US blockade: Iran starts feeling the heat

The US blockade is beginning to materially disrupt Iran’s oil flows, with loadings collapsing and storage filling rapidly. While the immediate revenue impact is limited, operational constraints are now forcing production cuts and setting up a delayed but significant financial squeeze.

Key Takeaways

- Iran exports remained resilient pre-blockade, averaging 1.85 mbd in March, above 1.7 mbd prior trend.

- No confirmed tanker has exited the US blockade zone.

- Loadings dropped sharply to 567 kbd post-blockade.

- Usable storage stands at ~26 mbbls (~14 days), rising to ~22 days including floating storage. Assuming not all storage tanks can be used, usable storage drops to just ~12 days including floating storage.

- Production cuts are underway, with cuts seen to rise as much as 1.5 mbd by mid-May, but the monthly decrease should average

- Iran's revenue impact is delayed but significant at $200–250m/day.

How much oil was Iran exporting before the US blockade?

Up until the blockade, Iran’s oil exports were largely unaffected by the war as the IRGC controlled the Strait of Hormuz. Naturally, vessels carrying Iranian oil were allowed to pass. As a result, Iran’s oil shipments averaged 1.85 mbd in March, above the 1.7 mbd seen in the previous three months.

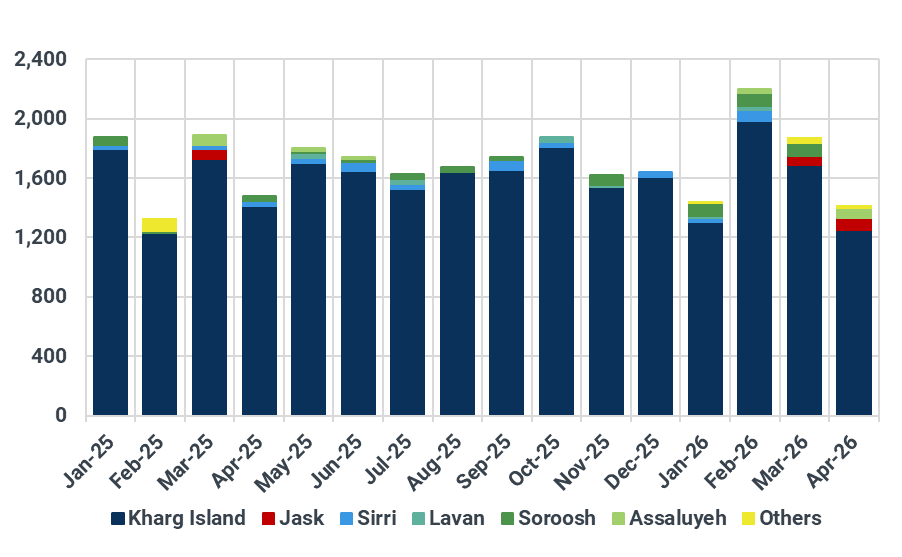

Iran oil exports by origin ports, kbd

Source: Kpler

Has Iran managed to pass oil through the blockade?

Despite claims that 31 tankers escaped the blockade zone, we have not observed any vessels successfully transiting it. Several tankers passed through the Strait of Hormuz but failed to clear the US blockade, which sits further south between the Gulf of Oman and the Arabian Sea. Most vessels instead diverted toward the Chabahar area in southeastern Iran.

What is the impact on Iran’s oil loadings? Is there any ballast capacity left?

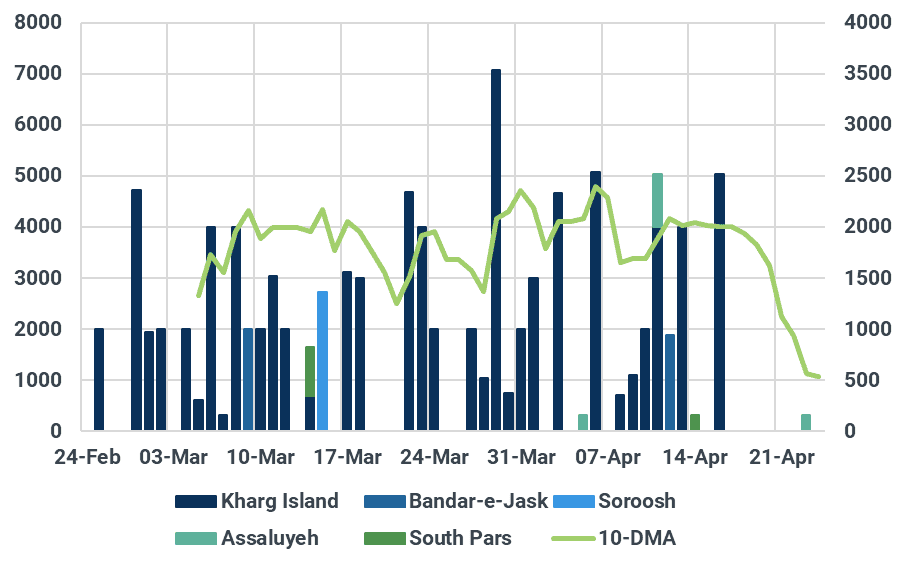

The blockade has already reduced loadings due to limited ballast availability. Crude and condensate loadings averaged 2.1 mbd between 1–13 April, but only five cargoes have been observed since, three at Kharg and two at Assaluyeh, bringing the average down to 567 kbd between 14–23 April.

There are still 7 VLCCs and 2 Aframaxes in the Persian Gulf with a history of lifting Iranian crude, representing 15.4 mbbls of potential near-term liftings. However, activity will remain constrained beyond that.

Iran daily crude and condensate by ports, kbd

Source: Kpler

How much onshore storage space is left?

Since the blockade, Iran’s oil inventories have built by 4.6 mbbls (~500 kbd), bringing total onshore stocks to 49 mbbls. We assess total storage capacity at 86 mbbls. However, our coverage currently is missing a few storage tanks located in northern oil refineries including the Tehran, Tabriz and Esfahan refineries. Accounting for these refineries would likely take total onshore storage capacity up to 90-95 mbbls. Assuming total capacity of 90 mbbls, NIOC currently has ~41 mbbls of unfilled storage capacity. This is equivalent to ~22 days of production.

However, several constraints reduce usable capacity. Firstly, not all tanks can be filled at 100% due to operational constraints and possible technical limitations. Secondly, some storage tanks are not accessible due to geography or the nature of the product:

- Tanks at Sirri and Lavan (~4.7 mbbls) are not accessible for onshore crude.

- Assaluyeh (~8.6 mbbls) is dedicated to condensate storage from the South Pars gas field.

- Parts of the Bandar Abbas site (~1.6 mbbls spare) are tied to the Persian Gulf Start condensate refinery and are not usable for crude.

As a result, 14.9 mbbls is effectively unusable, leaving ~26 mbbls of usable storage, equivalent to ~14 days of exports. Including 15.4 mbbls of available floating storage, total available capacity rises to ~41 mbbls (~22 days). Nonetheless, Iranian onshore storage is unlikely to exceed 80% utilisation, consistent with historical patterns. This indicates onshore spare storage capacity is closer to ~8-10 mbbls rather than 26 mbbls. In that case, this is only equivalent to around ~12 days of normal export volumes.

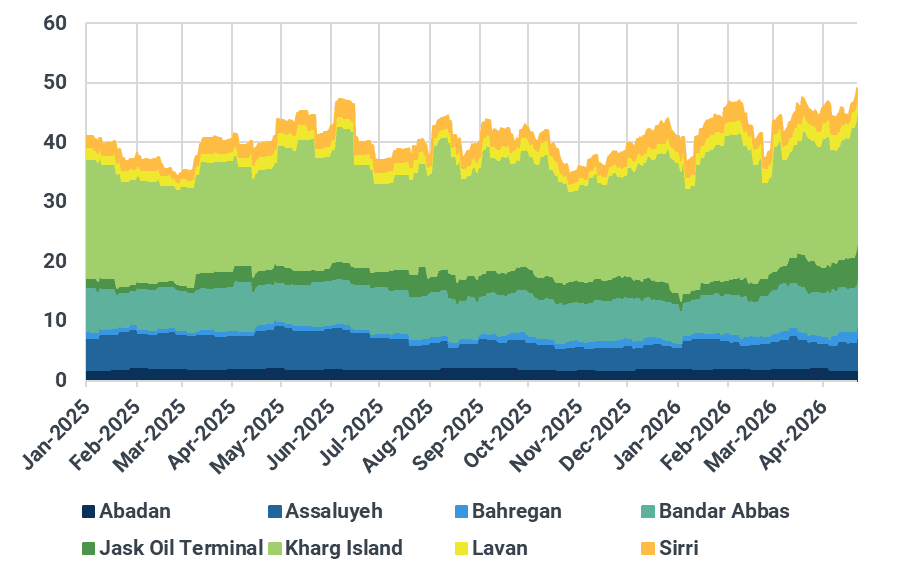

Iran oil inventories, mbbls

Source: Kpler

What happens to Iran’s oil production?

With limited ability to load crude, NIOC has begun reducing output. As seen in other regional producers earlier in March, cuts begin before storage reaches full capacity.

We estimate crude production will fall from 2.75 mbd to 1.2–1.3 mbd by mid-May if the blockade holds. Condensate output is unlikely to be impacted given strong domestic consumption. If the blockade is lifted by late May, production should recover quickly given NIOC’s strong experience in managing wellhead production flows.

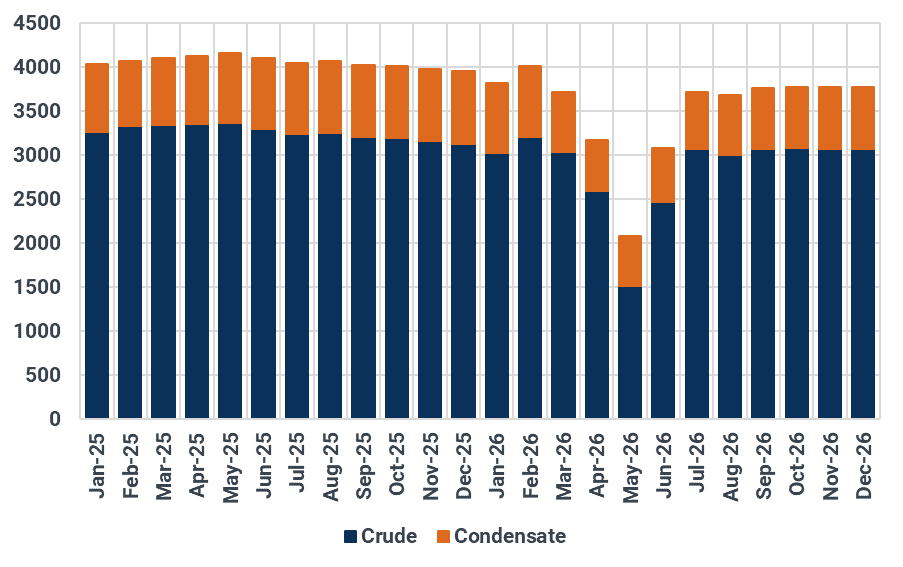

Iran oil production, kbd

Source: Kpler

Does this affect Iran’s oil revenues? How much oil is on water?

The blockade doesn’t impact Iran’s immediate revenues. It usually takes around two months for an oil cargo to reach northeastern China from Kharg Island. The Chinese buyer then has a two-month period to pay the Iranian counterparty, whether that is NIOC or a middleman.

Iran also holds 184 mbbls of oil on water currently, of which 60 mbbls are in the Persian Gulf and the Gulf of Oman and are therefore stuck. The remaining 124 mbbls are mainly around Singapore and close to China, although the US seized at least four tankers recently.

Despite the temporary sanctions waiver (which expired by now), China’s oil imports from Iran didn’t jump, highlighting Chinese teapots’ weak margins and the difficulty to offload Iranian crude. Therefore, not all the 124 mbbls are easily monetisable.

As a result, the blockade would only impact Iran’s oil revenues 3-4 months from now, limiting its effectiveness. Once this is the case, the blockade would reduce Iran’s oil revenues (including petroleum products and LPG) by around $200-250m per day at current prices.

However, the blockade more than symbolically pressures Iran. Curtailing production comes with higher opex. Iran is also a major grain, corn and rice importer. Lower imports of these agricultural products will drive higher inflation internally. Iran reportedly imports around $200-250m of mainly agricultural products daily too.

It is also unclear whether Iran is able to access its revenues in full. A major portion of the oil revenue flow used to pass through the UAE banking system, and the UAE may have become less complacent regarding these transfers, as highlighted by Treasury Secretary Scott Bessent recently.

Iran oil on water by location, mbbls

Source: Kpler

Will this strategy force Iran back to negotiations?

So far, the US blockade appears very efficient. No vessel carrying Iranian oil was able to escape from it. Although the blockade doesn’t choke Iran financially in the immediate term, it comes with the promise of doing so down the line if it is maintained. The fact that Tehran has asked for the blockade to be lifted as a condition to resume negotiating highlights that it is hurting where it hurts.

The blockade has apparently succeeded in bringing Iranian negotiators back to the negotiating table, with a meeting likely over this weekend as per latest press reports. However, key hurdles remain. Each side believes it holds the upper hand and doesn’t want to blink first. The upcoming meeting will matter in showing that Iranian negotiators actually have the backing of people who matter in Tehran (IRGC Commander Ahmad Vahidi and Supreme National Security Council Secretary Mohammad Bagher Zolghadr). Once this hurdle is passed, the hardest part remains for both sides negotiators.

See why the most successful traders and shipping experts use Kpler