Sustained Mideast Gulf fertiliser disruption concerns US corn yield potential

Vessels laden with fertiliser product in the Mideast Gulf remain hesitant to transit the Strait of Hormuz, with the last vessel to exit the Gulf occurring on 22 March. As a result, the number of laden vessels has risen to highs not seen for at least the past seven years. As the supply of fertiliser on the global market tightens, this has resulted in price rationing. Some US corn growers are expected to reduce their fertiliser application, though this may come at the expense of yield potential.

Fertiliser loading momentum has stalled

Since 28 Feb, select fertiliser terminals across the Mideast Gulf have continued to load urea, sulphur, and phosphates onto vessels, at a significantly reduced rate compared to previous years. However, the loaded vessels are still in the Gulf, unable to leave. Continuous restrictions on Strait of Hormuz transits and persistent threats to critical infrastructure have disrupted major fertiliser operations, with the geopolitical landscape shifting rapidly in recent weeks.

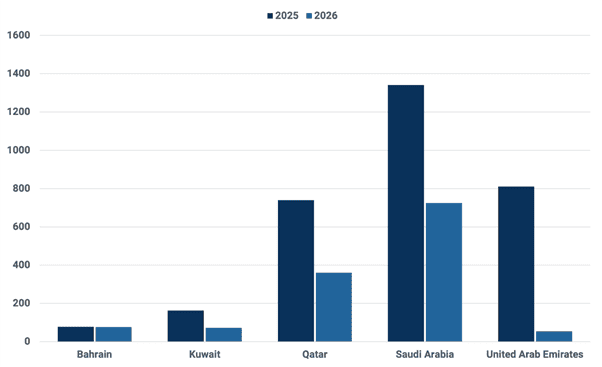

Fertiliser loadings across the Mideast Gulf for March (kt)

Source: Kpler

Mideast Gulf fertiliser activity has become increasingly restrictive. No ballast vessels have entered the Gulf with the sole purpose of loading fertilisers. All loadings during this period have been carried out by vessels that were already within the region. In the UAE, urea export activity was suspended entirely at the onset of the conflict. While UAE’s sulphur loadings only resumed in late March, activity remains minimal, with only two vessels having loaded to date.

Saudi Arabia’s Jubail industrial complex, one of the Gulf’s most prominent fertiliser export hubs for sulphur and urea, was struck on the night of Monday, 6 April. Jubail operations remained relatively consistent through the earlier weeks of disruption, but it has not received new vessels since the day after the strike. Overall, Mideast Gulf fertiliser loadings seem to have stalled entirely since early April.

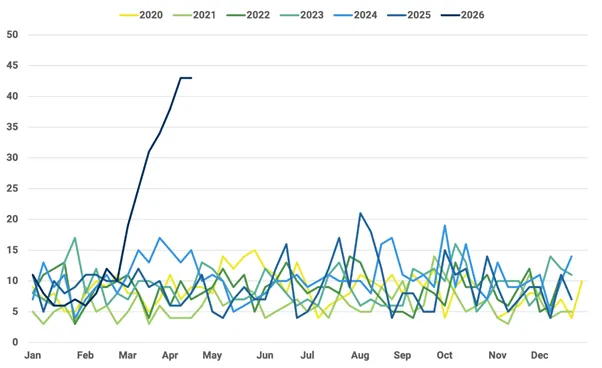

Fertiliser-laden vessels in the Mideast Gulf (count)

Source: Kpler

United States blockade adds further uncertainty

Earlier this week, the US established a naval blockade targeting “vessels of all nations entering or departing Iranian ports and coastal areas, including all Iranian ports on the Arabian Gulf and Gulf of Oman” as stated by the U.S. Central Command. The blockade shall not interfere with the navigation of vessels sailing to and from non-Iranian ports. While the blockade was formed to hinder Iranian trade, it is still uncertain if any of the other fertiliser-laden vessels will attempt to cross the Strait of Hormuz. Three of the four dry bulk carriers that have crossed the Strait of Hormuz this week were either delivering grains or had just discharged grains at Bandar Imam Khomeini, Iran. The crossings succeeded, but the precise location of the American blockade remains unclear.

Global supply tightening beyond the Gulf

The disruptions in the Mideast Gulf are sending shockwaves throughout the global fertiliser market, prompting major producers to prioritise domestic supply over international trade. China placed restrictions on urea, phosphates, and certain nitrogen-potassium blends, and has banned sulphuric acid exports entirely. Ammonium sulphate exports are the only exceptions. Russia has also restricted exports of ammonium nitrates and sulphur.

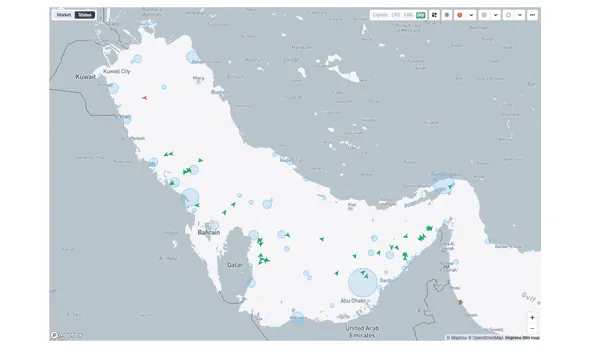

Mideast Gulf Fertiliser Vessel Update

As on 15 April, 44 vessels in the Mideast Gulf are loading or are loaded with fertilisers, for a total volume of 2,091 kt. The breakdown is as follows:

- 1,024 kt of urea

- 608 kt of sulphur

- 404 kt of phosphates (MAP/DAP) + complex fertilisers (NPK)

- 55 kt of fertilisers (grade of cargo TBD)

The last fertiliser-laden vessel to exit the Gulf and cross the Strait of Hormuz was Nadab on 22 March. The vessel is carrying Iranian urea to Yangon, Myanmar.

The vessel Prix, loaded with urea from Jubail, sailed to the Strait of Hormuz area on 9 April and is currently situated between the islands of Hormuz and Qeshm, but is still yet to exit.

Vessels loaded or expected to load fertiliser product (as on 15 Apr)

Source: Kpler

Fertiliser market continues to rise higher

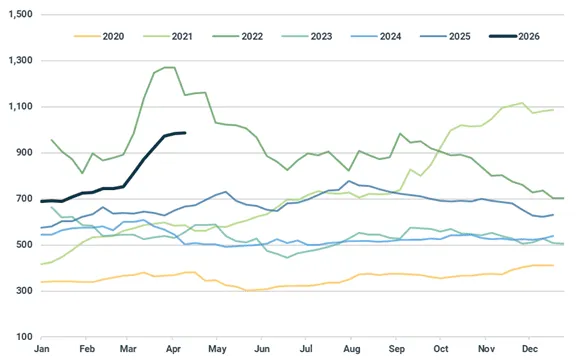

As the restricted movement of fertiliser via the Strait of Hormuz leads to wider supply-tightening measures across the world, the fertiliser market has risen to prices not seen since 2022.

North America Fertiliser Price Index (7 Jan 2002 = 100)

Source: Green Markets

However, cereal prices in 2025 are far from the elevated price levels seen in 2022 which had been caused by a relatively tighter global balance in 2021 and then the outbreak of war in Ukraine. So, globally, farmers are facing higher input costs for cereal production without a comparable increase in crop value which may support the bottom line. Therefore, something must give.

Prices paid index for feed grains and nitrogen fertiliser in the US (2011 = 100)

Source: USDA

US corn growers assess spring planting options

In the US, a survey conducted by the National Corn Growers Association (NGCA) around the end of March showed that 63% of farmers have already purchased at least 80% of their total nitrogen fertiliser needs for 2026, with only 9% of farmers without any cover.

So, as the majority of growers have covered most of their fertiliser needs, this has reduced the substitution of corn acres for alternative row crops. For example, a switch to soybeans would have likely seen the spend on nitrogen fertiliser an unnecessary expenditure at a time when margins are already narrow and cash flow is consequently under pressure. Hence, 80% of growers have kept with their initial planting decisions despite the war in the Middle East.

The survey also reported that 50% of farmers do not anticipate applying the full amount of fertiliser as planned; of which 96% attributed this to either price or availability concerns.

This would align with results when calculating the most economical application of nitrogen fertiliser for yield potential maximisation. For Illinois, the second-largest corn-producing state in the US, the recent hike in urea prices may reduce maximum corn yield potential to 96%. Should urea prices reach the same record peak in April 2022, this could see maximum yield potential drop a further percentage point, to 95%. In comparison, for this time last year, maximum yield potential was 98% as despite the USDA forecasting the same cash price at the time, the price of urea was notably lower.

Maximising corn yield with economical urea application for central Illinois

*Maximum return to nitrogen (N), the rate at which economic return for N application is maximised

Source: Corn Nitrogen Rate Calculator, USDA, DTN

US corn yield uncertainty offers market upside potential

If the 2026 US corn yield was to drop 5% from its current trend line of 183.0 bu/ac, and the percentage of planted area harvested was similar to the recent average, this would see nearly 800 mbu of production lost and 2026/27 ending stocks drop sharply below 2,000 mbu.

It should also be noted that unfavourable weather conditions would further tighten supply in 2026/27. Though, on the contrary, favourable production can lift yield potential above the trend line like last year, therefore potentially counteracting reduced nitrogen fertiliser application.

Looking ahead, the price of urea and corn will be closely monitored by US corn growers. While US corn fundamentals appear burdensome at present, aggressively high input costs are factoring into the feedback mechanism that influences growers’ decisions which could see a tightening of supply.

See why the most successful traders and shipping experts use Kpler

.jpg)