Atlantic MR pressure shifts: Navigating the split

Global tanker markets faced widespread downward pressure in late May. VLCC, Suezmax, and Aframax freight rates across key routes declined due to structural oversupply and influxes of ballast vessels. While Cross-Med Aframaxes and MEG-Japan LR2s managed to trade flat or steady , MR product tankers diverged sharply. UKC-USAC rates weakened , whereas USG-UKC benchmarks surged on resilient transatlantic summer demand.

VLCC

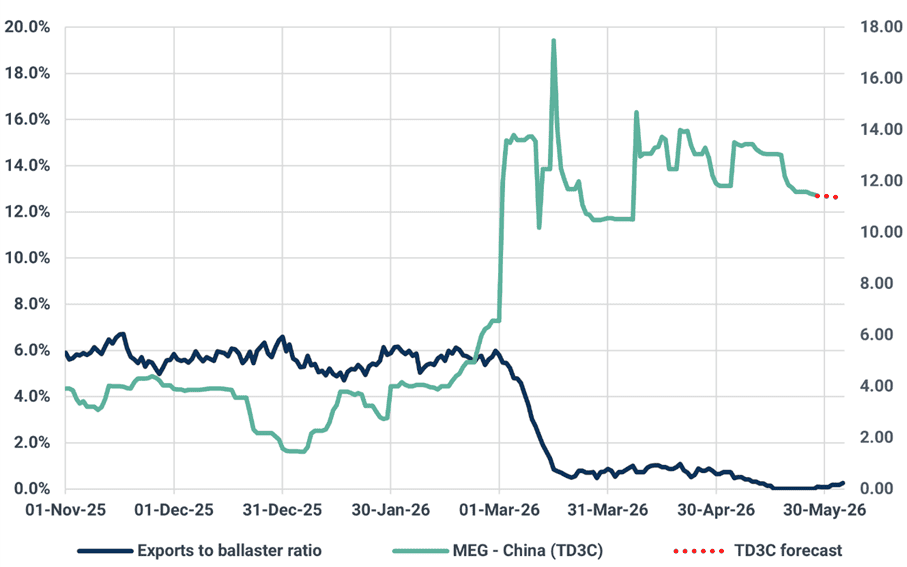

MEG – China (TD3C)

MEG to China VLCC rates continued descending in the last decade of the month, slipping by $0.31/bbl to $11.430/bbl. As May comes to a close, Kpler data suggest that just one VLCC, with no prior exposure to parallel trades, entered the MEG throughout the month, highlighting that liquidity on the route remains thin. A closer look suggests that the vessel in question followed the newly established Iranian route, centered on Larak Island. However, the past week saw OFAC sanction the Persian Gulf Strait Authority (PSGA), the Iranian body introduced to oversee transits through the Iranian corridor, curbing any optimism over an uptick in the ballaster traffic through the specific route. Absent progress in US-Iran talks, rates are expected to fall further over the forecast.

VLCC MEG tonnage balance ratio (%) (10MA) vs TD3C ($/bbl)

Source: Baltic Exchange, Kpler

Suezmax

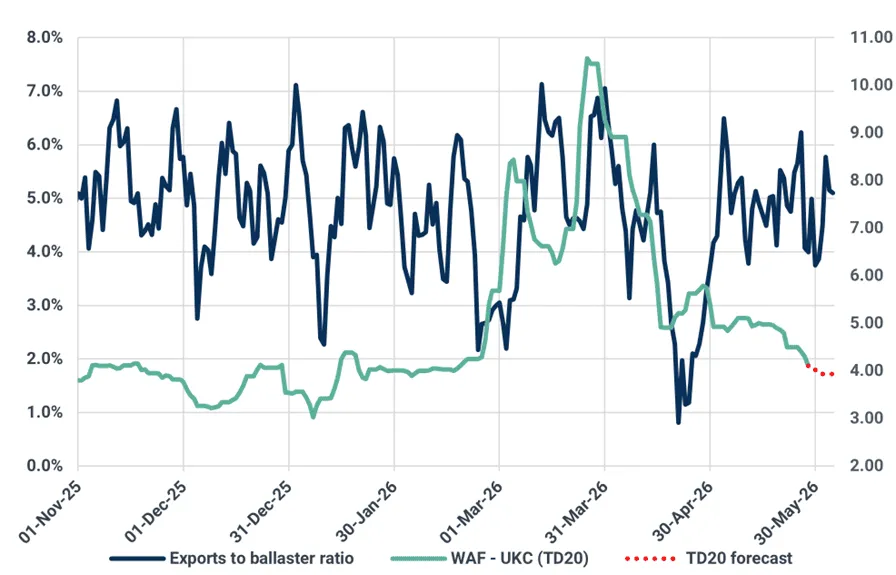

WAF – UKC (TD20)

In line with our expectations, the final decade of May saw a sharp correction in WAF-to-UKC Suezmax rates, with assessments falling by $0.69/bbl w/w to $4.11/bbl. Back in mid-May, we highlighted that a significant wave of ballast vessels from the East would likely trigger a renewed correction in regional assessments. This has now materialised, with most of these vessels having crossed the COGH and moved toward West Africa, while a second, smaller wave of ballasters is currently transiting the western Indian Ocean, suggesting that vessel length will persist into mid-June.

Suezmax WAF tonnage balance ratio (%) (10MA) vs TD20 ($/bbl)

Source: Baltic Exchange, Kpler

Aframax

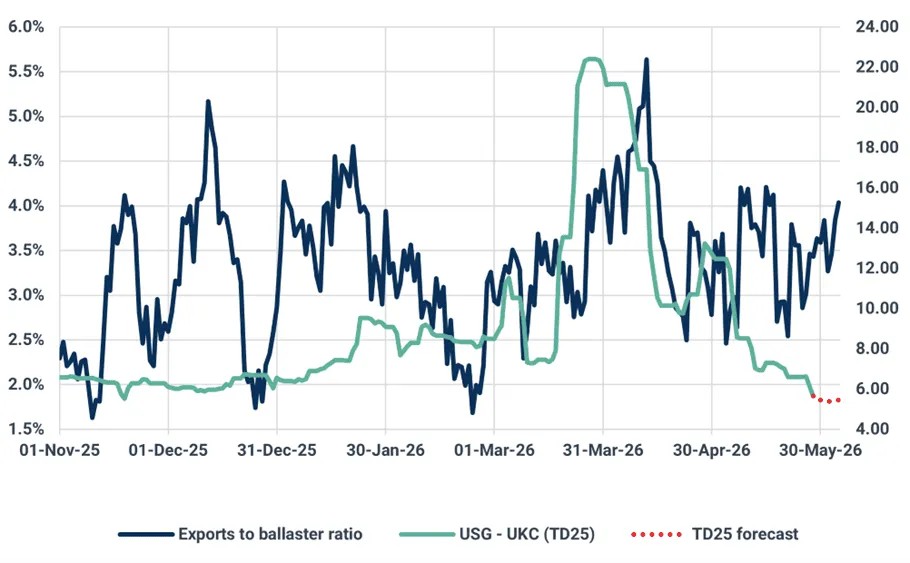

USG – UKC (TD25)

The descent in USG-to-UKC Aframax rates also accelerated toward the end of the month, with benchmark assessments declining by $0.96/bbl w/w to $5.65/bbl. This latest drop has left rates approximately 34% below their pre-conflict levels.

US Gulf crude exports to Europe rose to 2.4 mbd in May, with Aframaxes emerging as the primary beneficiaries, accounting for around 1.6 mbd of these flows. Despite the supportive demand backdrop, the Atlantic basin remains structurally oversupplied. By the end of May, the number of Aframaxes trading in the dirty market West of Suez had risen to 591 vessels in the final week of the month, representing an approximate 30% y/y increase. In comparison, WoS Aframax loadings have expanded by only 18% y/y as of May, highlighting that supply growth continues to significantly outpace that of demand.

Current tonnage balances suggest that the pace of the rates’ decline may slow over the forecast period.

Aframax US Gulf tonnage balance ratio (%) (10MA) vs TD25 ($/bbl)

Source: Baltic Exchange, Kpler

LR

MEG – Japan (TC1)

MEG-Japan LR2 rates held broadly steady, easing just $0.07/bbl from $13.42/bbl to $13.35/bbl over the week, with a brief dip to $13.31/bbl mid-week before recovering.

The structural weight on this route is Asian petchem weakness. Cracker run rates remain suppressed across Northeast Asia. South Korean operators reduced rates again this week, Japan's Maruzen cracker in Chiba stays in maintenance until July, and China's weak downstream demand is expected to cap any recovery through June–July. Global naphtha exports are at multi-year lows, constraining cargo generation for LR2 owners.

The partial offset comes from the Atlantic. The wide Eurobob-naphtha spread is incentivising blending in the ARA region, drawing marginal barrels westward. The LR2 ballast count in the West is at multi-year lows following April's clean-to-dirty switching, limiting supply-side pressure. Rates are expected to trade sideways in the near term, with upside capped by the potential for further vessel switches back to the dirty market.

MR

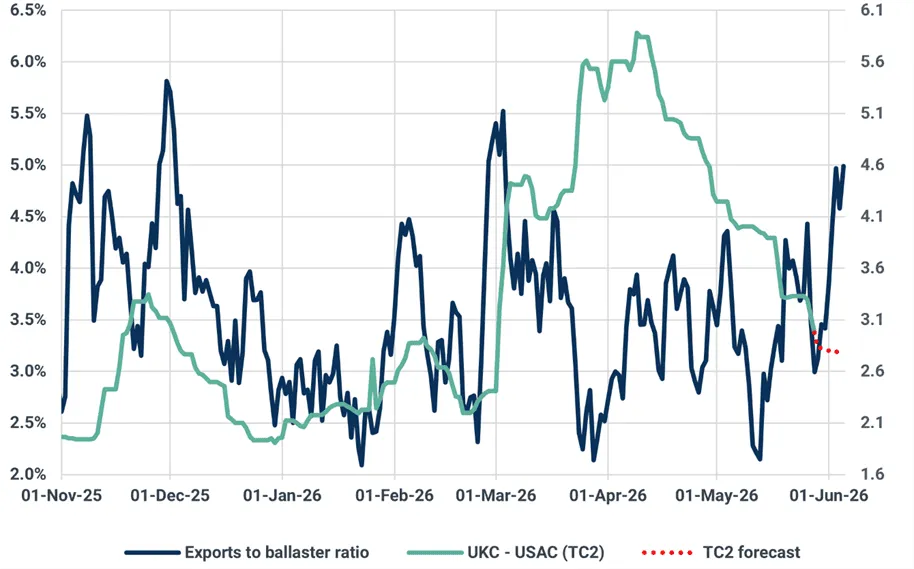

UKC – USAC (TC2)

UKC–USAC MR rates fell $0.34/bbl over the week, from $3.32/bbl to $2.98/bbl, extending recent weakness.

The fundamental backdrop offers some support. Trans-Atlantic flows have recovered above 400 kbd in May after a slump to 200 kbd in April. US gasoline inventories are near 5-year seasonal lows ahead of the summer driving season, sustaining demand for this route. However, these positives are being offset by a broader supply build on Atlantic MR tonnage. The retreat from record West-to-East flows seen in March/April has swelled the Atlantic ballast count, shifting control to charterers. With long-haul export momentum fading and no imminent catalyst to absorb excess tonnage, we expect rates to remain under pressure near term, with summer gasoline demand providing a floor rather than a springboard.

MR UKC tonnage balance ratio (%) (10MA) vs TC2 ($/bbl)

Source: Baltic Exchange, Kpler

Navigate these shifts with Kpler Chartering

When routes diverge this sharply, with TC14 surging while TC2 slides, the difference between a well-timed fixture and a missed opportunity comes down to how quickly you can read the market and act on it.

Kpler Chartering gives charterers, brokers, and shipowners the tools to act on intelligence like this in real time. It brings together tonnage visibility, cargo intelligence, market fixture data, voyage economics, live AIS tracking, and email management, into a single, integrated workspace. It replaces the fragmented combination of inboxes, spreadsheets, and separate AIS & data tools that define the traditional chartering desk.

Track ballast counts & vessel availability across every basin, model voyage economics across competing routes, match cargo orders against live fleet positioning and benchmark every negotiation against real-market prints. With 36,000+ commodity vessels tracked and freight data going back over a decade, Kpler connects the cargo intelligence and workflow tools you need to stay ahead of market turns. Explore Kpler Chartering

See why the most successful traders and shipping experts use Kpler

Ready to charter smarter?