The WTI-Brent blowout: war risks meet the export ban threat

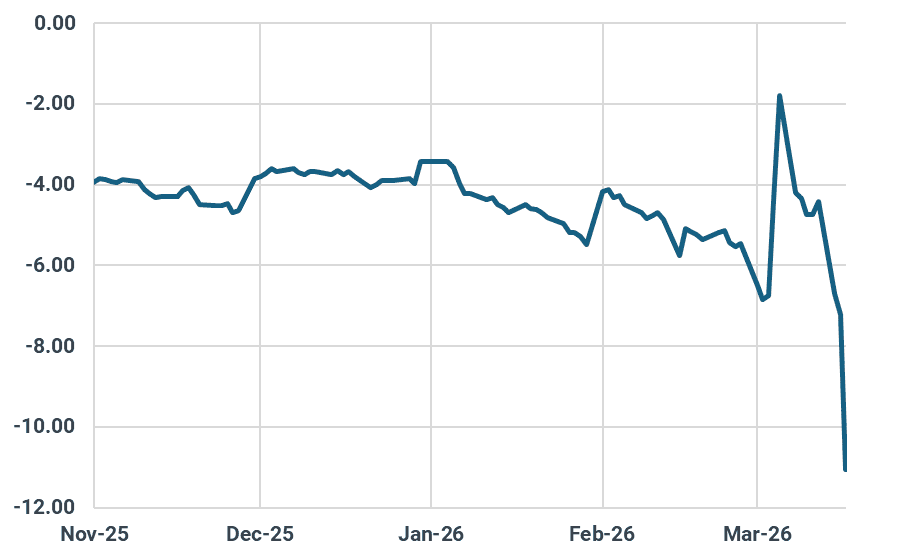

The global crude market is fracturing. The spread between the international Brent benchmark and US West Texas Intermediate (WTI) has blown out to approximately $10/bbl, double its typical $2-$5 range.

Key takeaways

- The Brent-WTI spread has widened dramatically to roughly $10/bbl as the global benchmark absorbs severe Middle Eastern supply risks while WTI remains insulated by domestic dynamics.

- The Trump administration’s suspension of the Jones Act for PADD 5 (West Coast) and staggered use of other policy tools has raised the topic of a full US crude and product export ban (though this has been denied).

- An export ban would trap roughly 4 Mbd of US crude (predominantly light-sweet shale) domestically. US refineries (average API 33) cannot efficiently process this volume of ultra-light crude (API 40+), leading to rapid storage exhaustion and forced shut-ins.

This divergence is the direct result of Brent being the globally-traded and liquid benchmark, absorbing the increasing disruptive effects in the crude markets. These include the growing production shut-ins in the Middle East on a daily basis, a new frontier of attacks on upstream assets, as well as the growing threat of attacks in the by Iran (or proxies) in the Red Sea (effectively blocking off the world’s smaller escape route for barrels).

At the same time, the US domestic crude system remains comparatively insulated. However, this pricing dynamic is being heavily influenced by escalating rumours regarding a potential US export ban. That being said, it was reported today that the White House has informed executives that there would be no ban.

Prompt-month WTI-Brent futures spread, $/bbl

Source: ICE, Nymex

Such a ban would not just directly move WTI. It would break its link to the global pricing as WTI Midland sits inside the Dated Brent basket. While WTI would clear locally, Dated Brent would lose a key flexible barrel and would tighten considerably, not to mention what price assessors would do to mitigate the effect of the lost assessment barrels.

It is very possible that the White House is using an export ban threat to strong arm European & Asian allies into joining a military effort to secure the Strait of Hormuz, as could be evidenced by statements coming out today from European nations claiming they will help vessel transits.

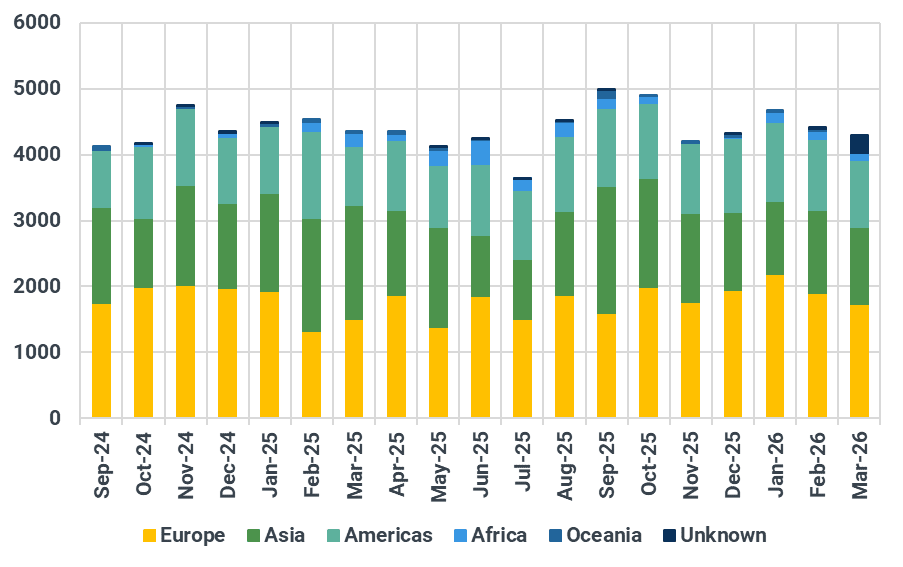

Globally, the implications would be catastrophic. A ban would remove over 11 Mbd US crude and products from the market, considerably amplifying the current Strait of Hormuz outage. Europe (which relies on ~1.8 Mbd of US crude) and Asia (~1.6 Mbd) would face immediate physical shortages.

US crude and condensate exports by destination continent, kbd

Source: Kpler

The US exports roughly 4 Mbd of crude, the vast majority of which is ultra-light sweet shale oil (API gravity 40+). Conversely, the US refining system is highly complex, optimized to run heavier, sour grades (average API 33). US coking refineries, particularly on the Gulf Coast, are currently capturing extraordinary margins of above $25/bbl running medium sour grades like Mars. There is no technical or economic incentive for them to suddenly switch to processing millions of barrels of trapped ultra-light shale crude.

Because domestic refiners cannot absorb this trapped light sweet crude, inventories would violently swell. An export ban trapping would push US storage to "tank top" by mid-April or early May. This would crush WTI prices locally, forcing massive, chaotic shut-ins across the US shale patch.

Market insights you can actually trust

Kpler delivers unbiased, expert-driven intelligence that helps you to track critical market developments for your own analysis. Our precise forecasting empowers smarter trading and risk management decisions. In times of conflict and geopolitical uncertainty, our real-time data keeps you ahead of supply disruptions and price volatility.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler