The new geopolitics of refining

The conflict with Iran has exposed a critical gap in traditional energy security strategy, demonstrating that refining capacity—not crude supply—has become the more immediate geopolitical vulnerability. While crude markets have largely stabilized, constrained refined product markets leave gasoline prices vulnerable and challenge long-held assumptions about energy resilience.

The New Geopolitics of Refining

For decades, energy security has centered on crude oil. Governments built large strategic petroleum reserves for crude, protected critical shipping lanes, and focused diplomacy on keeping oil flowing to global markets. Five months into the conflict with Iran, the market is pointing to a different reality. The world's greatest energy vulnerability is no longer simply producing enough crude oil—it is maintaining enough refining capacity to turn that crude into gasoline, diesel, and jet fuel.

Markets have repeatedly been told the war is over, a deal is imminent, or diplomacy is back on track. Yet despite the rhetoric, tanker traffic through the Strait of Hormuz remains only a fraction of what it was before February. The recent return to hostilities underscores why shipowners never fully regained confidence in the route.

The decline in crude prices has reinforced the perception that the energy crisis has largely passed. That interpretation risks focusing on the wrong indicator. Crude markets have adjusted far more quickly than refined product markets, suggesting that the strategic bottleneck has shifted downstream.

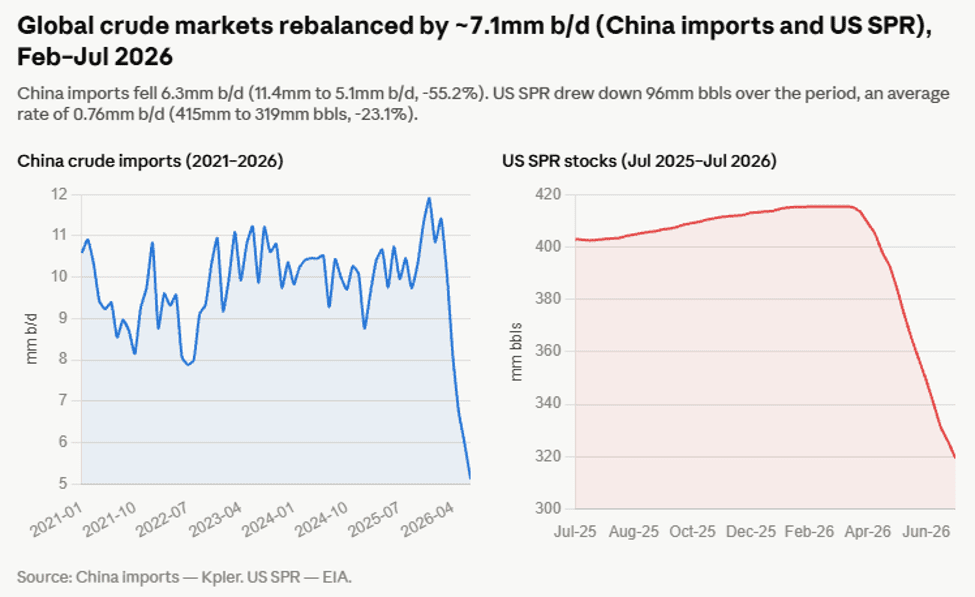

The memorandum of understanding (MOU) removed much of the geopolitical risk premium and pushed crude prices back toward pre-war levels. In reality, however, the crude market had already begun rebalancing before the ink on the agreement was dry. China's decision to sharply reduce crude imports effectively returned millions of barrels per day to the global market. Releases from the US Strategic Petroleum Reserve added further supply. Together, those developments restored more than 7 million barrels per day to the global balance and largely resolved the crude shortage.

While crude found relief through weaker Chinese buying and strategic government stock releases, gasoline, diesel, and gasoil faced a very different reality. Rather than gaining supply, the global market lost refining capacity. Repeated Ukrainian drone strikes have significantly reduced Russian refinery operations, while conflict-related disruptions across the Middle East have constrained another important source of refined product exports. Higher prices have tempered demand, but not enough to offset those supply losses.

The mismatch between crude and refined products exposes a gap in today's energy security framework. Governments have spent decades preparing for disruptions to crude oil supplies, yet they have far fewer tools available when the constraint is refining capacity. The geopolitical risk has not disappeared; it has migrated from crude supply to the refining system. Crude prices dominate headlines and shape perceptions of energy security. Meanwhile, stresses in refined product markets build quietly until they emerge as higher gasoline and diesel prices. By the time those pressures become politically visible, governments have far fewer options available to respond.

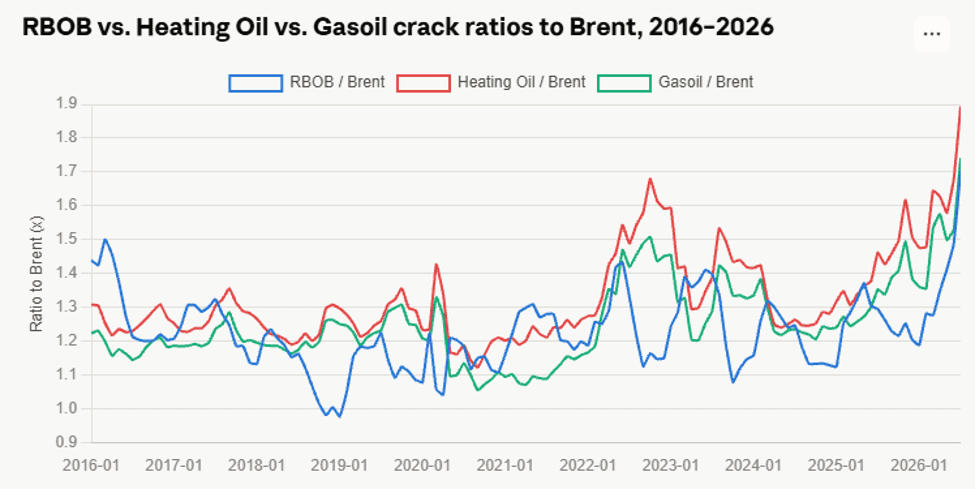

Financial markets are already reflecting that shift. RBOB, heating oil, and gasoil continue to trade at historically large premiums to Brent crude. They suggest that the scarcity is no longer crude oil itself, but the capacity to transform it into usable fuels. In other words, markets are signaling that refining—not crude production—has become today's strategic bottleneck.

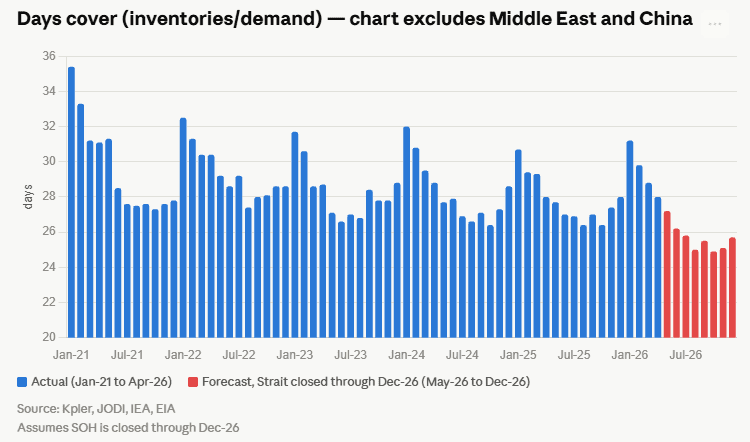

Inventories tell the same story.

To test whether reopening the Strait of Hormuz would materially improve the outlook, I modeled global gasoline days cover under a range of reopening scenarios. Even if the Strait reopened immediately, inventories recover only marginally. Across every scenario—including an immediate reopening—global gasoline inventories remain historically tight through year-end. Days cover hovers near 25 days of demand. Reopening the Strait helps restore crude flows, but it does little to rebuild refined product inventories.

Restoring transit through Hormuz will increase crude availability, but it will not immediately restore refined product supplies. One reason is Russia. With approximately 6.7 million barrels per day of refining capacity, it is one of the world's largest producers and exporters of refined products. Repeated Ukrainian drone strikes have disrupted nearly half of that capacity, forcing Moscow to periodically restrict product exports to protect domestic supply. The shortages have become severe enough to produce queues at Russian filling stations despite Russia's status as a major exporter of petroleum products.

The Middle East presents a different challenge. Even after security conditions improve, product exports are unlikely to return to normal overnight. Repositioning tankers, rebuilding export programs, replenishing inventories, and re-establishing confidence in Strait transit will all take time. The gradual recovery in Middle Eastern product exports will take time. Combined with the loss of Russian refining capacity, the global market is likely to remain structurally short of refined products long after crude supply begins to normalize.

The United States is unlikely to remain insulated from those pressures.

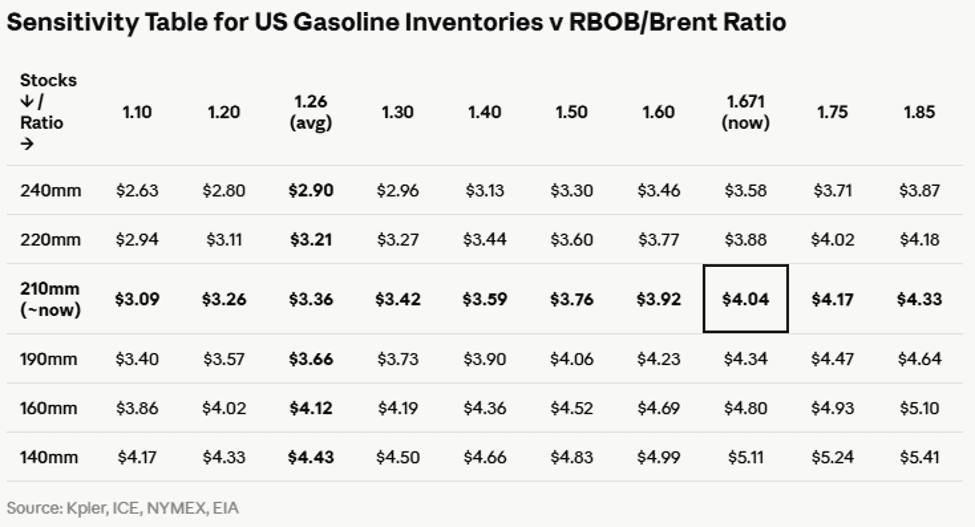

Today's national average gasoline price of roughly $3.80 per gallon reflects lower crude prices, not an easing in gasoline market fundamentals. US gasoline inventories remain near 210 million barrels, days cover continues to sit near historically low levels, and the RBOB-to-Brent ratio remains well above normal. Historically, inventories this tight and RBOB-to-Brent ratios this elevated have been associated with materially higher retail gasoline prices. If inventories continue tightening through the remainder of the summer, a return to more than $4 per gallon remains entirely plausible—even without another major rally in crude oil.

The broader lesson extends well beyond this summer's gasoline prices. The conflict has shown that repairing the energy system is likely to take far longer than restoring crude flows. Reopening shipping lanes is only the first step; rebuilding refined product supply requires functioning refineries, export infrastructure, and the confidence to move fuels back into global markets. As governments reassess energy security after this conflict, resilience will depend not only on protecting oil supply, but on ensuring that the world's refining system can withstand geopolitical shocks.

See why the most successful traders and shipping experts use Kpler