Aluminium's war premium: Middle East disruption drives supply chain shifts

War in the Middle East disrupted the aluminium market and drove prices to multi-year highs. The supply chain impacts have been far reaching. The US and Europe are competing to buy Canadian aluminium, while Asian producers look to ramp up output.

- The Gulf Cooperation Council (GCC) region is home to 8% of global primary aluminium production capacity. Interruption to raw material inputs and energy supplies, combined with direct kinetic attacks, means output is now running at around two-thirds of capacity.

- The war drove US aluminium prices to new highs however, import tariffs and competition for energy are more important drivers for the US domestic market. Competition for Canadian aluminium has increased.

- Europe has structural disadvantages in aluminium production, and war-driven price disruption favours Asian producers with lower energy costs and capacity to ramp up output.

- Supply chain impacts will continue through 2026 and into 2027.

The state of play

The GCC produced 6.16Mt of aluminium in 2025, over 80% of which was exported. Interruption to seaborne traffic through the Strait of Hormuz curtailed alumina supplies to aluminium smelters operated by Aluminium Bahrain (Alba), Emirates Global Aluminium (EGA), and Qatalum. EGA’s Al Taweelah alumina refinery lost access to seaborne bauxite imports. Producers were forced to innovate to keep raw materials flowing, using dark transits through the Strait of Hormuz, trucking material from Fujairah and Sohar, and setting up a transhipment operation in India. These pushed costs up sharply.

On 28 March, aluminium smelters operated by EGA at Al Taweelah (capacity 1.50Mtpa) and Alba (capacity 1.60Mtpa) suffered missile and drone attacks. Together, these account for nearly half of GCC aluminium production capacity.

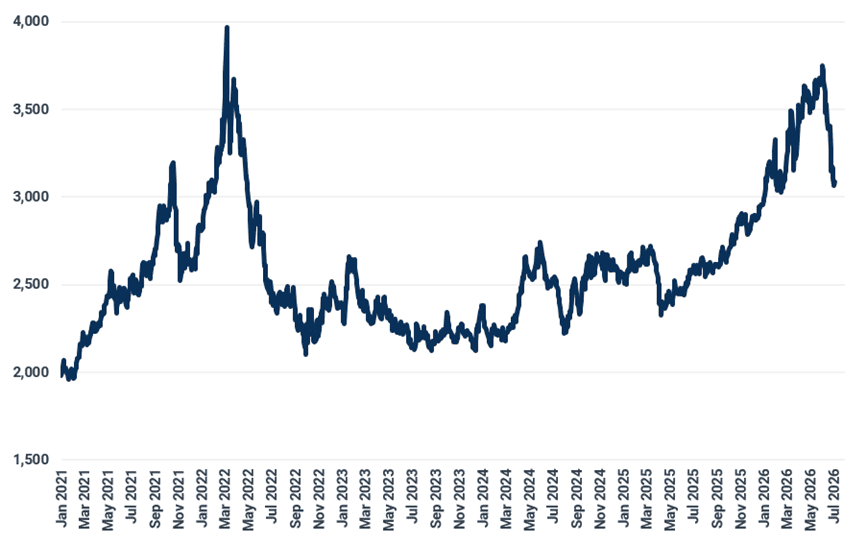

The threat of GCC supply disruption drove aluminium prices to the highest level since February 2022, when Russia launched its full-scale invasion of Ukraine however, improved prospects for peace saw them pull back. Nevertheless, the loss of Middle Eastern output means the global aluminium market is expected to be in deficit this year.

Aluminium LME 3-month official: price has fallen as war risks ease, but remains high ($/t)

Source: Kpler Insight, LME, Argus

United States supply chain implications

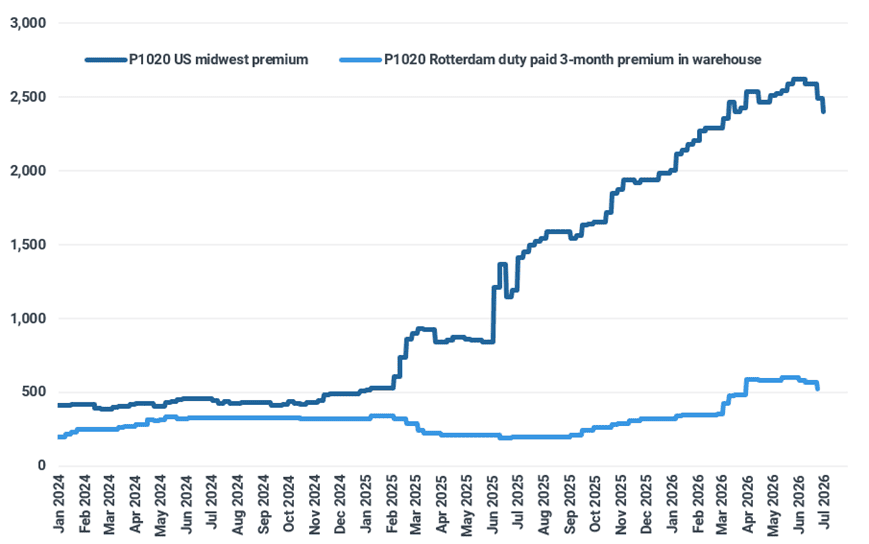

The GCC accounted for 16% (1.95Mt) of US aluminium imports in 2025. War in the Middle East drove the Midwest aluminium premium to a record $2,623/t on 27 May. It remains above the pre-war level.

However, Section 232 tariffs on imported aluminium products remain the primary driver of higher US aluminium prices and the most important factor in shaping US aluminium supply chains.

US importers face additional war-driven competition for Canadian aluminium from the European market, which is looking to replace Middle Eastern material and pivot supply chains to lower-carbon production. Canadian aluminium exports to the EU27 exceeded 1Mtpa for the first time in 2025, up 353% y/y. In contrast, Canada to US trade fell by 22% y/y in 2025 to 5.30Mt. Competition will remain strong while Middle Eastern supplies are disrupted.

Ramping up US domestic aluminium production is not an option in the short term. Aluminium producers are struggling to compete with data centres for access to electricity. Alcoa and Century Aluminium are both selling shuttered operations to the data centre industry.

Rest of the world supply chain implications

Europe has a structural disadvantage in aluminium production and will need to boost imports from non-Middle Eastern suppliers. Asian producers, including China and Indonesia, will be beneficiaries of higher aluminium prices.

The European P1020 duty-paid aluminium premium (in-warehouse Rotterdam) hit a peak of $600/t on 13 May, before retreating alongside global prices.

European supply chains were already strained due to the phasing out of Russian aluminium, the planned closure of the 0.58Mtpa Mozal smelter in Mozambique in March 2026, and the partial shutdown of the 0.32Mtpa Norðurál Grundartangi smelter in Iceland from October 2025 to April 2026. Europe faces structural power price disadvantages, exacerbated by the 2022 energy crisis. The restart of 75ktpa of aluminium capacity at Hydro’s Slovalco facility is an outlier. Supply chains will continue to be dependent on imports, including increased flows from Canada to replace lost Middle Eastern volumes. Imports from the GCC totalled 2.86Mt in 2025.

Responding to higher prices, China increased production and exported more. Domestic aluminium output hit a new high of 3.83Mt in May, putting the country on track to breach a self-imposed 45Mtpa capacity cap on primary aluminium production. The government responded with inspections and environmental assessments that saw some capacity shuttered. This caps the upside for exports, with most aluminium remaining in the domestic supply chain.

High prices will accelerate new capacity projects in emerging producers such as Indonesia. Tsingshan Group has asked nickel pig iron producers at Weda Bay, Indonesia, to cut output in order to preserve energy for aluminium production. However, any acceleration in Indonesia will play only a very limited role in easing global supply tightness in 2026.

US and European price premiums: tariffs, not war, is the driver of high US domestic aluminium prices ($/t)

Source: Kpler Insight, LME, Argus

See why the most successful traders and shipping experts use Kpler