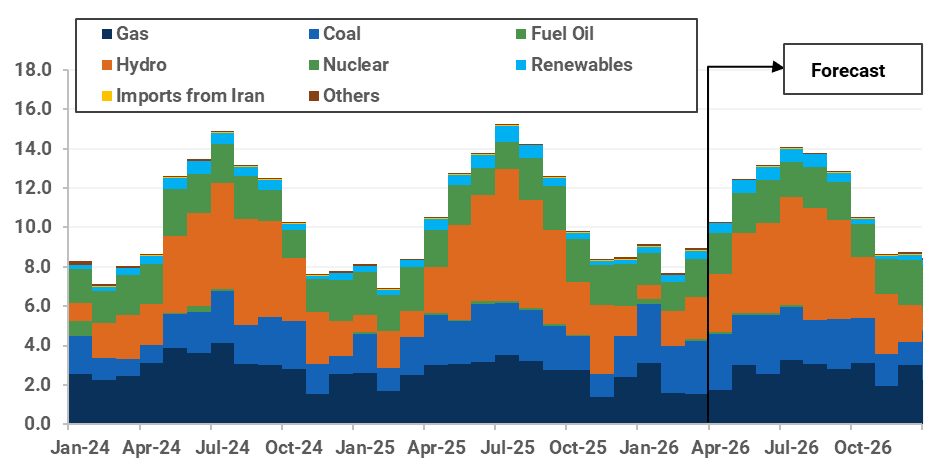

In the power sector, reliance on coal generation is expected to remain high, while nuclear output continues to offset part of the gas shortfall, with May 2026 power generation still estimated ~0.3 TWh lower y/y. Gas-to-power demand for 2026 is now expected at 8.8 bcm (-0.8 bcm y/y).

The forward picture still carries material risk. June LNG cargo visibility remains thin under the base case, with a more consistent resumption of Qatari term volumes assumed only from late June to early July. This keeps prompt spot LNG demand skewed to the upside if Qatari deliveries fail to materialize, although persistent FX and credit constraints cap Pakistan’s ability to procure spot cargoes aggressively. PLL’s cancellation of its latest May tender for two prompt cargoes, after a prior May tender was left unawarded despite seven bids at $16.98–17.28/MMBtu, underscores both the high replacement cost of spot LNG and Pakistan’s reluctance to buy unless term supply fails to materialise.

Kpler Insight now estimates Pakistan’s 2026 LNG demand outlook at 4.9 mt. Further government-to-government facilitation remains a likely alternative if Qatari term supply does not fully normalize, helping ease Pakistan’s gas balance and limit demand destruction without materially increasing spot exposure. The net pricing impact remains asymmetric: any renewed disruption or delay to these term flows could generate modest upside pressure on Asian spot LNG prices. However, Pakistan’s constrained ability to pay for high-priced spot cargoes should limit the scale of any spot demand response.

Pakistan historical and forecasted monthly gas demand by sector (bcm)

Sources: Kpler Insight, OGRA. Note: (1) Monthly proxies up to FY 2023–24 (ending June 2024) are based on historical data from OGRA; (2) From FY 2024–25 (starting July 2024) onwards, monthly figures are based on the Kpler Insight model.

Pakistan historical and forecasted monthly power generation (Twh)

Sources: Kpler Insight, NEPRA. Note: (1) Gas fired generation includes both domestic gas & RLNG fired while renewables include solar and wind generation; (2) April-2026 onwards are Kpler insight estimates.

See why the most successful traders and shipping experts use Kpler