Demand destruction from US/Israel–Iran conflict: Asia-Pacific transportation fuels

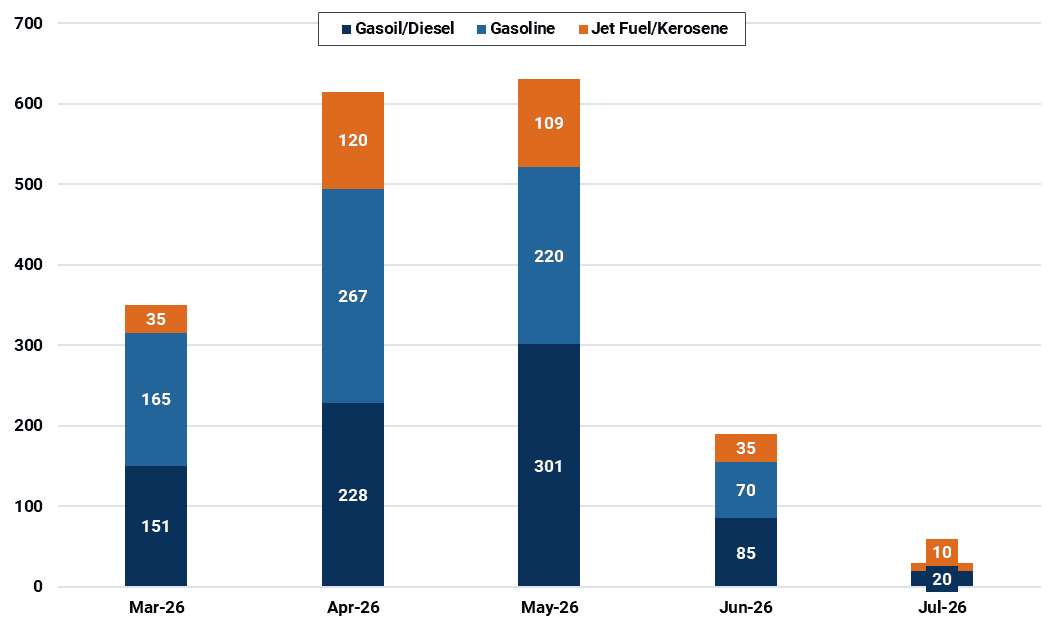

With refinery run cuts emerging across Asia-Pacific as refiners reassess crude availability and prioritise domestic fuel supply – thereby curtailing exports – fuel inventories and, ultimately, demand assumptions are being tested by the closure of the Strait of Hormuz. Assuming the current disruption persists through the remainder of the month, regional demand destruction across gasoline, jet/kerosene, and gasoil/diesel could peak at 630 kbd in May, according to our analysis.

Considering that we have seen no meaningful de-escalation in the US/Israel–Iran conflict nor any signs of a full reopening of the Strait of Hormuz (SoH), we have begun assessing additional demand destruction across oil products globally. In the latest Refined Products S&D release, we already lowered demand projections across all products in the Middle East, together with light ends in Asia. We are now evaluating further impacts under the assumption that the conflict remains intense through early Q2, with normal operations and flows gradually resuming by early May. Given the range of products and regions affected, we are taking a segmented approach, with the aim of presenting a consolidated view of the global oil products demand impact shortly.

As a first update, we have completed demand destruction estimates for Asia-Pacific gasoline, jet/kerosene, and gasoil/diesel. Under our current assumptions, these losses peak at around 630 kbd in May. The estimates are developed on a country-by-country, product-by-product basis, drawing on the latest domestic supply outlooks, trade flow assumptions based on the most recent positions of major regional exporters, and current inventory levels relative to minimum operational thresholds. In essence, the exercise assesses how much demand destruction would be required, under current supply and trade expectations, to prevent inventories from falling below minimum operational levels. We also incorporate pre-emptive demand-curbing measures already implemented in some countries.

Transport fuel demand destruction in Asia-Pacific (kbd)

Source: Kpler

Our current Refined Products S&D already reflects the refined products supply impact of the conflict across the Middle East and Asia-Pacific, which we have covered extensively in recent articles. Building on those insights, as well as industry sources, we have made the following assumptions regarding aggregate transport fuel export reductions from major regional hubs through May:

- Saudi Arabia: 20–35% export reductions

- UAE: 60–80% export reductions

- Kuwait, Bahrain: 70–90% export reductions

- Oman: ~10% export reductions

- South Korea: ~30% export reductions, with refiners prioritising fulfilment of term supply commitments for CPP

- India: ~15% export reductions

- Singapore, Taiwan, Malaysia, Australia, Indonesia: 10–30% export reductions

- China: 50–70% export reductions

- Japan: ~30% export reductions

- Thailand: Energy exports halted to all countries except Laos and Myanmar, currently assumed to remain in place through May 2026.

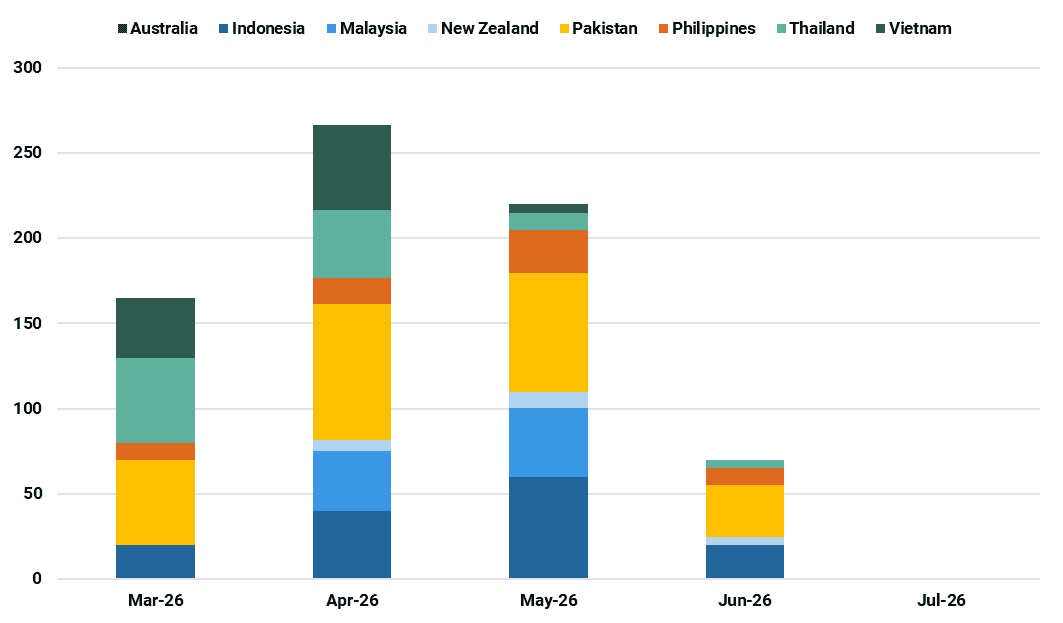

With regards to gasoline, Pakistan appears the most vulnerable to the ongoing disruption. The country holds a deeply net-short position, with roughly 85% of imports sourced from the Middle East, around 20% of which typically transit the SoH. Authorities have already implemented temporary demand-curbing measures, including a four-day workweek, work-from-home mandates, school closures with a shift to online classes, and reductions in government fuel use.

Other major demand centres with high exposure to the conflict include Thailand and Vietnam, both of which have introduced similar pre-emptive measures. Meanwhile, Indonesia, the region’s largest gasoline importer, has indicated that current inventories and available refining capacity should be sufficient to cover demand through the Eid Al-Fitr period.

Asia-Pacific gasoline demand destruction (kbd)

Source: Kpler

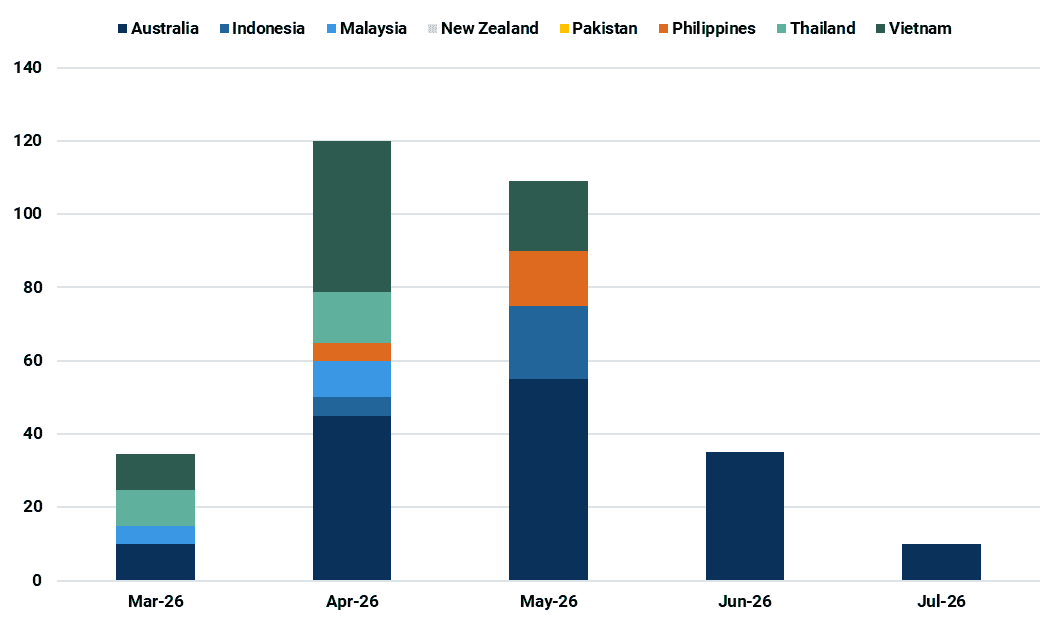

On jet/kerosene, aside from direct disruptions stemming from the closure of Middle Eastern air routes, significant demand destruction is unlikely to materialise until April–May. Australia and Vietnam are expected to lead losses in absolute terms, as jet fuel shortages could begin to emerge as early as April.

Asia-Pacific jet fuel/kerosene demand destruction (kbd)

Source: Kpler

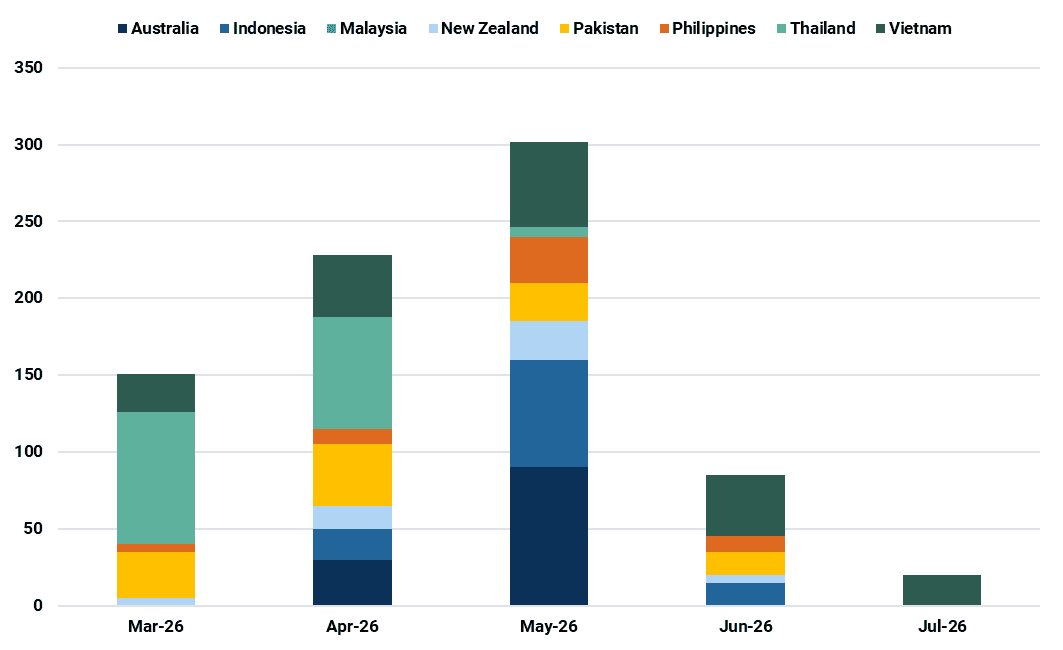

Diesel markets in Asia-Pacific appear particularly vulnerable, given limited supply flexibility, especially in developing economies, while higher prices are already weighing on demand across key end-user sectors. Beyond near-term demand destruction stemming from supply disruptions, a prolonged conflict could ultimately weigh on economic growth. This risk is amplified by the higher GDP elasticity of industrial and transport fuel demand in non-OECD economies, posing additional downside risks to our demand outlook beyond Q2-2026.

Asia-Pacific gasoil/diesel demand destruction (kbd)

Source: Kpler

In short, it is increasingly likely that even those dire estimates are somewhat underestimating second-level consequences of reduced fuel availability and mounting economic headwinds, so we are going to keep this analysis ongoing for the duration of the conflict, expanding the scope across all major liquids markets.

Market insights you can actually trust

Kpler delivers unbiased, expert-driven intelligence that helps you to track critical crude oil market developments for your own analysis. Our precise forecasting empowers smarter trading and risk management decisions. In times of conflict and geopolitical uncertainty, our real-time data keeps you ahead of supply disruptions and price volatility.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler