US–Iran 60-day deal will bring temporary relief to Hormuz vessel backlog, while OFAC’s General License X remains conditional

The US–Iran MoU and OFAC General License X mark a real de-escalation signal for shipping, cargo risk and compliance workflows, but not a return to pre-crisis trade. GL X authorizes covered transactions involving Iranian-origin crude oil, petrochemical products and petroleum products through 12:01 am EDT on 21 August 2026, including certain transactions involving blocked vessels where ordinarily incident and necessary to the covered trade. The relief is time-bound, activity-scoped and revocable; it does not delist vessels or counterparties, and it does not resolve broader financial sanctions, tolling risk or later-stage nuclear and UN-related implementation.

Market & trading calls:

- Vessel backlog first, new supply later: Early increases in Hormuz transits and loadings likely reflect delayed vessel activity clearing rather than fresh Iranian supply. Commercial crossings of the estimated 570-vessel backlog are assumed at a safe clearance rate of around 15 vessels per day, with upside possible if transit conditions improve.

- GL X creates a narrow authorization window: Covered Iranian-origin crude, petrochemical and petroleum transactions are authorized through 12:01 am EDT on 21 August 2026, but the license is not a full sanctions lift.

- Compliance relief remains activity-scoped: GL X may cover transactions ordinarily incident and necessary to the authorized oil trade, including certain dealings with blocked vessels, but it does not delist vessels, owners, operators or other counterparties.

- Cargo attribution should improve as the Gulf de-darkens: Lower GNSS interference and AIS spoofing should reduce the undisclosed-destination share, but shadow-fleet behavior will not disappear immediately.

- Post-60-day tolling is the next risk point: Any Iranian fee or safe-passage mechanism could introduce a sanctioned counterparty and keep legal, insurance and banking risk above pre-crisis levels.

A temporary de-risking signal, not full normalization of flows

The announced US–Iran Memorandum of Understanding (MoU) has now been implemented through OFAC’s General License X as of 21 June, which authorizes certain transactions ordinarily incident and necessary to the production, sale, delivery or offloading of Iranian-origin crude oil, petrochemical products and petroleum products through 12:01 am EDT on 21 August 2026.

The authorization also covers certain payments and vessel-related services, including insurance, where they are tied to the covered activity. Broader termination of UN-related, IAEA-related and unilateral US measures remains subject to a later phase. Markets have already reacted: crude prices have fallen to a three-month low on expectations that Iranian supply and Strait of Hormuz traffic could begin to normalize.

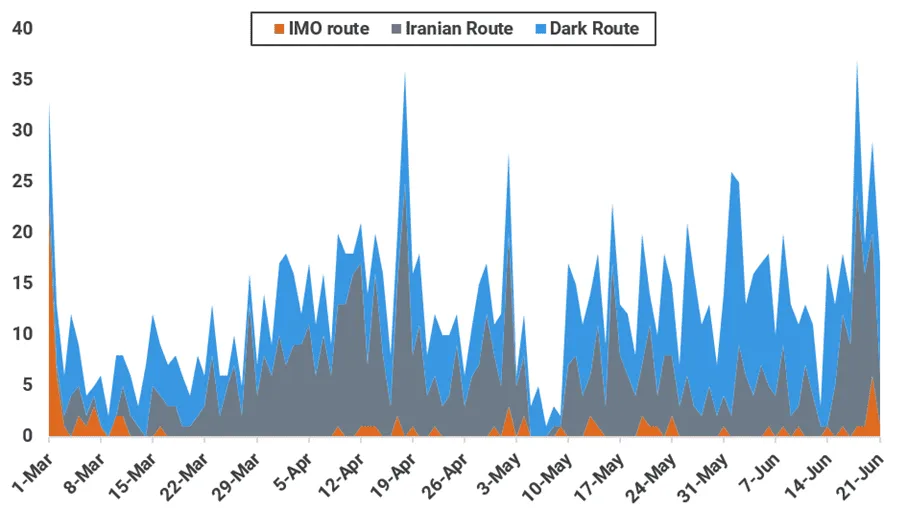

The MoU is therefore best read as a de-escalation signal for shipping and cargo risk rather than a return to normal Iran trade. Initial upticks in Strait of Hormuz transits were observed from 18 to 21 June, with 108 total crossings recorded over the period. This marks a clear increase from the previous single-digit daily crossing averages, but it should be interpreted primarily as delayed vessel activity beginning to clear rather than immediate new supply.

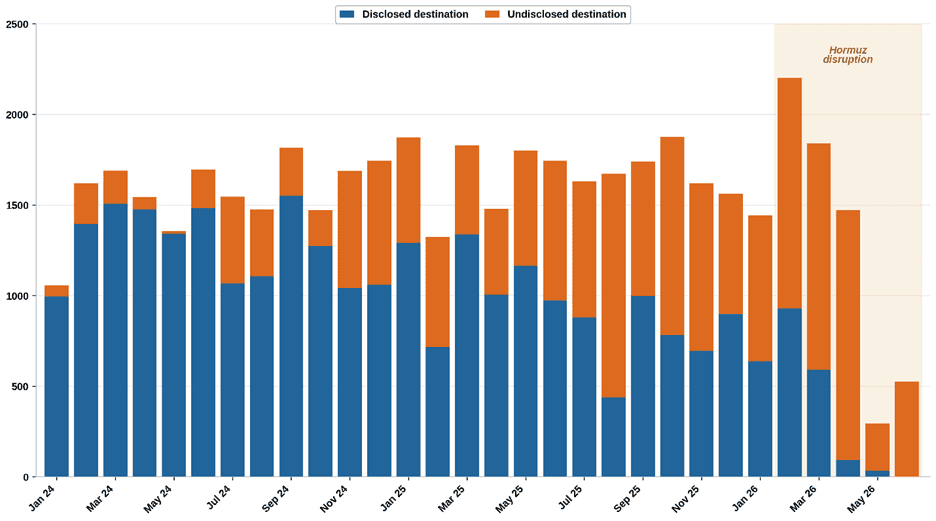

Iran has continued to move roughly 1.6–1.7 mbd of seaborne crude throughout the sanctions period before the US blockade in April, overwhelmingly crude rather than condensate or clean products. GL X does not create this trade from zero. Instead, it moves covered flows into a temporary authorized window and re-illuminates activity that never fully stopped. The immediate impact is therefore on cargo-risk treatment and voyage confidence, not necessarily on underlying production or export capacity.

Iranian seaborne crude exports by destination disclosure (kbd)

Source: Kpler. Monthly seaborne crude/condensate exports by destination; intra-Iran floating storage excluded. Recent months reflect the Strait of Hormuz disruption and are subject to retroactive revision.

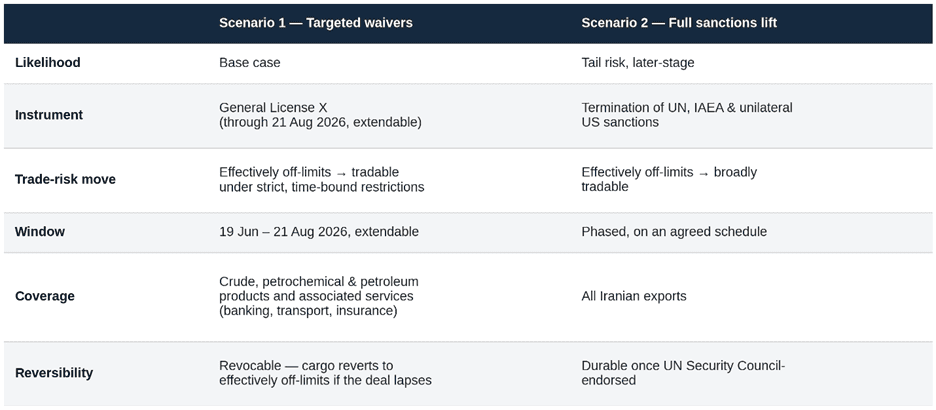

From here, two scenarios dominate the compliance outlook. The base case, now confirmed, is GL X, a temporary authorization that eases Kpler Risk & Compliance’s Iran-related trade-risk rating from effectively off-limits to tradable under strict, time-bound restrictions. Any extension would require further official action and would depend on progress in the negotiations. The second, less likely scenario is a full lifting of sanctions, which would move trade risk materially lower across Iranian exports, but only as a later-stage outcome contingent on the nuclear negotiation, an implementation mechanism and UN Security Council endorsement.

Kpler Risk & Compliance’s base case highlights that GL X is revocable, so if the agreement lapses or is contested, covered cargo can revert immediately to effectively off-limits. Any easing must stay conditional and explicitly time-bound.

The two scenarios at a glance

Source: Kpler Risk & Compliance

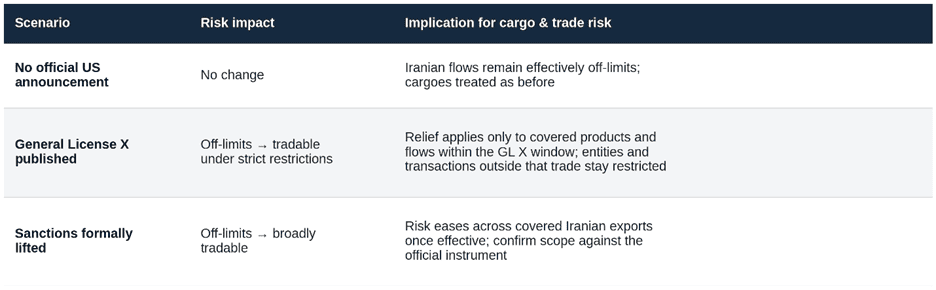

GL X is not a clean compliance reclassification for the ships carrying the cargo. It authorizes dealings involving blocked vessels only where those dealings are ordinarily incident and necessary to the covered oil, petrochemical or petroleum-products trade. It does not delist those vessels, operators or counterparties. Outside the authorized activity, tankers, operators and trading entities may remain individually sanctioned, including many of the shadow-fleet vessels behind the rising undisclosed-destination share shown above.

Covered cargoes can therefore still carry vessel- and counterparty-level exposure. Screening should remain entity-level even where the product-level treatment has eased. Because GL X is time-bound, residual secondary-sanctions exposure for non-US persons and the risk that later-stage UN-related implementation is delayed, reversed or fails to materialize both keep covered cargoes short of a clean reclassification.

Risk impact by scenario

Source: Kpler & Compliance

First 30-plus days: the backlog clears before flows can rebuild

The first visible impact is likely to be the clearing of delayed vessel activity over 30 days or more, rather than an immediate wave of new flows. Vessels that have been waiting, slow-steaming, rerouting or sitting in compliance limbo would start to move again once the agreement gives market participants enough confidence to re-enter the Strait. The MoU provides the initial mechanism: Iran is expected to arrange safe passage at no charge for 60 days, while the US removes its naval blockade within days of signing, with traffic intended to return toward pre-crisis levels within the same window.

Kpler Risk & Compliance believes this will be difficult to achieve within 30 days alone. Even if trapped vessels are prioritized and around 15 vessels transit safely per day, the 570 commercial-vessel backlog as of 22 June would imply close to 40 days of clearance before accounting for additional frictions. Ongoing mine-clearance operations, insurance checks, chartering delays, port scheduling and compliance re-screening could realistically extend the timeline further.

Full clearance could therefore realistically take six weeks or more, particularly if the removal of suspected mines from the Strait takes several weeks.

Openness does not equal pre-crisis traffic while access-fee risk remains unresolved

Even if the Strait formally reopens and covered Iranian oil flows are authorized, traffic is unlikely to snap back to pre-crisis levels without greater legal certainty. Shipowners, traders, banks, insurers and refiners still need to assess the scope of GL X, the durability of US implementation and the treatment of counterparties before fully re-engaging. The current framework authorizes covered oil-related activity but leaves broader financial sanctions, frozen-asset access and the nuclear track to a 60-day negotiation that either side may seek to extend.

The market is therefore likely to reopen faster in sentiment than in actual vessel flows. Commercial participants may wait for more clarity on implementation, while some counterparties will remain cautious because of residual sanctions, reputational exposure, insurance costs and banking risk.

A further friction sits over the Strait itself: the unresolved question of post-60-day access charges. US messaging has presented the waterway as toll-free, but the MoU only guarantees free passage for the initial 60-day window. After that, Iran has signaled that it may seek to levy fees for services such as navigation, environmental protection and maritime management rather than a formal toll. That distinction is legally contested. The Strait of Hormuz is a natural international waterway, and maritime-law specialists argue that coastal states cannot charge for passage itself, regardless of how the charge is labelled. That makes any future Iranian fee regime materially different from charges levied by man-made, service-based waterways such as the Suez or Panama canals.

For risk and compliance teams, a fee regime adds more than cost. It introduces a new counterparty. Any Iranian state body collecting charges would need to be screened for sanctions exposure before payment is made, and the payment route itself could create additional banking and compliance questions.

Alongside this, war-risk insurance premiums that rose during the blockade are likely to normalize only gradually. Until the post-60-day arrangement is defined, participants will continue to price in the prospect of recurring access fees, residual legal uncertainty and insurance risk. Effective transit costs are therefore likely to remain above pre-crisis levels even after the first wave of vessel activity resumes.

Maritime visibility should improve as GNSS interference and AIS spoofing ease

If regional tensions continue to ease, signal interference should decline, improving maritime visibility and reducing uncertainty in vessel tracking. GNSS interference is likely to fall, AIS spoofing should become less frequent, and AIS gaps among mainstream commercial operators should narrow. That would lift voyage confidence and improve cargo attribution, with early signs of better route visibility already observed since 18 June.

However, the improvement should be treated as gradual rather than immediate. High-risk actors may continue to use dark activity, spoofing or irregular AIS behavior through the transition, particularly where sanctions exposure, cargo origin or destination remain commercially sensitive.

Vessels crossed SOH by route as of June 21

Source: Kpler Risk & Compliance; full traffic data is available, including non-commercial vessel tracking from MarineTraffic.

Later-stage US sanctions lifting is possible, but contingent on the pace of negotiations

A full sanctions lift remains possible, but it belongs to a later stage rather than the base case. The MoU frames the termination of broader measures, including UN Security Council resolutions, IAEA measures and unilateral US sanctions, as occurring on an agreed schedule. That process remains contingent on the 60-day negotiation, the establishment of an implementation mechanism and eventual UN Security Council endorsement.

The signposts are concrete, including the durability of GL X, the pace of the 60-day talks: the establishment of the implementation mechanism, and progress on frozen assets and the nuclear file. Each milestone achieved would move the market closer to durable relief; each missed or delayed milestone would keep risk capped at a temporary, activity-scoped authorization level.

The agreement is therefore a trigger for preparedness, not automatic normalization. The official US instrument has confirmed the initial scope of authorized activity, but markets should remain ready to adjust quickly as extension, revocation and later-stage implementation risks evolve. The prudent reading is a de-escalation that is real, but still reversible.

See why the most successful traders and shipping experts use Kpler