Europe’s solar capture rates hit record lows as market divergence widens

After record-low capture rates this spring, Kpler Insight forecasts a strong seasonal recovery into winter, but the rebound leaves clear winners and losers across Europe.

Executive Summary

- The average European solar capture rate fell to 38%, its lowest ever levels and down 7 percentage points from last year’s record low in May.

- After France recorded the lowest solar capture rate across all European markets at 9.5% in April, Kpler forecasts point to sharp rebound over the coming months.

- Germany’s solar capture rate fell by 6 percentage points y/y to 25% in April but climbed steeply (+34 pp) in June thanks to the heatwave.

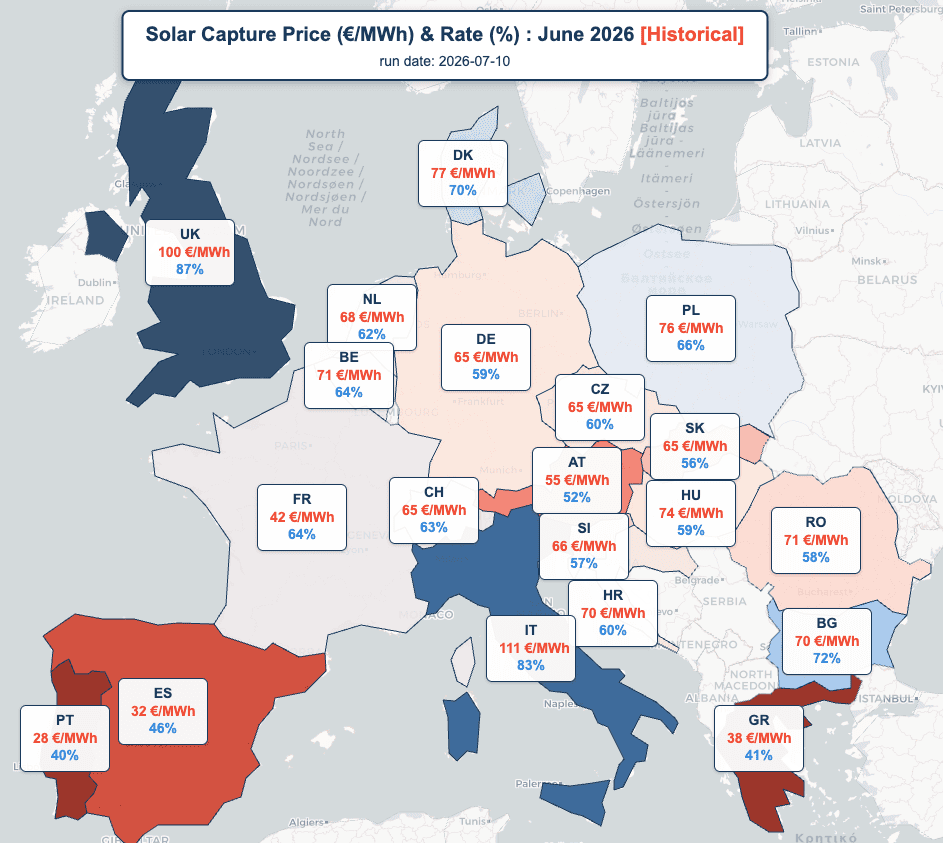

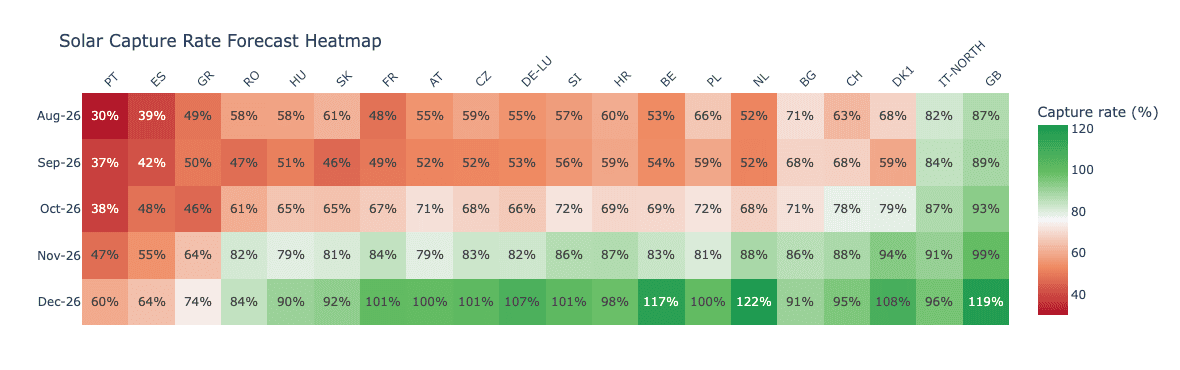

- Iberia continues as the weakest solar market, with Portugal and Spain set to average only 42% and 50% capture rates respectively across Aug-Dec 2026.

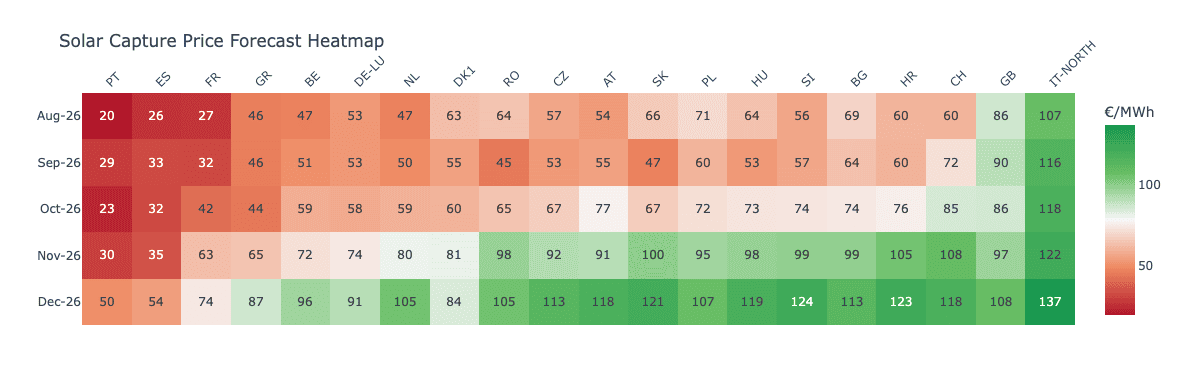

- Consistently leading the European market, Great Britain is projected to hit 97% in Dec-26 while Italy-North averages the highest forecasted capture prices of ~120 €/MWh over the next five months.

The value of solar is becoming increasingly location-specific. Across Europe, rising solar penetration is making capture economics a more important revenue driver than outright baseload prices.

The key question is no longer simply where power prices are highest, but where solar generation still coincides with valuable hours.

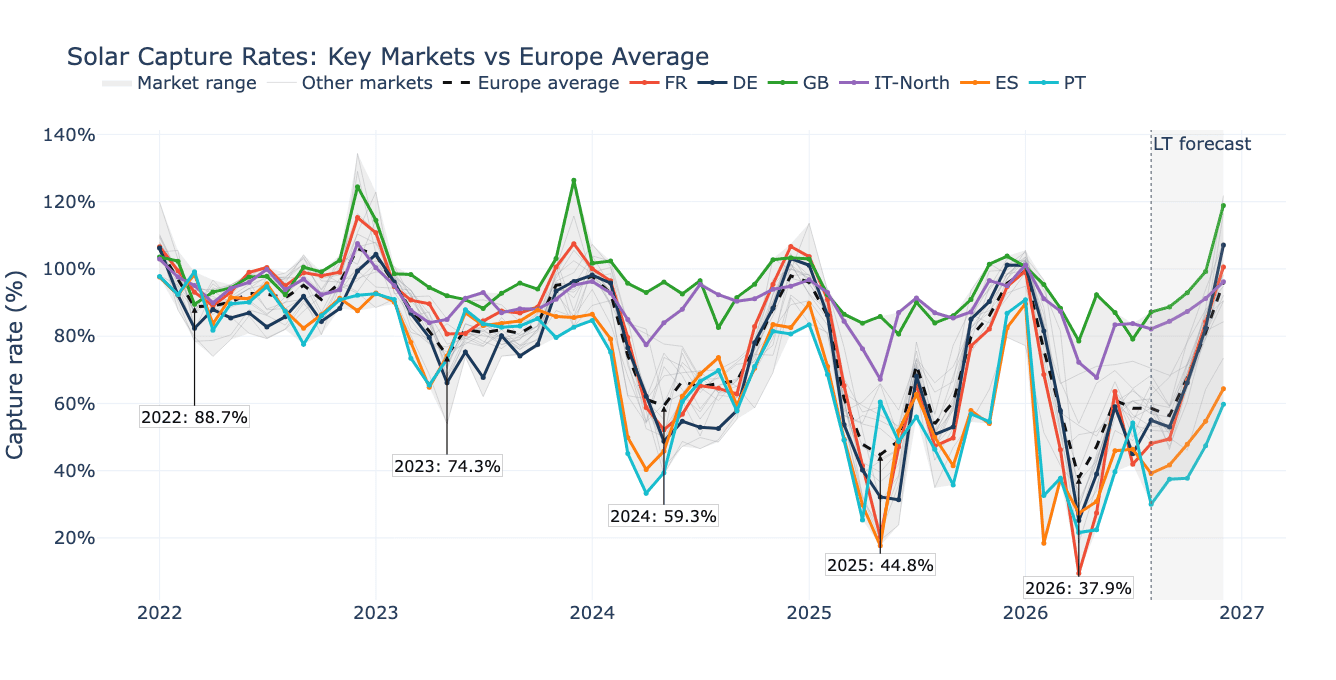

Solar capture rates are becoming more volatile

Solar capture rates are no longer moving in a narrow band around baseload prices.

Through 2022 and early 2023, most major markets clustered close to 80-100%. Since 2024, the dispersion has widened sharply, with repeated spring and summer drawdowns pushing several markets below 50%.

France stands out for the severity of the 2026 compression, where solar capture rates fell to around 9.5% in April 2026. This was the lowest recorded capture rate across Europe due to a combination of factors including:

- High nuclear availability resulting in a larger inflexible baseload supply

- Mild weather and holiday periods, softening power demand in France

- And most importantly, solar surplus domestically and in neighbouring markets

However, the heatwave in June helped recover capture rates to 63% as high temperatures reshaped daily demand patterns and tightened supply.

Germany paints a similar picture falling to 25% in April 2026, its lowest levels since reaching 31% in June 2025.

Over the past 12 months, Great Britain and Italy-North have remained the strongest solar capture markets, outperforming the European average by around 20 percentage points, while Iberia has stayed at the lower end of the range.

This shows that average power prices can remain positive, but solar revenues will still collapse if mid-day prices weaken.

Looking ahead: winter recovery, but not a reset

To model a warm, El Niño-style weather pattern, this view uses Kpler’s 2023 weather reference year rather than a long-run mean weather case.

Using these weather parameters, Kpler’s long-term forecast points to a seasonal uptick in solar capture rates into winter, but the rebound is uneven across markets.

The results point to a sharp rise in both French and German solar capture rates into winter. In France, capture rates can rise from 48-49% in Aug-Sep 2026 to around 101% by Dec, while Germany follows a similar upward trajectory reaching 107% by Dec.

The recovery reflects a more supportive winter price shape, as lower solar output reduces midday cannibalisation and stronger daytime system tightness lifts the value captured by solar generation.

Spain and Portugal continue to trail average European levels by roughly 25 percentage points across Aug-Dec 2026.

By contrast, GB and Italy North remain the strongest markets, with GB averaging a 97% capture rate and Italy North delivering the highest forecast capture price at around 120 €/MWh.

The overarching trend across Europe is a structural collapse in solar capture factors, primarily because massive capacity additions are severely outpacing power demand and storage deployment during midday peak hours.

Despite the grim structural picture, Kpler Insight identifies two key upside drivers:

- Summer heatwaves lift power demand for cooling, raising the midday price floor.

- High gas prices due to geopolitical tensions increase spot prices when gas-fired generation sets the price during “shoulder hours”.

Low capture rates are a storage signal

Low solar capture rates are not only a warning signal for merchant solar revenues, but also point to a growing opportunity for Battery Energy Storage Systems (BESS).

Solar profitability ultimately relies on structural demand revival, with BESS assets uniquely positioned to capture immediate value.

When solar-heavy midday hours clear at a steep discount to evening peaks, BESS can monetise the same price shape that is eroding solar capture values.

Power Insights you can trust

Beyond a weekly report, Power Insight also includes:

- Ongoing market updates as events develop

- A monthly deep-dive report covering structural trends across European power markets

Interested in a demo to see everything Power Insight has to offer? Request a 30minute demo of Power Insight.

See why the most successful traders and shipping experts use Kpler