Are French Q3-26 and Q3-27 underpriced?

France is in its most severe heatwave on record, with 23 & 24 June the two hottest days ever recorded nationally. A heat-driven transformer failure cut power in Finistère (Britanny, France) yesterday. While nuclear today is absorbing the shock better than the headlines suggest, Kpler Insight believes the real mispricing lies elsewhere: evening summer tightness driving dangerous high-priced market coupling hours, a fragile hydro outlook, and drought risks. Q3-26, and especially Q3-27 at 38 €/MWh, look underpriced today, according to Kpler Insight.

Executive Summary

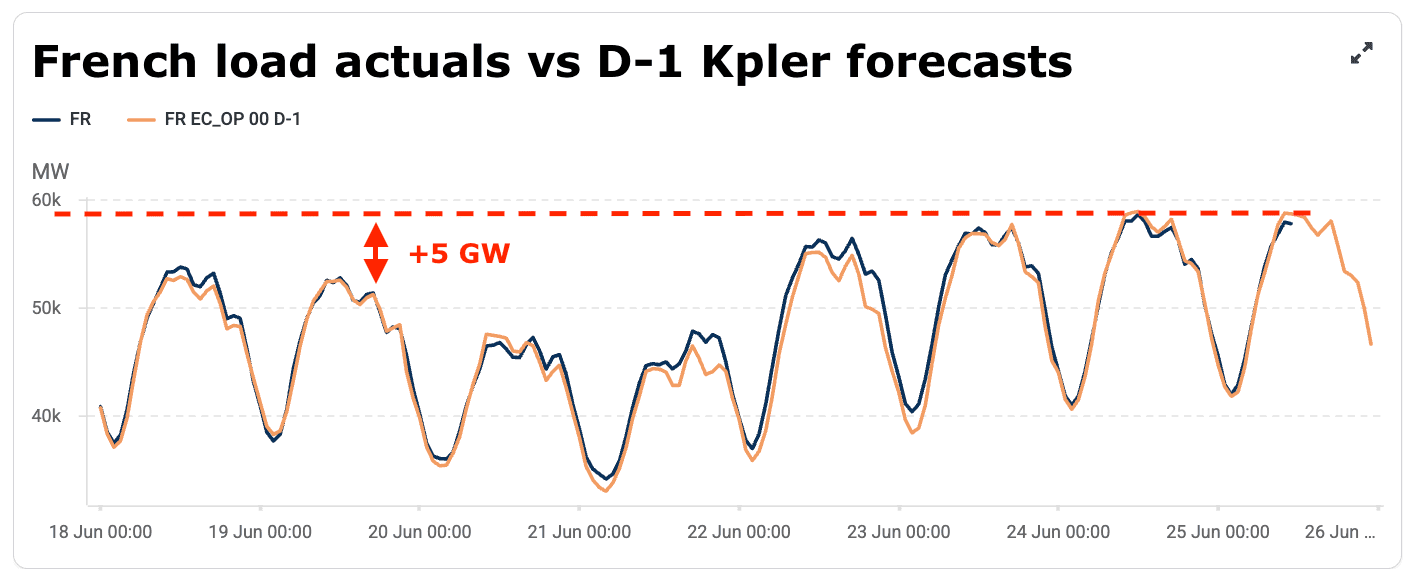

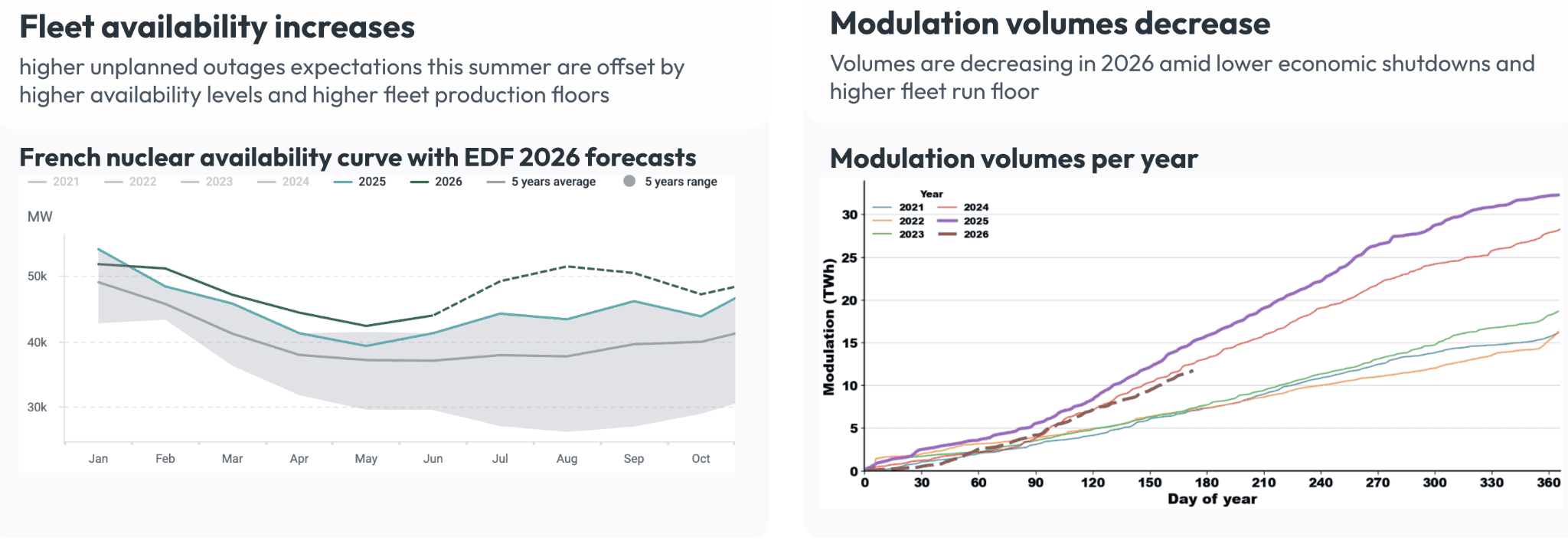

- The heatwave is historic, but nuclear is holding up. France is in a 2003-comparable heat episode that has lifted evening peak demand 9% w/w to ~57 GW. Weather-related constraints are trimming an estimated 5-6 GW of nuclear capacity, yet availability is +5.5 GW y/y, modulation volumes are running lower y/y, and cumulative output is up ~8 TWh y/y.

- While nuclear disruption seems fairly priced in, hydro and market tightness are not. This tightening is being driven by an exceptionally hot summer outlook, anticipated drought risks, and already stressed Alpine and Nordic hydro conditions.

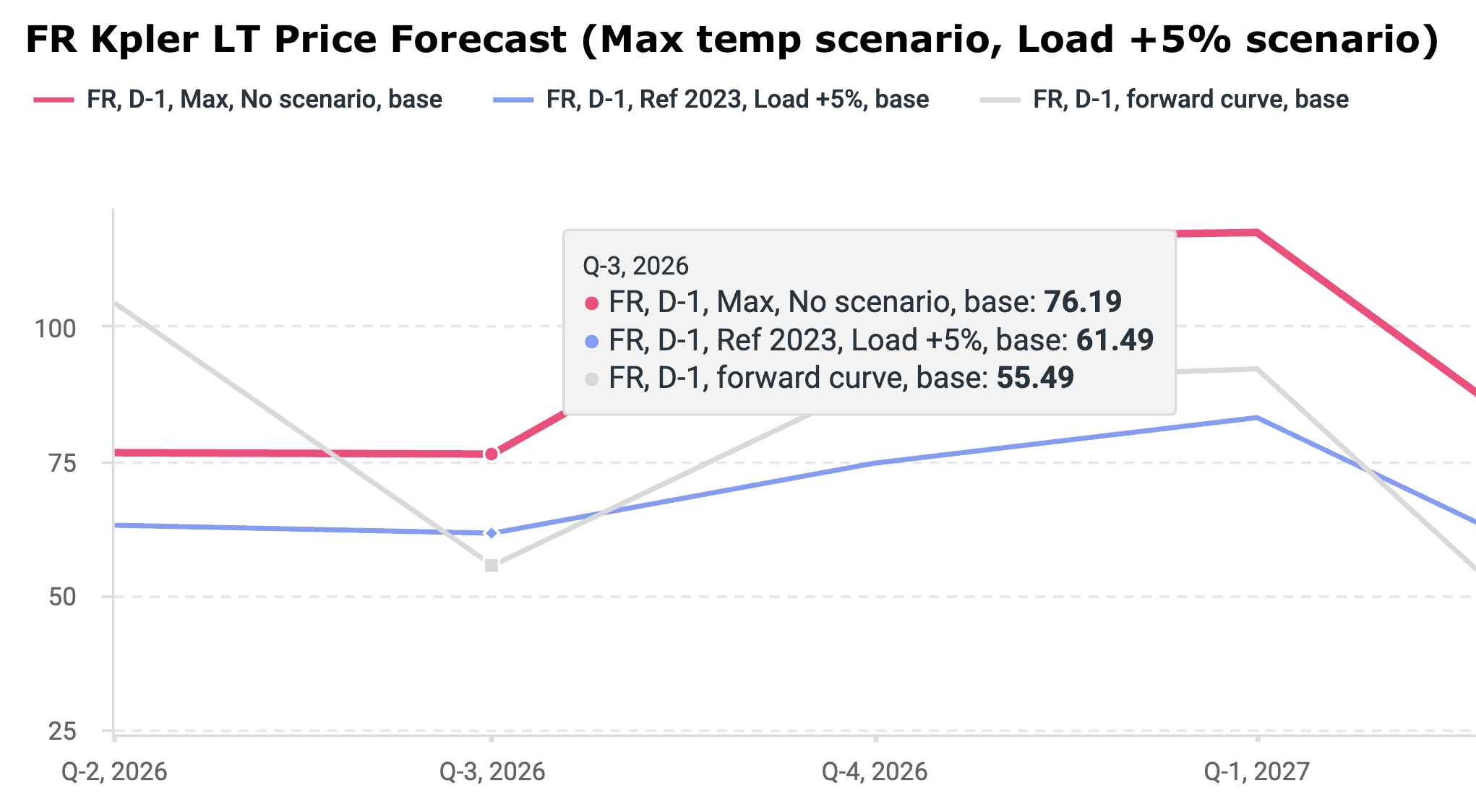

- Kpler LT models point higher. Under a load +5% and max weather scenario, Kpler's LT FR forecast lifts Q3-26 by 5 to 20 €/MWh. With similar dynamics likely to repeat, Q3-27 at 38.16 €/MWh looks strongly underpriced.

Market & Trading Calls

FR Q3-26: Bullish, driven by heatwave-driven evening demand, increasing drought risks at the end of summer and a fragile hydro outlook. These three risks skew Q3-26 toward the upper end of our LT scenarios, against a fleet that is holding output near 2025 levels rather than collapsing.

FR Q3-27: Bullish with conviction. Currently priced at ~38 €/MWh, almost 20 €/MWh below Q3-26 at 58 €/MWh (as of 24 June), with the temperature expected to be elevated because of El Niño and A/C penetration increasing temperature sensitivity.

Navigating through a historical heatwave

France is navigating one of the most severe heatwaves on record.

Over the past few days the country has been among the hottest places on the planet: 23 and 24 June became the two hottest days ever measured nationally, the 24-hour average breaching 30°C for the first time and the episode running at an intensity Météo-France puts on a par with August 2003. Maxima have reached 40-42°C across the western two-thirds of the country.

The grid shows strain.

Other than continuous RTE must-run calls to ensure grid voltage stability, on the evening of 23 June, two heat-related explosions on a 225 kV RTE transformer at the Squividan substation (Finistère) caused a 100 MW disruption in North-West France. The prefecture attributed the failure directly to the extreme heat.

Demand has tracked the thermometer: evening peak load rose 9% w/w to ~57 GW.

On the nuclear side, the picture is more currently reassuring than the headlines imply.

The heatwave is trimming an estimated 5-6 GW of capacity, but the fleet enters the summer in materially better shape than a year ago: availability is +5.5 GW y/y and expected to stay high, modulation volumes are running lower y/y, and cumulative output is up ~8 TWh y/y.

Our view: high availability, lower modulation activities and the RTE–EDF agreement could spare southern plants the most drastic reductions, keeping output broadly in line with (or slightly below) 2025.

With temperature sensitivity steepening, the fear of nuclear disruption looks fairly priced in, but some risks remain underestimated.

Which risks are potentially being underpriced ?

Evening demand tightness increases market coupling dynamics amid price spikes near neighbouring countries.

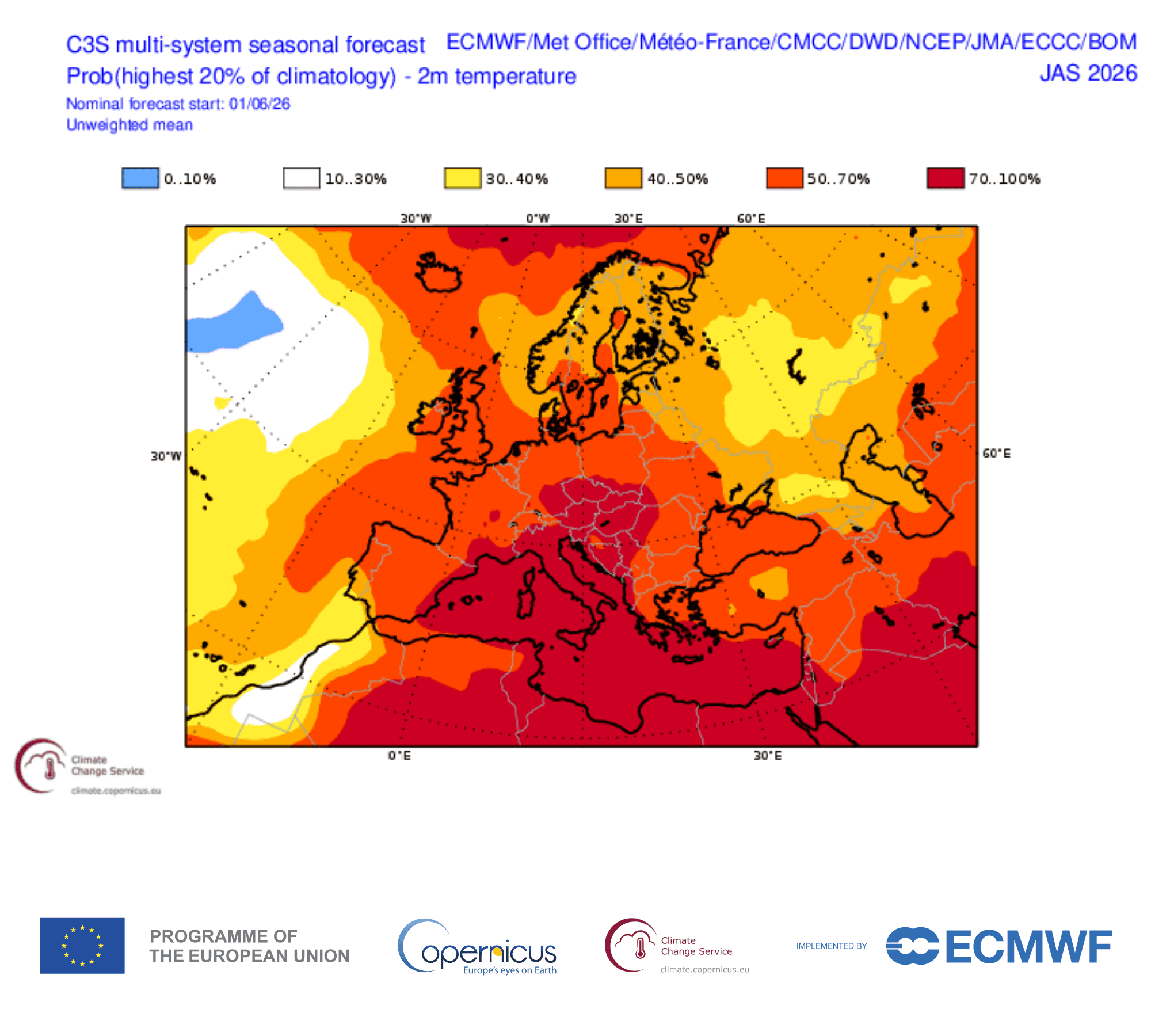

Eight or nine of the nine major forecasting systems point to a higher-than-normal probability of above-average temperatures this summer, with the Continental European anomaly running a particularly steep 1-2°C above seasonal norms.

For power markets, this combination means higher cooling demand, greater environmental-constraint risk, lower thermal generation and transmission efficiency, weaker solar PV yields, and a higher likelihood of weather-driven volatility through the season across the whole region.

These outliers can run far above the curve: Belgium just cleared above 1,000 €/MWh in a single evening quarter hour. Notably, Italy even reversed its usual flow and became an exporter to France and Switzerland, highlighting the severity of the regional supply tightness.

Thus, France becomes especially vulnerable this summer to a high-priced market coupling dynamic when:

- Hot weather pushes domestic demand towards 57 GW, as seen this week.

- Nuclear availability remains limited to around 44-45 GW throughout the summer.

- Run-of-river hydro falls below to 3 GW avg levels during Q3.

- Solar generation fades during the evening peak.

Average summer wind output in France is ~3-4 GW, leaving a clear supply evening gap.

In the absence of stronger wind generation events, France becomes increasingly exposed to market coupling, which under tight system conditions can amplify both exports and price spikes.

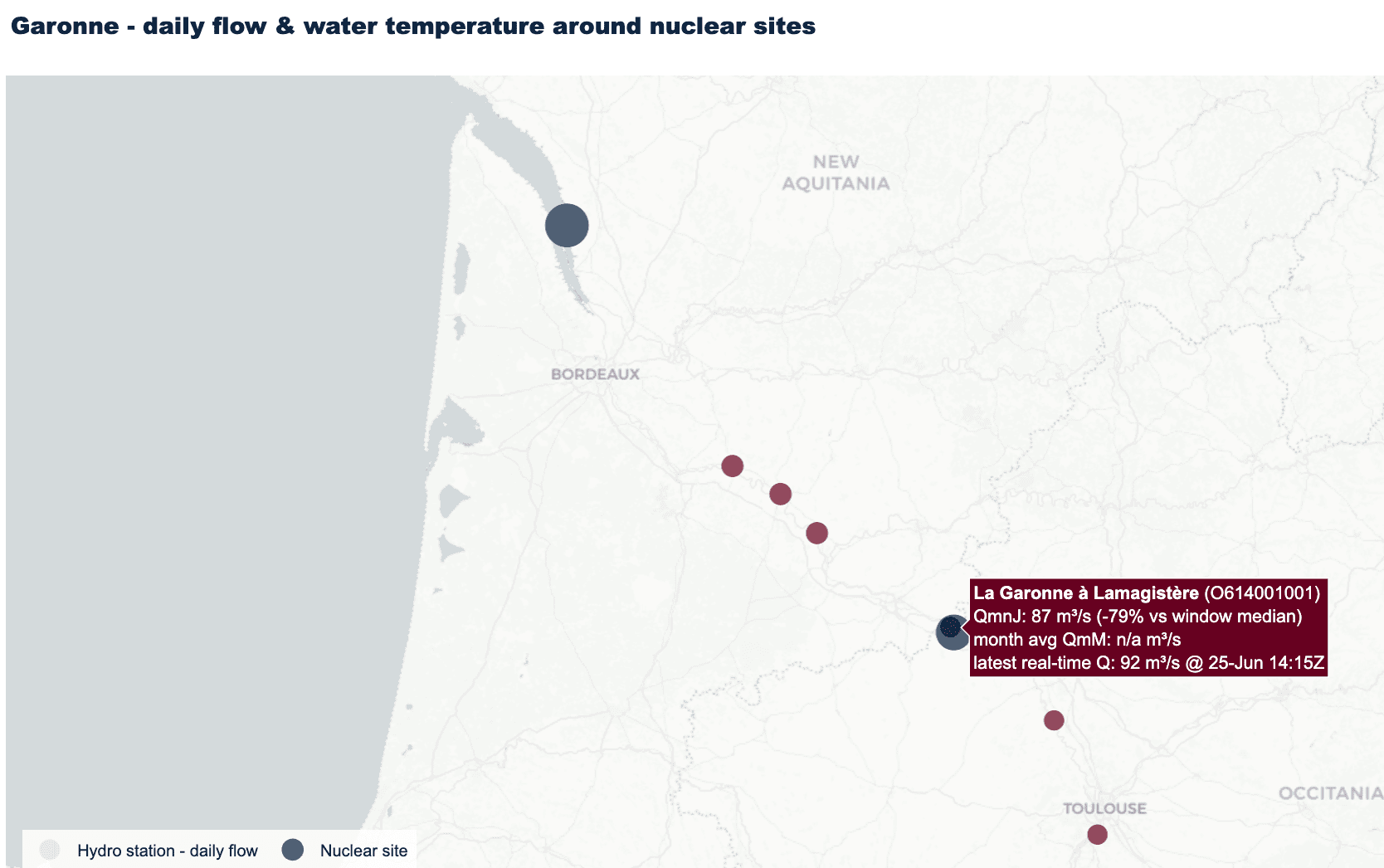

End-of-summer river drought risks.

If the heat persists, river flows are likely to remain under pressure into the latter part of the season.

Near Golfech (at Lamagistère on the Garonne), river flows are around 80% below the 200-day median, while near Saint-Alban on the Rhône they are around 50% below the 200-day median. This suggests Golfech is more exposed to drought-related constraints than to high water temperatures today.

With sustained elevated temperatures, RTE can often maintain voltage stability through must-run derogations.

But a drought is different: once river flows become insufficient, plants using cooling towers have no alternative but to reduce output.

Fragile hydro

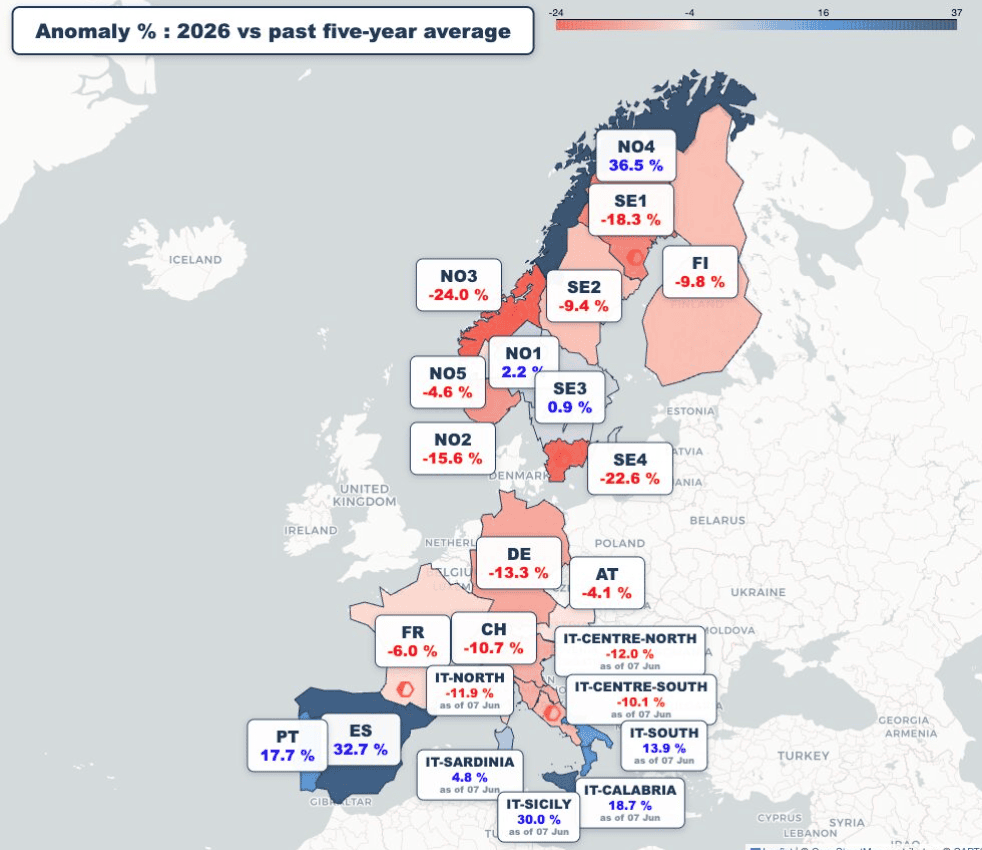

While Spanish hydro is abundant and supporting France in the evening with 3 GW exports on average this week, the hydro outlook in the Alps and the Nordics looks fragile.

- NO2 remains 15.6% below five-year seasonal averages, limiting exports to Germany, Netherlands, Great Britain and DK1.

- Alpine stocks remain 6% below five-year average, with record temperatures likely to impact the management of reservoir water to meet evening demand.

Kpler LT price forecast outlooks

We applied two stress scenarios to our long-term price forecast:

- Under a +5% load scenario (using REF_2023 weather conditions), Q3-26 prices increase by 5-20 €/MWh relative to the latest market settlement.

- Under our max weather scenario, Kpler's long-term French power price forecast rises by around 20 €/MWh relative to the base case.

Power market insights you can trust

This article is from Power Insight which covers the European power market in depth, and includes the following reports:

- Power weekly – Week-ahead trading calls for Belgium, France, Germany, and the Netherlands; blends Kpler forecasts with a review of generation, fuel markets, and supply & demand.

- Weather weekly – 14-day to 3-month power-market weather forecasts (ECMWF/NOAA) covering temperature, wind, and precipitation across CWE, CEE, SWE, and the Nordics for near- and long-term trading.

- Power monthly – In-depth French and German market analysis with directional views on front-month, quarter, and year-ahead contracts, driven by fuel markets, renewables, generation availability, and cross-border flows.

See why the most successful traders and shipping experts use Kpler