Running out of barrels: cumulative oil losses hit 133 mbbls since the start of the war

Three weeks into the conflict, as shut-in barrels mount, cumulative losses are now on track to overwhelm the system’s limited buffers within weeks.

Key takeaways

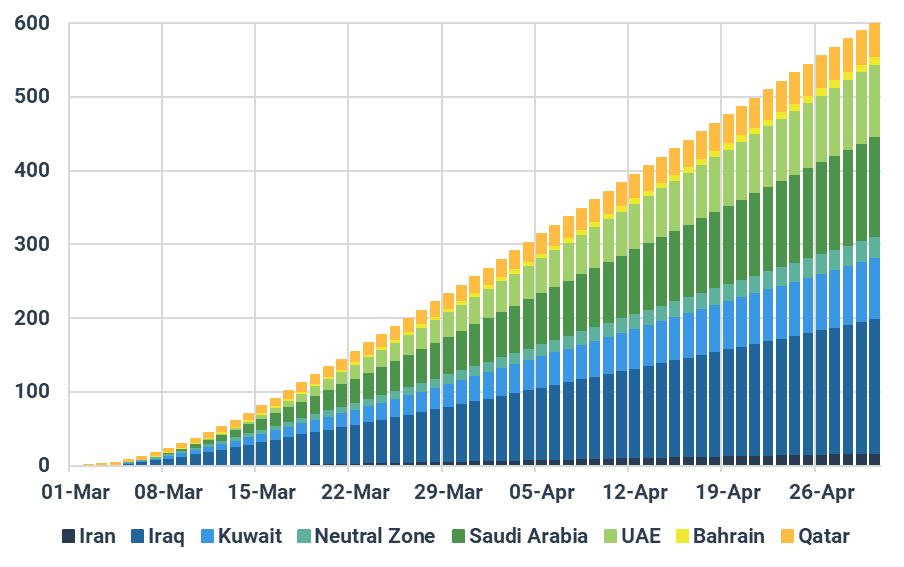

- Over 130 mbbls already lost, with cumulative disruptions set to exceed 250 mbbls by the end of March, 400 mbbls by mid-April and 600 mbbls by the end of April if flows don’t resume. This timeline suggests the US and Israel will look to end the war by mid-April, if possible.

- Production outages have reached 10.7 mbd by now and could jump to 11.5 mbd by late March. Refinery hits, not just export constraints, are also contributing to shut-ins.

- Short-term fixes (SPR, sanctions relief) can only delay, not offset, the growing structural deficit.

Friday 20 March 2026 marks Nowruz (the Iranian New Year) and Day 21 of the conflict. The US and Israel continue targeting military and IRGC bases across Iran, and earlier this week killed Ali Larijani, the Islamic Republic’s second most important official after the Supreme Leader. However, the Strait of Hormuz remains effectively closed, as risks are still deemed too high for most tankers. Since 1 March, only 21 tankers have managed to exit the Persian Gulf laden with crude, and just four of them were carrying non-Iranian oil.

This extreme situation has very quickly led to production shut-ins. Iraq, in particular, was forced to shut in a large portion of its production given limited available storage and a lack of ballast vessels in the Gulf. In the region, some fields, especially in Iraqi Kurdistan, also halted output as a precaution, with Iran firing missiles in nearby areas. This initially halted northern Iraqi exports, although flows through the ITP pipeline resumed earlier this week.

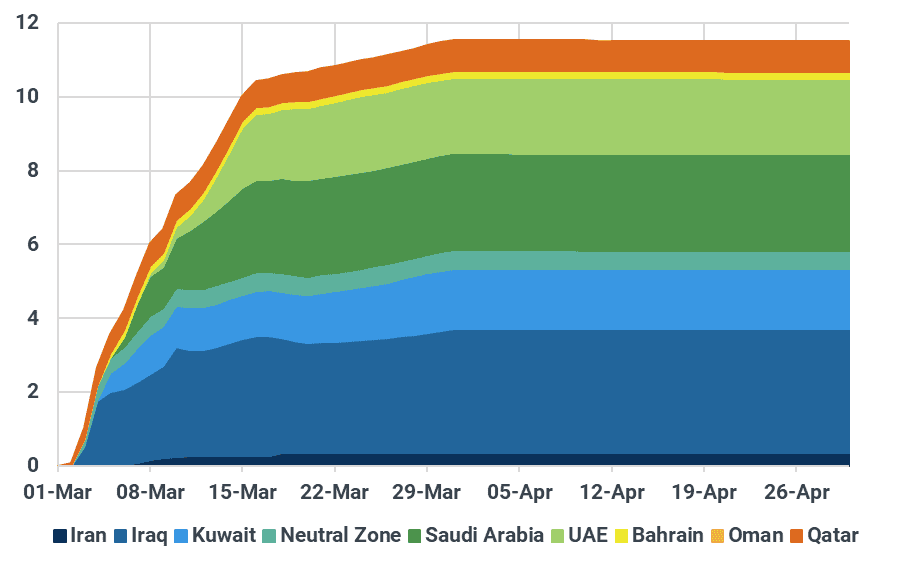

By 5 March, we estimate regional output had fallen by 3.6 mbd. By 10 March, this had jumped to 7.3 mbd. By 20 March, supply disruptions reached 10.7 mbd. These could rise to as much as 11.5 mbd by late March and remain at that level throughout April if the situation in the Strait of Hormuz does not improve.

Middle East oil production cuts by country, mbd

Source: Kpler

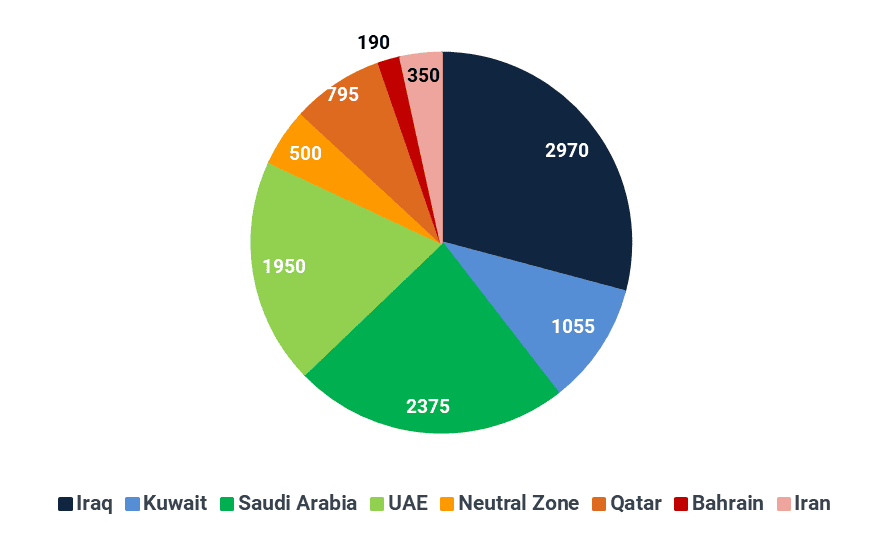

At peak, we believe production cuts will reach the following levels:

- Iran: 350 kbd

- Iraq: 3.3 mbd

- Kuwait: 1.64 mbd

- Saudi-Kuwaiti Neutral Zone: 500 kbd

- Saudi Arabia: 2.6 mbd

- UAE: 2.05 mbd

- Bahrain: 190 kbd

- Qatar: 830 kbd

Current production losses (20 March), kbd

Source: Kpler

These production cuts are not only driven by export constraints. Several regional refineries have also been impacted by missile and drone attacks, reducing refining activity. Aramco’s 550 kbd Ras Tanura and 400 kbd Samref refineries were recently hit, while Adnoc’s 922 kbd Ruwais and Bapco’s 400 kbd Sitra facilities have also been affected.

At the same time, domestic demand for transportation fuels has weakened, particularly in Iran, where travel and industrial activity have collapsed. Four phases of NIOC’s South Pars gas processing plants (Phases 3, 4, 5 and 6) have been offline since the 18 March attacks, reducing condensate output by around 100 kbd. Overall, we estimate regional refinery runs have declined by 2.5 mbd so far.

The scale of the disruption has pushed oil prices significantly higher, with ICE Brent front-month now hovering around $110/bbl, up from $72/bbl before the war. Physical prices in Asia are already above $150/bbl for Oman-Dubai. However, a range of mitigating measures, including the IEA’s record 400 mmbbl release from storage, the temporary lifting of sanctions on Russian oil, the suspension of the Jones Act, and the potential easing of sanctions on Iranian oil, have so far prevented Brent and WTI from reaching historical highs.

It may only be a matter of time. The cumulative loss of barrels cannot be fully offset by these measures. While helpful, they remain short-term fixes. Even if deployed immediately, the 400 mmbbl SPR release would only cover around 45 days of lost supply. In reality, releases will be spread over time, at a maximum rate of around 2.5 mbd.

Russia currently holds around 130 mbbls of crude on the water, although most of these volumes are already committed to Chinese and Indian buyers. Iran holds an additional 170 mmbbls on the water, largely unsold. In theory, these could cover roughly 16–17 days of disruptions, but the measure efficiency remains uncertain, as NIOC is unlikely to release volumes if it cannot access the proceeds.

So far, we estimate that the market has lost a cumulative 133 mbbls. If the situation does not improve, cumulative losses will reach 256 mbbls by the end of March close to the IEA’s crude release of 260 mbbls (with the remainder of the 400 mbbls consisting of products).

Cumulative losses are set to reach 400 mmbbls by 13 April, and approximately 600 mmbbls by the end of April. This timeline suggests that, in an ideal scenario, the US and Israel would need to end the conflict by early to mid-April. Even then, additional short-term measures would likely be required to prevent further price escalation.

Cumulative production losses by country, mbbls

Source: Kpler

Market insights you can actually trust

Kpler delivers unbiased, expert-driven intelligence that helps you to track critical market developments for your own analysis. Our precise forecasting empowers smarter trading and risk management decisions. In times of conflict and geopolitical uncertainty, our real-time data keeps you ahead of supply disruptions and price volatility.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler