New pipelines bypassing the Strait of Hormuz could come online in 1-2 years

Saudi Arabia's East-West pipeline and the UAE's ADCOP pipeline are currently the two most strategically significant pieces of infrastructure in the MEG. Expansion projects at these pipelines and their associated ports will enable a further reduction in reliance on the SOH over the coming years. In particular, 2027 could see the UAE increase its bypass capacity from 1.8 Mbd to 3.6 Mbd.

The US-Israel war on Iran has revived momentum behind a range of infrastructure projects aimed at reducing reliance on the Strait of Hormuz. As we predicted in early May, progress is emerging primarily on projects that expand capacity within existing corridors, rather than on new cross-border infrastructure — specifically, building additional parallel capacity alongside ADCOP to Fujairah, and debottlenecking and enhancing the Saudi East–West pipeline.

The continued investment by Gulf states in contingency energy infrastructure, including alternative export pipelines, storage facilities, and redundancy measures—reflects a growing recognition that reliance on the Strait of Hormuz as the sole outlet for exports is no longer a prudent long-term strategy. At the same time, these governments face the difficult task of balancing the substantial financial costs of building and maintaining contingency infrastructure against the probability of prolonged disruption. This trade-off is further complicated by political uncertainty: while the current Trump administration will conclude its term within the next few years, the prospect of regime change in Iran appears considerably less likely, suggesting that the strategic risks associated with Tehran are likely to persist well beyond the current U.S. political cycle.

Acceleration of the UAE's West-East pipeline project and Fujairah port expansion

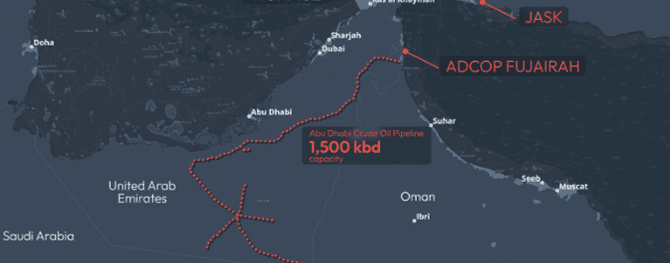

Plans to expand the UAE's ADCOP (Habshan-Fujairah) pipeline bypassing Hormuz were already in motion prior to the current crisis, with ADNOC evaluating a second parallel line — a $3 billion, 300-kilometre project —as early as 2023. Unlike the existing ADCOP route, this new line would allow offshore and western Abu Dhabi crude streams to reach Fujairah without transiting the Gulf, with the aim of doubling the UAE's Strait bypass capacity from approximately 1.8 Mbd to over 3 Mbd.

Recent reports indicate the new pipeline — the West-East Pipeline project — is 50% complete and targeting an early-2027 start, with the UAE's Crown Prince having directed ADNOC to fast-track construction. This ambitious timeline has only become feasible against the backdrop of the SOH blockade and a broader recognition of how deep regional dependencies on this waterway run. Given that Fujairah port itself will need to be expanded, we see a mid-2027 (rather than early-2027) startup as more likely for the pipeline to materially impact exports. Once realized, this development would channel offshore UAE grades — such as Upper Zakum, Das Blend, and Umm Lulu — to the port of Fujairah.

Existing UAE ADCOP pipeline

Source: Kpler

Expanding the Saudi East-West pipeline by 1-2 Mbd

Separately, Saudi Arabia has reportedly begun preliminary discussions about increasing East–West Pipeline capacity by 1–2 Mbd, however industry sources familiar with the matter told Kpler that the expansion being considered is related to the construction of a parallel products pipeline.

Currently the kingdom’s east-west pipeline is capable of moving up to 7 Mbd from Abqaiq to Yanbu on the Red Sea. Looking ahead, though, the binding constraint isn't the pipeline itself but the export terminals downstream: sustainable export capacity at Yanbu is estimated at around 4.5–5 Mbd — roughly 1.5 Mbd from the Yanbu North Crude Terminal and around 3.0 Mbd from Muajjiz — leaving limited scope to push beyond that ceiling under current infrastructure. Any meaningful increase in throughput would therefore require debottlenecking the loading infrastructure at Yanbu before pipeline capacity itself could be expanded or a parallel pipeline added. Given these bottlenecks, we'd expect this project to materialize over a longer horizon, with a start-up date feasible from 2028 onwards.

New Mediterranean corridors planned via Turkey and Syria

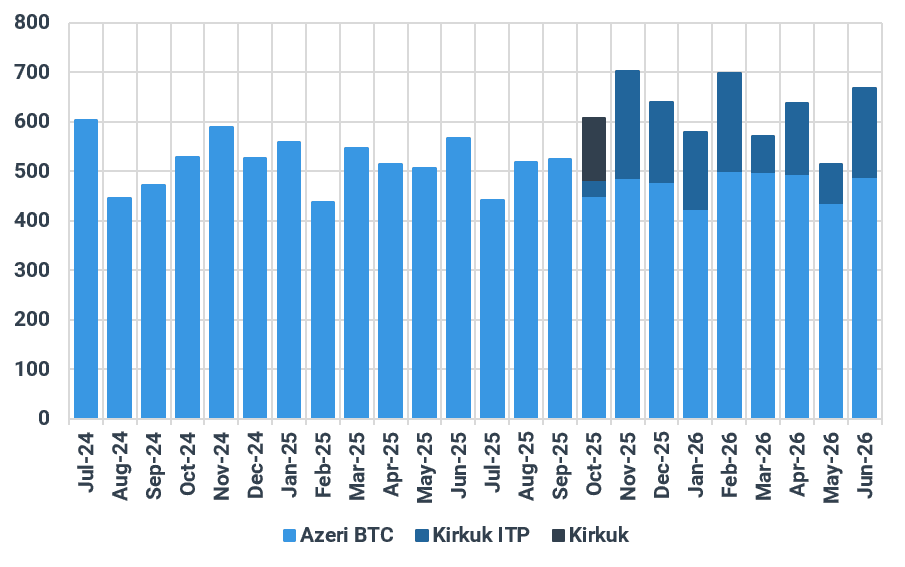

Similar momentum is building in the Mediterranean. In March 2026, Turkey proposed extending the Kirkuk-Ceyhan pipeline south to Basra — a move that would create a full Mediterranean export corridor and substantially cut Iraq's dependence on Hormuz. Discussions around the Basra-Haditha-Baniyas pipeline have also gained traction, and both projects are now back on the table. Iraq's cabinet has cleared the state-run Basra Oil Company (BOC) to sign preliminary agreements with a Chevron-led consortium to advance the two pipeline options. These initial agreements set the stage for the consortium to prepare technical and financial feasibility studies comparing the Basra-Haditha-Kirkuk-Ceyhan and Basra-Haditha-Baniyas routes. If these studies are completed by year-end, construction could begin as early as next year — though the projects themselves would still take another 3-5 years to complete. Should the Basrah-Kirkuk-Ceyhan project be realized, this would naturally increase exports out of Ceyhan.

Ceyhan crude exports, by grade, kbd

Source: Kpler

See why the most successful traders and shipping experts use Kpler

.jpg)