US labor market resilient, but with a real wage problem

May payroll growth impressed in May, but declining real wages pose economic and political risks.

Summary

- Labor Market Resiliency Continues: The headline unemployment rate held at 4.3% in May with healthy underlying dynamics – the labor force expanded and the number of unemployed declined. Total nonfarm payrolls added +172k m/m, bringing the three-month pace to +188k, the highest level in over two years. The prime age employment ratio, reported at 80.8%, remains at the top end of the range.

- Real Wage Concerns: However, real wages likely dipped again in May as inflation surges in response to the Iran conflict. In April, real wages declined for the first time since 2023. In May, nominal wages increased 3.4% over 12 months, below the 3.8% rate of headline inflation reported in April. This dynamic could become a significant problem for the Trump administration if it persists.

- Fed Hike Increasingly Possible: Since early April we have leaned towards a one-hike bias for the Fed this year in order to keep inflation expectations well anchored. Today’s report gives little reason to believe monetary policy is overly restrictive. Our bullish USD thesis also remains intact on today’s labor market report.

Market Analysis

As the conflict with Iran runs into a fourth month, all eyes remain focused on whether the US economy can weather the storm of higher energy prices. The inflationary impacts are already being felt. In April, PCE-based headline inflation finished at a 12-month pace of 3.8%, easily marking the highest level since 2023, when the US economy was slowly exiting from Covid, and Ukraine-war induced inflationary shocks. Nonetheless, despite the recent bout of Iran uncertainty, US labor market data for May points to ongoing resiliency, albeit with some critical caveats.

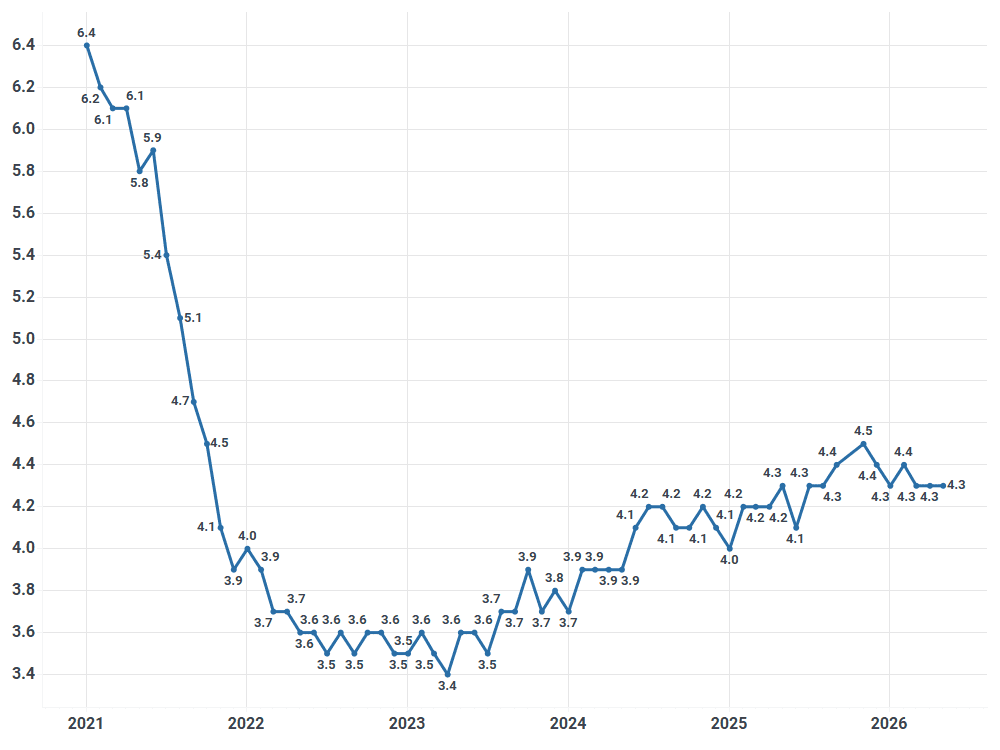

Monthly US Headline Rate of Unemployment (%)

Source: BLS

The US headline rate of unemployment (U3), measured via the Household Survey, finished May at 4.3%, in line with month earlier levels, and off the cycle high 4.5% seen in November of last year. After a clear upward trend in the unemployment rate through the second half of last year, the situation has seemingly stabilized since the start of this year, with U3 holding in a tight range between 4.3 – 4.4%. The data underlying UR was also encouraging in May with an expansion in the labor force (+83k m/m) alongside a healthy decline in the number of unemployed (-66k m/m).

The prime age portion of the US labor market, which includes those aged 25 – 54, remains healthy. In May, 80.8% of the prime age population had a job, holding at the upper end of the post-Covid range, and surpassing the peak seen in the 2010s (80.6%). The story is very different for the above-55 population, whose proportion of which are employed has declined rapidly in recent months, hitting 36% in May, down from 37% this time last year, and well off the levels approaching 39.5% in 2019.

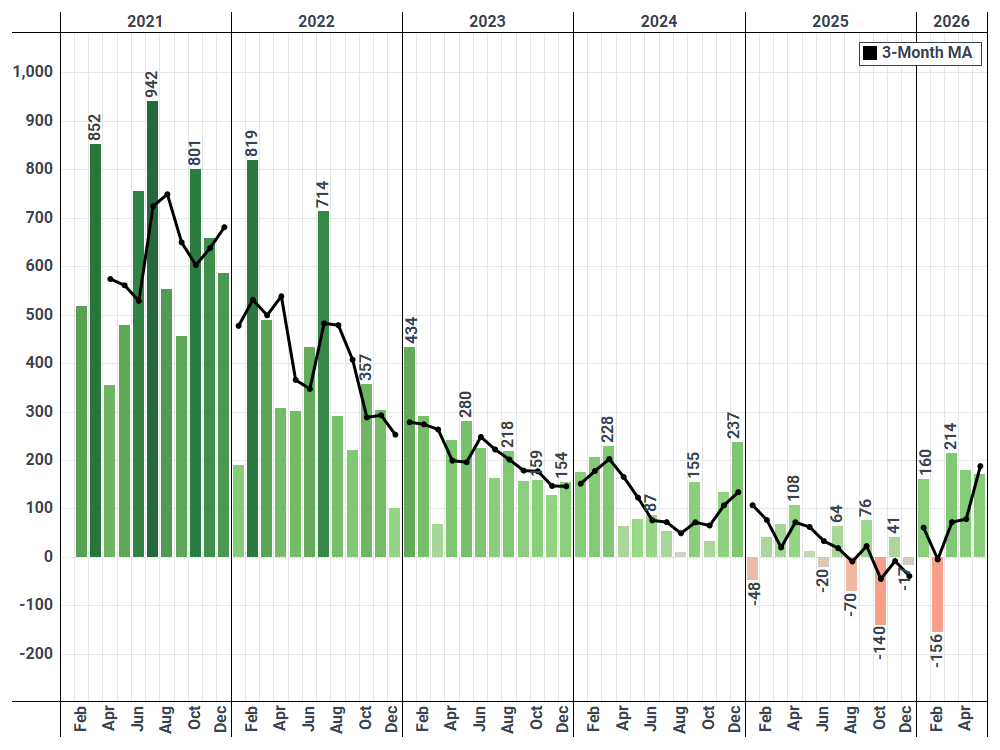

Nonfarm payrolls, measured via the Establishment Survey, also impressed in May with total payroll growth managing +172k m/m, bringing the three-month pace to an impressive +188k, easily marking the highest level in over two years. The three-month pace of private only payroll growth also looked healthy in May at +166k. These job growth figures are likely well above the breakeven pace, which we estimate is in a range closer to +25k given limited immigration levels, albeit this might need to be scaled up if the current pace of job creation continues.

Monthly Total Nonfarm Payroll Growth (M/M, in thousands)

Source: BLS

It also appears that AI capital expenditures are lifting Americas most cyclical labor sectors – manufacturing and construction. Manufacturing payroll employment growth averaged monthly declines in 2023, 2024, and 2025, but has recovered into 2026 with the three-month pace finishing May at +7k. Average monthly construction employment growth, which was flat in 2025, has also rebounded in 2026 with the three month pace of additions at +14k in May.

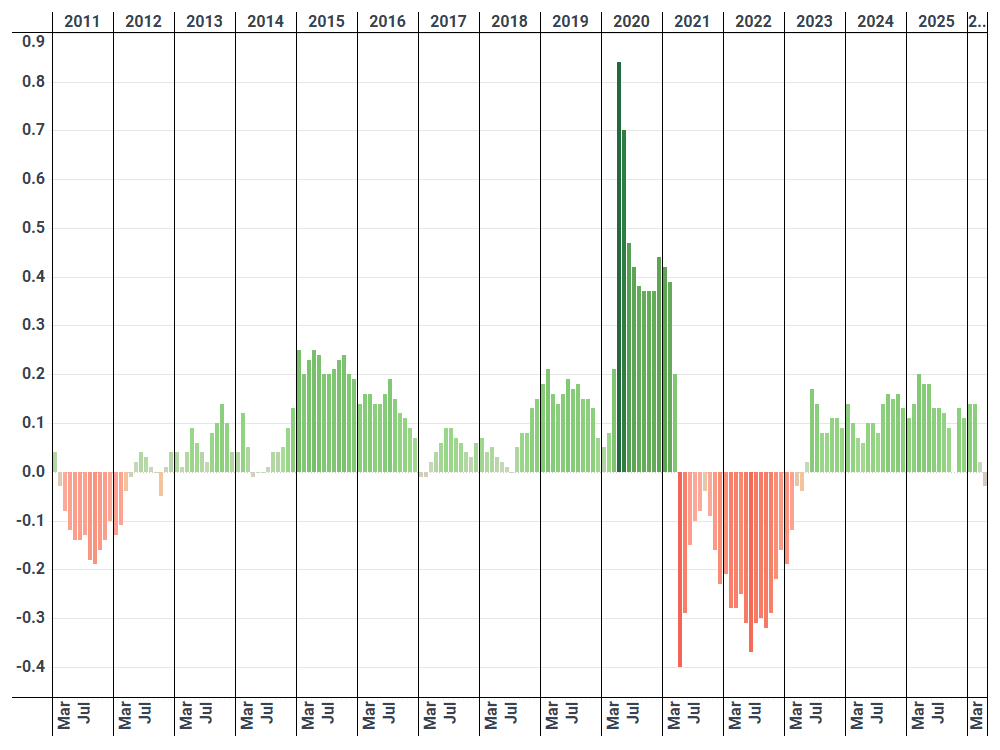

Nonetheless, despite a positive overall labor market report, we remain concerned about inflation and real wage dynamics. In April, the 12-month pace of real wage growth dipped negative for the first time since 2023. This pattern continued in May. Nominal wages only rose 3.4% over 12 months, pacing well under the 3.8% rate of headline inflation. This could become a major political problem for the Trump administration if elevated inflation levels persist. In 2022, Biden ran into the same problem after more than a year of real wage declines.

As we argued in our report on Wednesday, June 3, our view is that the Fed will hike rates once this year in order to keep inflation expectations well anchored. With the labor report today, there is little reason to believe that monetary policy is overly restrictive. Our bullish USD thesis also remains intact following today’s labor market figures.

US Real Wage Growth Over 12-Months (%)

Source: BLS; data not yet published for May

See why the most successful traders and shipping experts use Kpler